portishead1

Timing

My timing couldn’t have been worse once I wrote my final article discussing Walgreens Boots Alliance (NASDAQ:WBA). WBA’s Q3 FY ‘22 outcomes introduced on June 30 despatched the inventory into an all-too-familiar tailspin, simply as I had argued for the agency as an undervalued, long-term purchase. Furthermore, I recommended, in that very same article, that CVS (CVS) was overvalued and subsequently its inventory was due for a pullback. As an alternative, CVS’ inventory soared following the discharge of their very own Q2 FY ‘22 outcomes earlier this month. Whereas each shares simply took a beating on account of (one other) opioid-case ruling, my thesis within the prior article is enjoying out in reverse…at the very least for the second.

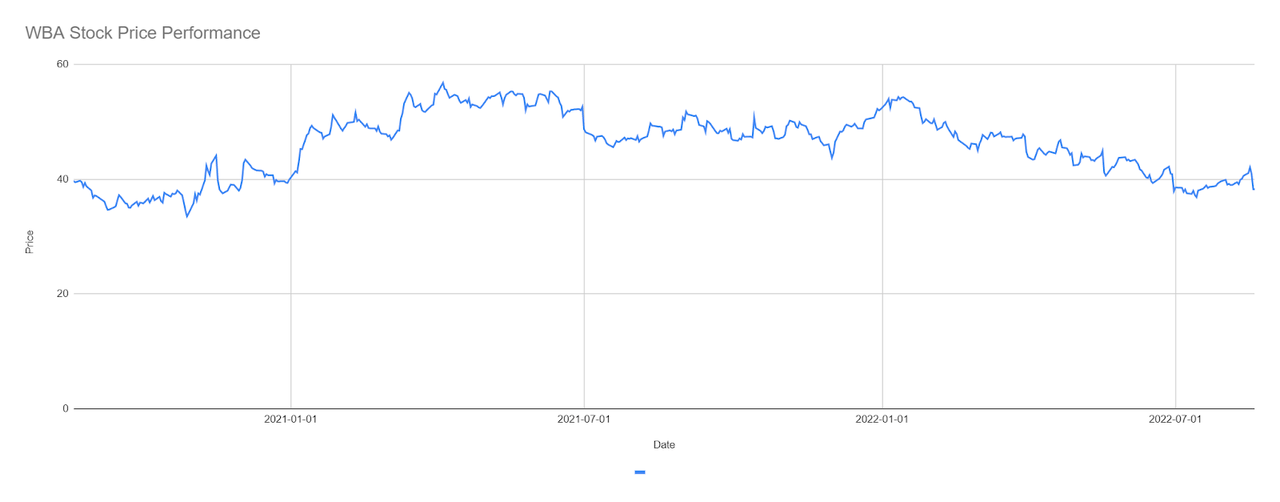

Determine 1: WBA Inventory Value Efficiency (Yves Sukhu) Determine 2: CVS Inventory Value Efficiency (Yves Sukhu)

Notes:

-

Information in Figures 1 and a couple of as of market shut August 19, 2022.

Some readers took me to process. In my protection, I didn’t argue particularly that WBA was going to take-off following Q3 FY ‘22 outcomes, nor that CVS would crater following their Q2 FY ‘22 earnings announcement. Reasonably, I proposed a “imply reversion” for each shares, with WBA presumably advancing extra rapidly than a pending decline in CVS’ shares. Maybe, I overestimated the tempo of a restoration in WBA’s share worth. Regardless, on this evaluation, I need to desk the dialogue on CVS for a second. As an alternative, I need to focus solely on WBA and the present bearish arguments in opposition to the inventory.

From my point-of-view, the bearish place in opposition to WBA is summarized as:

1. The core (retail + pharmacy) enterprise could also be weakening.

2. Walgreens Well being is an “unknown”. WBA tried the same technique prior to now solely to see it fail. The section presently operates at a loss and its success is way from assured.

3. Ample capital to gasoline Walgreens Well being growth could also be unavailable with the core enterprise below stress, administration’s failure to dump Boots UK, and the corporate’s current debt load.

On this evaluation, I discover these bearish arguments in opposition to the agency below the lens of Q3 FY ‘22 outcomes, provide a pathway to long-term development based mostly on a “correct” context of Q3 efficiency, and eventually current some ideas on the place shares could also be headed.

