BCFC/iStock Editorial by way of Getty Photographs

In August 2021 I revealed an article through which I argued as soon as once more why Walgreens Boots Alliance (NASDAQ:WBA) is an efficient funding and gave 4 the explanation why I purchased the inventory shortly earlier than the article was revealed. Since then, the inventory elevated about 15% outperforming not solely the S&P 500 (SPY) however resulting in annualized beneficial properties of virtually 40% (not together with dividends). On this article I’ll argue why I’m much more bullish about Walgreens Boots Alliance now and nonetheless assume it’s a nice funding.

Quarterly Outcomes

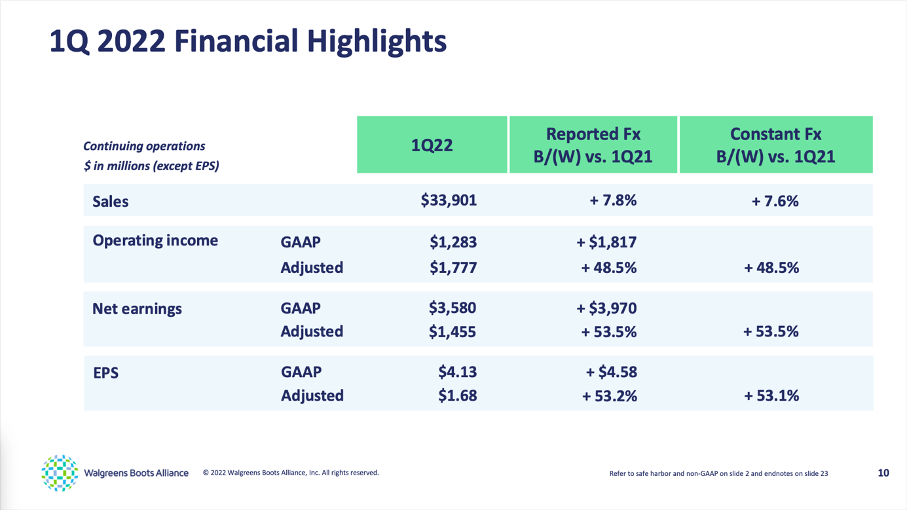

Within the first quarter of fiscal 2022, Walgreens Boots Alliance generated $33,901 million in gross sales and in comparison with $31,438 million in gross sales in the identical quarter final yr this is a rise of seven.8% year-over-year. Working revenue in Q1/22 was $1,283 million and in comparison with an working lack of $535 million in the identical quarter final yr this was a big enchancment however makes it unimaginable for us to calculate any significant development charges.

Walgreens Q1/22 Outcomes

Walgreens Boots Alliance may additionally report $4.13 in diluted earnings per share – in comparison with a lack of $0.36 per share in the identical quarter final yr. And when taking a look at adjusted diluted earnings per widespread share, we see a rise of 37.7% year-over-year from $1.22 in the identical quarter final yr to $1.68 this quarter.