Setting Their Sights Decrease

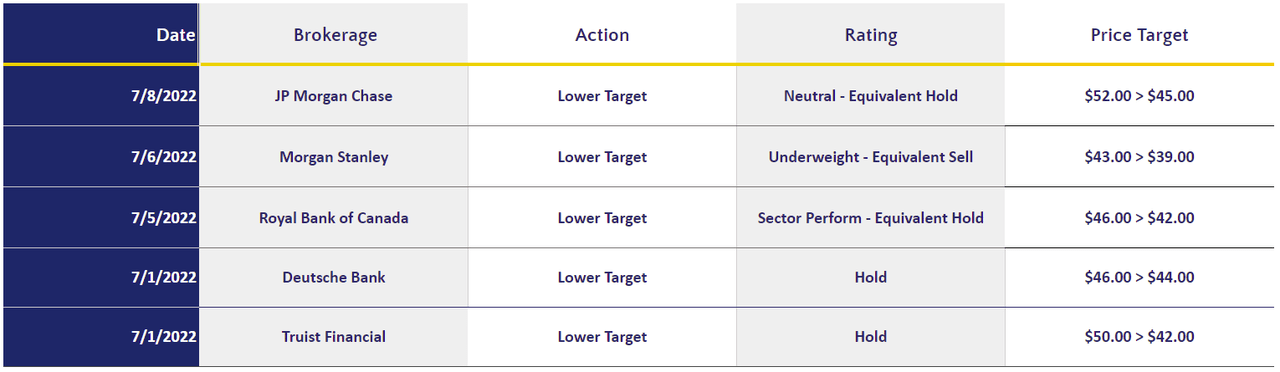

It’s price noting early on that a variety of analysts turned more and more bearish on WBA following Q3 FY ‘22 earnings, with a number of decreasing their worth targets for the agency.

Determine 3: WBA Analyst Rankings (MarketBeat)

Utilizing the (restricted) information from Determine 3, we will simply calculate that the typical analyst goal dipped from $47.40 to $42.40, or a decline of over (10%). The overall response amongst analysts following the earnings announcement was unsurprising. Allow us to revisit WBA’s efficiency for Q3 FY ‘22, and use it as a lead-in to our primary dialogue.

Questioning the Core

Okay, let’s get the plain out of the way in which. WBA’s Q3 FY ‘22 outcomes weren’t that nice. Amongst different issues:

-

Gross sales from persevering with operations of $32.6B decreased (2.8%) in fixed forex. Nevertheless, we should always observe that internet gross sales got here in barely forward of analysts’ common estimate of $32.2B.

-

The enterprise incurred a GAAP working lack of ($320M) versus GAAP working revenue of $1.1B in the identical prior 12 months interval. Non-GAAP working revenue was $1.0B within the quarter, representing a lower of (33.5%) versus the prior interval on a continuing forex foundation.

-

GAAP EPS from persevering with operations decreased (73.8%) to $0.33 versus the prior interval. GAAP EPS was considerably beneath the estimate of $0.66. Keep in mind, nonetheless, that GAAP EPS consists of WBA’s authorized bills related to its opioid-case settlement with the State of Florida. Adjusted EPS of $0.96 declined (28.9%) versus the prior quarter in fixed forex, however managed to beat the estimate of $0.92.

-

US section (retail + pharmacy) gross margin declined (60) foundation factors to twenty.8% versus 21.4% within the prior interval.

-

US pharmacy comparable scripts gross sales declined (1.8%) versus the prior interval, and complete US pharmacy gross sales decreased (9.7%).

-

After pushing for the sale of Boots UK to unencumber capital for growth of Walgreens Well being and different strategic initiatives, administration’s overview of the enterprise concluded with a choice to retain the enterprise.

On the floor, these outcomes would doubtless lead an investor to query the well being of the core enterprise. For instance, administration famous that comparable scripts gross sales really grew 2.1% within the US through the quarter excluding immunizations. However, we additionally observe that comparable scripts development, a key revenue driver, has been trending decrease, with 6.2% and 4.7% development in Q1 FY ‘22 and Q2 FY ‘22 respectively. Now, contemplating the “complete” of the section, if gross sales and margins are declining in america – the agency’s largest working section which has generated practically 97% of adjusted working revenue YTD – these circumstances clearly act to restrict the quantity of capital that administration can divert to its “poster-child” development engine, Walgreens Well being. And, in fact, WBA’s resolution to retain – or failure to dump – Boots UK doesn’t assist issues because the anticipated capital from such a sale is unavailable. And, nearly with out query, buyers would look unfavorably upon a choice by administration so as to add to their present $33.4B debt load to assist finance their healthcare ambitions. As such, it’s simple to attract the short conclusion, if solely from Q3 FY ‘22 outcomes, that WBA’s core enterprise will not be headed in the suitable path, imperiling administration’s skill to develop Walgreens Well being at a adequate price to determine a aggressive presence and to offset future declines within the core.

In Context

On the floor, the image appears to be like considerably bleak and Q3 FY ‘22 outcomes appear to mirror the final perspective of Raymond James analyst John Ransom, who I famous in one other article on WBA as saying:

[The] downside is I can title 5 issues mistaken with the core enterprise and never a lot proper.

Nevertheless, as we parse WBA’s efficiency, maybe we would maintain a couple of issues in thoughts:

1. WBA, like everybody else, was battling a troublesome inflationary setting on the finish of their Q3 FY ‘22. And with inflation largely peaking within the Could-June interval, their Q3 ended through the “worst of the storm”.

2. The corporate was lapping a very sturdy Q3 FY ‘21 that was bolstered by COVID-19 tailwinds.

3. Many WBA areas haven’t but returned to regular working hours on account of labor shortages/constraints.

4. “[Challenging] monetary market circumstances past [WBA’s] management” prevented administration from offloading Boots UK, and a “hearth sale” didn’t appear warranted given sturdy efficiency from the enterprise.

5. Administration continues to be within the (comparatively) early levels of constructing out Walgreens Well being. The section will not be but worthwhile and introduces an EPS headwind; however that headwind is anticipated to say no in FY ‘23 because the operation turns to profitability thereafter.

6. WBA elevated its stake in AllianceRx Walgreens specialty pharmacy to 100% in Q1 FY ‘22 noting “…there could be a 7% decline in [US] revenues because of roughly an $8 billion decline within the AllianceRx Walgreens Prime enterprise. Administration is presently restructuring the enterprise, inclusive of its funding in Shields.

The factors above should not meant to function excuses for WBA’s efficiency, however slightly give some context for the agency’s working setting in Q3 FY ‘22, and FY ‘22 on the whole. Certainly, a more in-depth have a look at Q3 FY ‘22 outcomes reveal a greater efficiency than some might have initially understood:

-

“[Net] gross sales [from continuing operations] exceeded expectations, rising 3% excluding the unfavorable influence of the decline in AllianceRx Walgreens enterprise and the gross sales development from Walgreens Well being.” In different phrases, WBA’s core enterprise minus specialty pharmacy nonetheless grew throughout Q3 FY ‘22.

-

Internet gross sales of $100.3B for the 9 months ended Could 31, 2022 mirrored a rise of two.7% in fixed forex. Furthermore, “…[front-of-store] margins [were] up considerably year-on-year.”

-

US retail comparable gross sales elevated 2.4%, excluding tobacco, versus the prior quarter. The decline within the AllianceRx enterprise, talked about above, acted as an “…850 foundation level headwind to [US] gross sales”. It’s cheap to anticipate WBA’s largest section to return to development because the specialty pharmacy enterprise emerges with a “…extra energized…technique.”

-

US pharmacy gross sales declined (9.7%) throughout Q3 FY ‘22, however comparable pharmacy gross sales really grew 2.0%. Once more, context is essential with respect to WBA’s Q3 FY ‘22 US pharmacy outcomes, because the agency lapped a very sturdy quarter within the prior interval that was bolstered by COVID-19 tailwinds. Even so, comparable pharmacy gross sales elevated, with administration explaining that “…[pharmacy] volumes stay challenged by staffing shortages and momentary working hour reductions.”

-

Worldwide section gross sales grew 9.3% in Q3 FY ‘22 to $5.3B versus the prior quarter in fixed forex, with adjusted working revenue doubling to $174M. The section’s internet gross sales for the 9 months ending Could 31, 2022 stood at $16.7B, reflecting a 15.7% enhance versus the prior interval in fixed forex. Boots UK grew gross sales 13.5% through the quarter and drove 103% adjusted working revenue for the Worldwide section as an entire in Q3 FY ‘22.