VillageMD

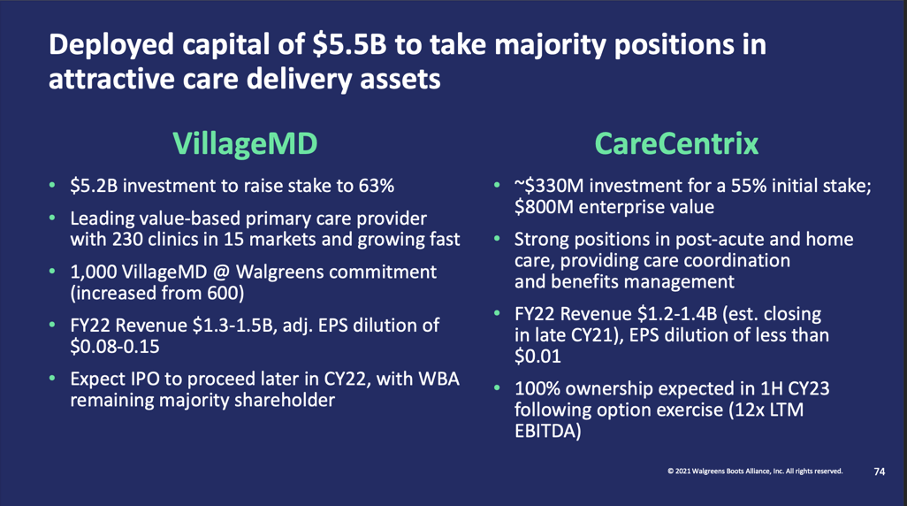

When trying on the quarterly outcomes above, we see an enormous discrepancy between earnings per share on GAAP foundation and the non-GAAP numbers. The massive discrepancy is stemming from $2,617 million in “Different revenue”, which was a results of the “acquisition” of VillageMD that was accomplished on November 24, 2021. However acquisition might be not the right time period – Walgreens Boots Alliance made a $5.2 billion funding in VillageMD and elevated WBA’s possession stake from 30 % to 63 %. However VillageMD stays a standalone firm and for 2022 it’s even planning an preliminary public providing.

VillageMD will use the $5.2 billion funding to speed up the opening of recent Village Medicals at Walgreens main care practices. Till 2025 not less than 600 new Village Medical in additional than 30 U.S. markets must be opened (and till 2027 even 1,000 are deliberate). Proper now, 81 VillageMD co-located facilities are open and by the top of calendar yr 2022 it must be not less than 160.

Walgreens Healthcare Acquisitions

Except for VillageMD, Walgreens Boots Alliance additionally invested about $330 million in CareCentrix and purchased a 55% preliminary stake, however a 100% possession is anticipated within the first half of 2023. CareCentrix is offering care coordination and advantages administration for sufferers who wish to heal or age at house. Presently, CareCentrix is managing take care of 19 million members via over 7,400 supplier areas.

Steadiness Sheet

Walgreens Boots Alliance spent $5.5 billion on acquisitions (or growing stakes in different corporations) and therefore it is sensible to take a look at the stability sheet as soon as once more. On November 30, 2021, Walgreens Boots Alliance had $2,647 million in short-term debt and $11,199 million in long-term debt. When evaluating the full debt to a complete fairness of $30,579 million, we get a D/E ratio of 0.45, which appears slightly low and isn’t any cause to fret. When evaluating the full debt to the working revenue Walgreens Boots Alliance may generate within the final 4 quarters ($3,826 million), it could take about 3.6 years to repay the excellent debt. And whereas this can be a little greater than I wish to see, we should level out, that working revenue was already greater in than previous ($,4834 million in fiscal 2019 and $6,223 million in fiscal 2018) and shall be most certainly greater once more.

Walgreens Boots Alliance additionally has $4,135 million in money and money equivalents on its stability sheet, which might be used to repay excellent debt. After subtracting this quantity, it could take solely 2.5 occasions the working revenue of the final 4 quarters to repay the excellent debt, which appears acceptable.

As consequence of the acquisitions, goodwill elevated from $12,421 million on August 31, 2021, to $21,520 million, which isn’t nice. Moreover, intangible property additionally elevated from $9,936 million to $12,770 million in the identical timeframe. All in all, the stability sheet just isn’t good, however it’s acceptable and no cause to fret and neither solvency nor liquidity must be a problem for Walgreens Boots Alliance.

Development

When trying on the development charges in the previous few years, Walgreens Boots Alliance can actually be described as struggling firm. Whereas income elevated with a CAGR of 6.26% within the final ten years, earnings per share have been principally flat during the last ten years and declined with a CAGR of 5.17% over the past 5 years. And when taking a look at these numbers, it isn’t shocking that traders are ascribing WBA such a low valuation a number of and that the inventory is in a corrective part for a number of years.