-

GAAP internet money from working actions of $1.6B and free money movement of $1.3B for Q3 FY ‘22r; GAAP internet money from working actions of $3.8B and free money movement of $2.6B for 9 months ended Could 31, 2022. GAAP internet money from working actions within the quarter declined (7%) and (11.5%) for the 9-month interval. Free money movement (“FCF”) declined (13%) and (22.2%) for the quarter and 9-month interval, respectively. Whereas each money from operations and FCF decreased, once more keep in mind that WBA lapped a very sturdy Q3 FY ‘21, was managing by inflationary circumstances, and lots of shops are nonetheless not working on their regular schedule.

-

Walgreens Well being gross sales of $596M for Q3 FY ‘22. Walgreens Well being gross sales through the quarter elevated 13% on a sequential foundation, with the section reporting $527M in gross sales for Q2 FY ‘22. Additional, with 2.3M lined lives on the finish of Q3 FY ‘22, WBA is already forward of their 2M lined lives CY ‘22 purpose.

So, with context, WBA’s Q3 FY ‘22 outcomes had been arguably not that unhealthy.

A Mannequin for Constant Development

We are actually naturally led to ask how the agency will return to a path of constant development and improved profitability. I elaborate my ideas as follows:

1. Stabilizing and rising the core: As talked about above, the core enterprise, though not with out its points, is arguably performing higher than many give it credit score for. Administration has been working to handle pharmacy staffing points with sturdy hiring incentives. Additional, they’re working to return hundreds of shops to regular working hours. Thus, whereas staffing and working challenges might lumber into This fall FY ‘22, there’s purpose to hope they are going to be largely resolved heading into and through FY ‘23. Additionally, the core enterprise may even see a greater margin efficiency in FY ‘23 with the restructure of the specialty pharmacy enterprise, as mentioned within the subsequent level, and as administration continues its push for US pharmacy efficiencies with the rollout of extra micro-fulfillment facilities. These facilities take away routine duties from “the arms” of pharmacists, permitting them to deal with affected person interplay and affected person care. Whereas WBA is a bit behind their anticipated rollout of those facilities, the expectation is that “…[the] facilities [which] fill about 20% of retailer scripts as we speak, [will head] to 40% to 50% over time.”

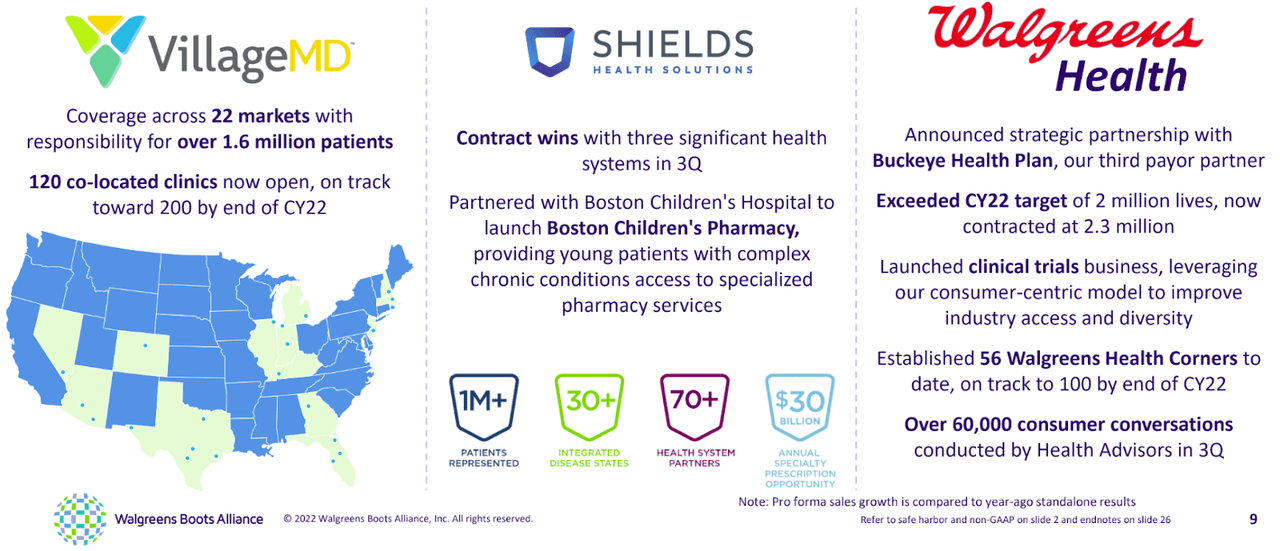

2. A revitalized specialty pharmacy technique: WBA CFO James Kehoe remarked through the firm’s Q1 FY ‘22 earnings name that the choice to buy 100% of AllianceRx was pushed by the necessity to restructure the enterprise, and the view that “…[it’s] most likely higher below one proprietor to do [it] faster.” With that sense of urgency in thoughts, buyers may see an improved top-line and profitability image shifting into FY ‘23 pushed (partly) by the reorganized specialty pharmacy enterprise; a enterprise that carries increased margins than, for instance, generic medication. Furthermore, the specialty pharmacy enterprise, inclusive of Shields, will play an essential position within the coming fiscal interval with administration noting that “…[they] anticipate decrease ranges of exercise on COVID vaccinations subsequent 12 months…[and that] does generate a large headwind subsequent 12 months.” Accordingly, the upper margins provided by the AllianceRx enterprise will assist to offset declines in COVID-19 vaccinations. Traders also needs to acknowledge the specialty pharmacy enterprise as a development car for WBA as that specific market maintains a CAGR that’s increased than the general prescription drug market, and represents an annual $30B alternative based on administration.

Determine 4: Walgreens Specialty Pharmacy Alternative (WBA Q3 FY ’22 Earnings Presentation)

3. Walgreens Well being growth: Mr. Kehoe defined additional through the Q3 FY ‘22 earnings name that “[WBA is] spending doubtlessly extra within the second half of [FY ‘22 on Walgreens Health] due to timing. However the headwind on Walgreens Well being will go from 6% this 12 months, all the way down to very low single digits subsequent 12 months.” Therefore, whereas Walgreens Well being is more likely to nonetheless produce a loss in FY ‘23, the ensuing EPS headwind must be far weaker. Administration reported that the corporate, which elevated its stake in VillageMD to 63% in 2021, stays on observe to open 200 co-located clinics by the tip of the calendar 12 months. These openings can be complemented by the opening of 100 Walgreens Well being Corners by the tip of CY ‘22, with every in-store “nook” permitting well being plan sufferers to speak straight with pharmacists and different medical professionals. The corporate appears to be “on observe” to attain $2B in internet gross sales for the section in CY ‘22 (not FY ‘22), and to attain a run-rate of $10B in gross sales by FY ‘25.

4. Nurturing Boots UK for a future sale: Maybe it is going to show a “blessing in disguise” that administration was unable to dump Boots UK with, as already talked about, that enterprise rising gross sales 13.5% through the quarter and driving 103% development in adjusted working revenue for the Worldwide section in Q3. Clearly, ought to administration proceed to reveal development in and viability of the enterprise, the section will fetch a better valuation sooner or later, particularly as world market circumstances (hopefully) enhance. Certainly, WBA CEO Roz Brewer made positive to say through the Q3 FY ‘22 earnings name that “…[WBA] will keep open to all alternatives to maximise shareholder worth.” Understanding that the Worldwide section generates a minority of WBA’s income, I’ve little doubt Boots UK can be offered in some unspecified time in the future to unencumber capital for growth in healthcare providers and specialty pharmacy, and for debt discount.

5. Continued expense discount: WBA’s Transformation Value Program, which started in December 2018, has been very profitable and continues to be so. With an authentic goal of $1.5B of annual price financial savings by FY ‘22, the goal has been repeatedly raised and now stands at $3.5B in annual financial savings by FY ‘24.