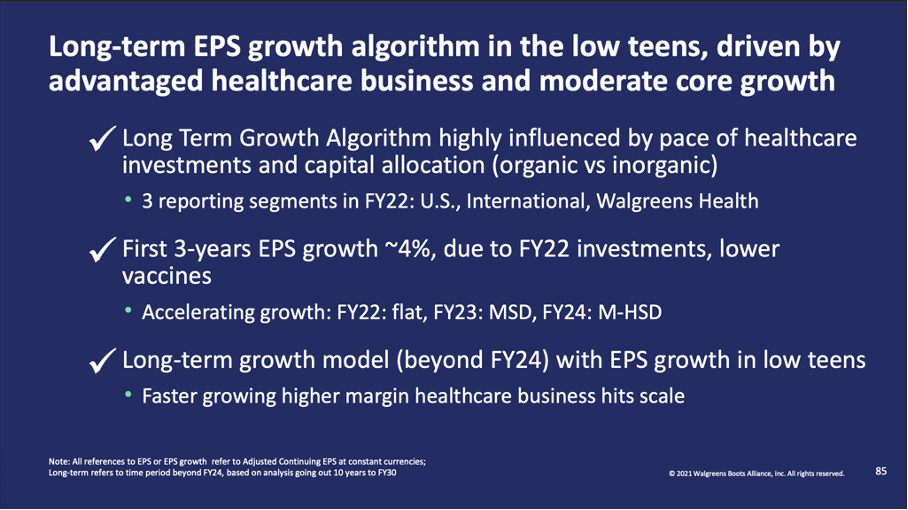

Nonetheless, in its final digital investor convention, administration was fairly optimistic that Walgreens Boots Alliance can return on the trail of excessive development charges it has been on in previous many years. Within the subsequent three years, administration is anticipating slightly low development charges (which is able to speed up over time), however from 2025 going ahead administration is anticipating earnings per share to develop within the low teenagers.

Walgreens Lengthy-term Steering

WBA Investor Day Convention

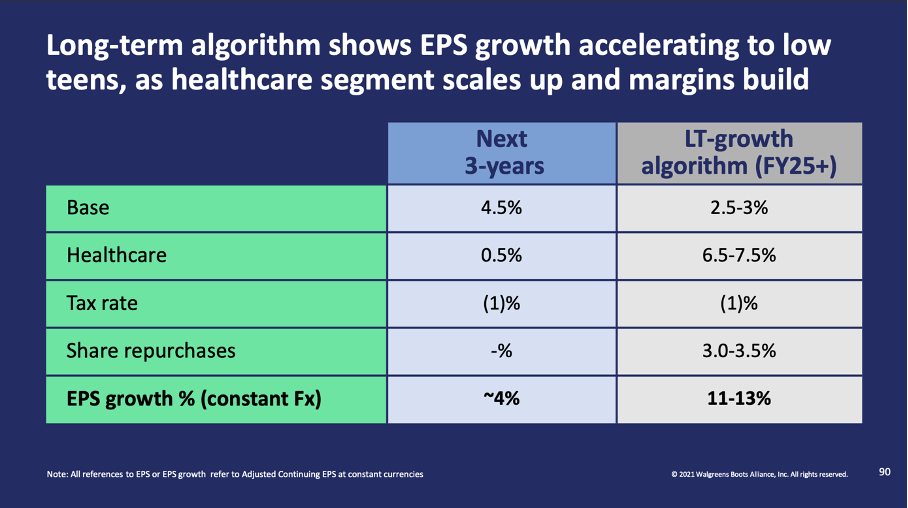

And when taking a more in-depth take a look at the long-term development algorithm, we will determine three most important drivers of EPS development. The bottom enterprise (Walgreens’ present enterprise) will contribute about 3% to long-term development and about 3.0% to three.5% development will stem from share buybacks, which the corporate will use once more as a device from fiscal 2025 going ahead.

WBA Lengthy-term algorithm

WBA Investor Day Convention

Nonetheless, the largest a part of long-term development ought to stem from “healthcare” as administration will ramp up healthcare investments to construct out the “long-term development engine”. And these healthcare investments vary from the above-mentioned majority stakes in VillageMD and CareCentrix, but additionally embody majority stakes in Shields in addition to the 28.5% shareholding in AmerisourceBergen (ABC) and the 21% shareholding in Possibility Care. In whole, Walgreens is valuing its healthcare portfolio at $20 billion. And within the years to return the sooner rising and higher-margin well being care enterprise will hit scale and contribute to development. Administration can also be mentioning, that over the long term, the tempo of the healthcare investments could have an enormous affect on the long-term development charges (implying that fluctuations are doable). However nonetheless, administration is seeing a transparent path to a development mannequin that goals for EPS development of 11% to 13%. And a gross margin that may pattern barely decrease resulting from continued strain from pharmacy reimbursement is already mirrored in that mannequin.