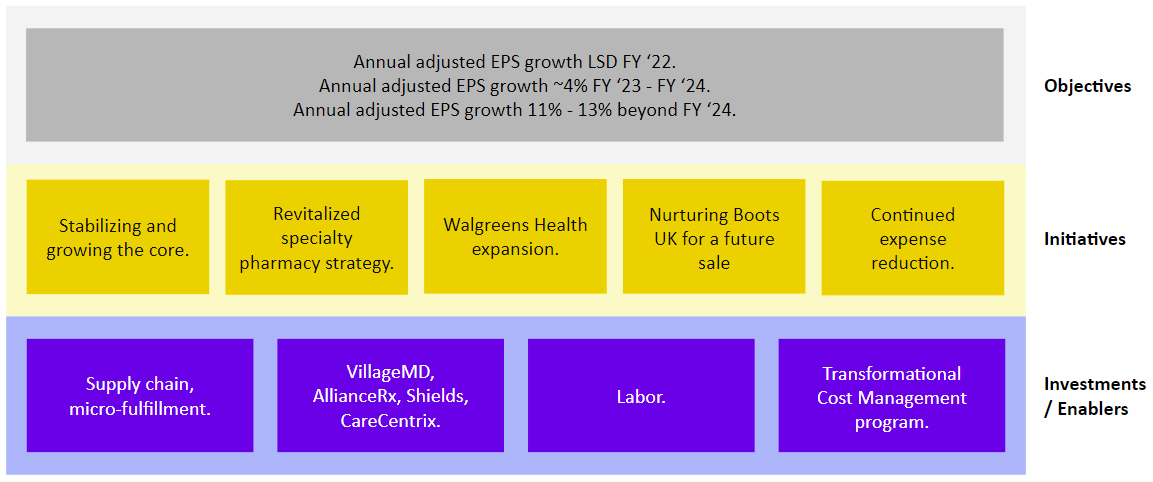

Whereas there are not any ensures, the sum of the actions above provide a pathway for WBA to trace in opposition to its long-term development algorithm of low single-digit adjusted EPS development in FY ‘22 (re-affirmed following Q3 FY ‘22 earnings outcomes) and ~4% development for FY ‘23 by FY ‘24, whilst the corporate faces down a major COVID-19 headwind shifting into This fall of this fiscal 12 months and heading into FY ‘23. As I usually love to do, I created the next diagram to aim to seize the connection between the weather of this part, particularly administration’s monetary aims versus their underlying initiatives and investments.

Determine 5: WBA Strategic Mannequin (Yves Sukhu)

Observe that Determine 5 above displays my interpretation of WBA’s strategic mannequin and doesn’t straight map to administration’s mannequin; though, in fact, they overlap.

A Robust End?

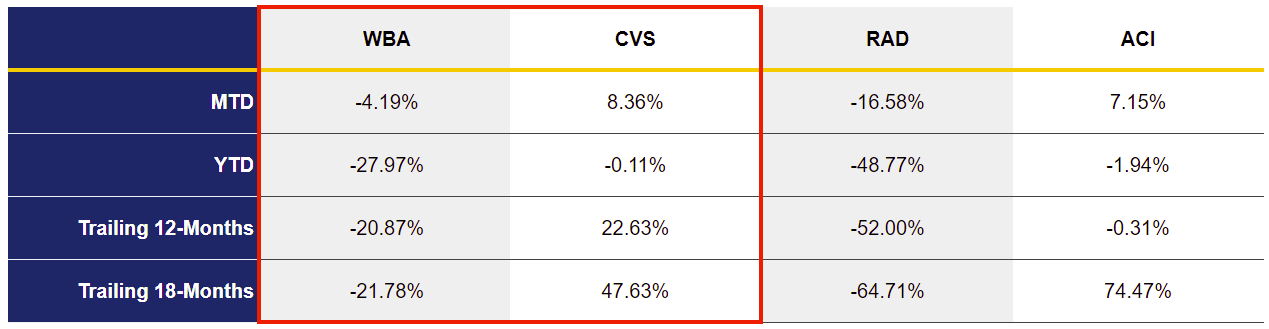

So, if we would agree WBA’s core enterprise and technique should not the “misplaced trigger” that many might need us consider, how will the remainder of the 12 months play out? This actually has not been a great 12 months for WBA shares; particularly when in comparison with CVS.

Determine 6: WBA and Chosen Competitor Efficiency Comparability (Yves Sukhu)

Notes:

-

Information as of market shut August 19, 2022.