Dividend and Share Buybacks

Walgreens Boots Alliance can also be fascinating for its dividend and the corporate is without doubt one of the dividend aristocrats because it elevated the dividend for 46 years in a row. And with administration’s excessive expectations for EPS development, we will additionally assume that the dividend shall be raised much like EPS development. And I’m conscious that dividend development within the current previous was slightly disappointing for a lot of traders (though dividend elevated with a CAGR of 5.15% over the past 5 years, which is suitable). Proper now, Walgreens Boots Alliance is paying a quarterly dividend of $0.4775 per share leading to a dividend yield of three.52% proper now. And when trying on the adjusted earnings per share of the final 4 quarters (which have been $5.49), we get a payout ratio of 35% which is suitable. GAAP EPS of the final 4 quarters could be even $7.42, however resulting from “different revenue” (see above) this quantity is distorted, and I’d not use it right here.

As already talked about above, administration is not going to deal with share repurchases within the subsequent few years and we’ll solely see restricted quantities spent on share buybacks as administration will slightly deal with enhancing credit score metrics. Nonetheless, share repurchases are an necessary a part of the long-term technique and when trying on the development algorithm talked about above, share buybacks will most certainly contribute between 3.0% and three.5% to backside line development.

Intrinsic Worth Calculation

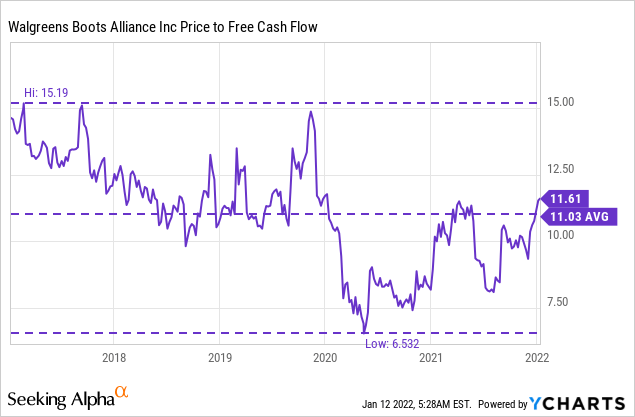

Walgreens Boots Alliance is buying and selling for a low P/E ratio of seven.25 proper now, however resulting from “different revenue” the EPS of the final 4 quarters was unusually excessive and the P/E ratio may not be the most effective metric to make use of. However when trying on the ahead non-GAAP EPS we nonetheless get slightly low valuation multiples proper now (10.71). Or when trying on the price-to-free-cash-flow ratio, Walgreens Boots Alliance is buying and selling for 11.5 occasions free money stream and though this is kind of in keeping with the common P/FCF ratio of the final 5 years (which was 11.03), the inventory remains to be extraordinarily low cost.

As an alternative of trying on the easy valuation metrics, we will additionally use a reduction money stream calculation to find out an intrinsic worth for Walgreens Boots Alliance. As foundation for our calculation, we will use the free money stream of the final 4 quarters, which was $4,057 million. When assuming that Walgreens Boots Alliance just isn’t capable of develop in any respect, the intrinsic worth for Walgreens Boots Alliance would nonetheless be $46.76 (assuming a ten% low cost charge and 867.6 million excellent shares). When assuming a modest development charge of solely 3% for the years to return, the intrinsic worth would improve to $66.80, and Walgreens Boots Alliance would already be undervalued.

However we will make a number of arguments, that an intrinsic worth of $66.80 remains to be not correct for Walgreens Boots Alliance. First, when trying on the common free money stream of the final 5 years, it was a lot greater than the free money stream of the final 4 quarters. And when utilizing that quantity ($4,995 million) as foundation as an alternative and assume as soon as once more 3% development until perpetuity, we get an intrinsic worth of $82.25 for Walgreens Boots Alliance.

When trying on the development assumptions and administration’s long-term steerage from above, we nonetheless should state that these assumptions are too cautious. An assumption of solely 3% development until perpetuity can also be too cautious when taking a look at previous development charges of Walgreens Boots Alliance. When calculating with the assumptions from Walgreens Boots Alliance long-term development algorithm (0% development in 2022, about 4% development in 2023 and about 7% development in 2024 and 11% development from 2025 going ahead) we get an intrinsic worth of $136.78 for the inventory. And I nonetheless used the decrease free money stream of the final 4 quarters and naturally solely 6% development until perpetuity beginning a decade from now (as I at all times do).

Walgreens Boots Alliance vs. CVS Well being Corp. (CVS)

I already noticed Walgreens Boots Alliance as an incredible funding up to now however contemplating the corporate’s newest strikes and particularly given the excessive development charges of its long-term development algorithm, I’d see Walgreens Boots Alliance as an actual discount now.

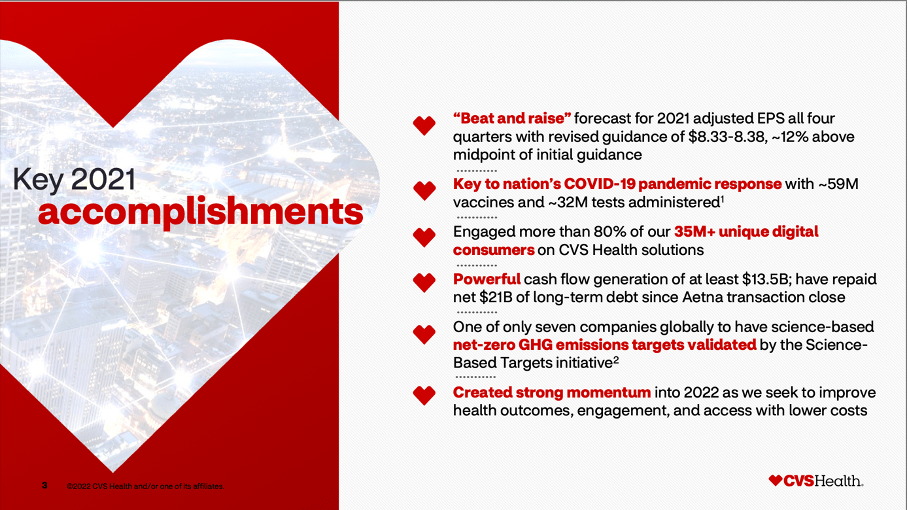

Prior to now few years, I argued a number of occasions that CVS Well being Corp. was an incredible funding and an actual discount. CVS is now buying and selling above $100 and has doubled for the reason that earlier cyclical lows. In September 2021 (when my final article about CVS was revealed), the inventory was buying and selling for $86, and I known as it nonetheless a discount. With CVS buying and selling for $106 on the time of writing we should cease utilizing the time period discount sooner or later, however CVS remains to be undervalued for my part and definitely one of many higher investments you can also make on this insanely overvalued market. CVS Well being additionally raised its steerage lately and contemplating adjusted earnings per share of $8.35 for fiscal 2021, the inventory is buying and selling for under 12.7 occasions earnings. And whereas these are non-GAAP numbers, the inventory can nonetheless be known as extraordinarily low cost. When utilizing assumptions, that are greater than practical for my part ($10 billion in FCF in fiscal 2021 in response to steerage and 6% development until perpetuity), we get an intrinsic worth round $170 for CVS making the inventory nonetheless undervalued.

CVS Key Accomplishments 2021

In my view, each corporations – CVS Well being Company in addition to Walgreens Boots Alliance – are nice investments and whereas I noticed CVS because the better discount up to now, I’d now argue that an funding in Walgreens may result in related returns.

Conclusion

Walgreens Boots Alliance and CVS Well being Company are actually two related corporations and are most likely stepping into an identical course. And it looks like Walgreens Boots Alliance is now assuming related excessive development charges for the enterprise as CVS’ administration did a number of years in the past (development charges within the low double-digits). Walgreens Boots Alliance additionally has a strong stability sheet and will even make a number of extra (smaller) acquisitions to strengthen its healthcare phase, which shall be one of many drivers for future development.

And the most effective half is, that at present share costs administration doesn’t should be proper with its development assumptions. If Walgreens ought to actually be capable to develop within the low double-digits over the long term, we might have an excessive discount on our palms. However even when administration is totally fallacious and overly optimistic and the enterprise can develop solely 3% yearly, we nonetheless have an undervalued inventory proper now.