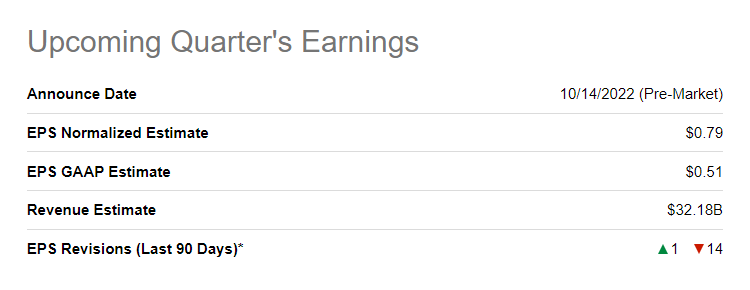

Attempting to foretell what is going to occur on the finish of WBA’s FY ‘22 is, in fact, anybody’s guess. Past all of the macroeconomic and geopolitical uncertainty, WBA administration notes that they “…anticipate some headwinds within the fourth quarter…Vaccinations are an anticipated headwind of 15 to 17 proportion factors. Investments to construct out…Walgreens Well being section may lead to 10% to 12% influence on fourth quarter EPS. Different headwinds embody labor investments of round 5 proportion factors and lapping prior 12 months one-time positive factors of roughly 4 proportion factors of EPS development. Mixed, these headwinds quantity to an anticipated 34% to 38% year-on-year headwind and results in full 12 months EPS development of low single digits.”

Determine 7: WBA This fall FY ‘22 Income and EPS Estimates (In search of Alpha)

In contrast in opposition to This fall FY ‘21 adjusted EPS of $1.17, the normalized EPS estimate for This fall FY ‘22 does certainly quantity to a greater than (30%) lower versus the prior interval.

With shares already “beat up”, a This fall FY ‘22 shock may clearly spark the inventory fairly a bit increased. Then once more, I proposed the identical thought earlier than Q3 FY ‘22 and look how that performed out. However, to reiterate, WBA did beat adjusted EPS and internet gross sales estimates in Q3; though the efficiency was not sturdy sufficient to excite the market.

What may result in a considerable beat in This fall FY ‘22? I speculate that the next may very well be (cheap) prospects:

1. Cooling inflation as a gross sales driver. As mentioned earlier, WBA’s Q3 FY ‘22 ended simply because the inflation price was peaking in america. With inflation cooling off, and customers spending their “new” financial savings, WBA, like different retailers, may see a gross sales bump by the tip of the 12 months.

2. An surprising COVID-19 enhance. Whereas the charges of latest COVID-19 infections and fatalities fortunately proceed to fall, the World Well being Group simply famous that there have been nonetheless 15,000 COVID-related deaths prior to now week all over the world, describing the statistic as “utterly unacceptable”. So, whereas WBA administration is anticipating a considerable COVID-19 headwind within the fourth quarter, it’s nonetheless potential {that a} 4th COVID-19 shot advice should still be “within the playing cards”. And, as I discussed in my final article discussing WBA, administration’s FY ‘22 steering doesn’t think about a 4th COVID-19 shot. As I’ve mentioned so many instances in order to sound like a “damaged report”, at any time when the world thinks the pandemic is “completed”, it appears to return roaring again. Therefore, there’s nonetheless “room” for a COVID-19 tailwind in This fall.

3. Higher than anticipated price administration outcomes. Once more, one in all administration’s ongoing highlights is the success of the Transformational Value Administration Program. Optimistically, this system might over-deliver within the fourth quarter and assist a greater bottom-line efficiency as in comparison with present estimates.

So, I feel it’s cheap, not assured, to suppose WBA may ship a powerful end to the present fiscal 12 months significantly with quite a lot of unhealthy information already baked into the inventory worth. One specific threat is WBA’s looming monetary accountability associated to the Ohio opioid-case ruling talked about earlier. Nevertheless, it’s not clear that WBA, or CVS and Walmart (WMT) for that matter, can be required to make any instant funds; and WBA plans to enchantment the ruling. So, shares may simply rally because the 12 months wraps up, particularly noting that the inventory had been marching increased, buying and selling above $42/share earlier than information of the opioid-case broke.

Working Some Numbers: A Quantitative View on Shares

Past the cheap chance of a powerful end to FY ‘22, we would strive to have a look at the rest of the fiscal interval in a extra quantitative method. I nonetheless argue that WBA is undervalued and that its valuation multiples are more likely to revert to the imply, particularly as the corporate positive factors extra traction with Walgreens Well being and its specialty pharmacy companies – two faster-growing, higher-margin segments that assist to justify increased multiples for the agency. Contemplate WBA’s P/S and P/B multiples:

Determine 8: WBA and Chosen Competitor Comparability (Yves Sukhu)

We see that WBA’s multiples are effectively beneath these of CVS. Additional, WBA lags CVS on a P/E foundation as effectively, with In search of Alpha information offering us with trailing-twelve-month (“TTM”) P/E multiples of seven.08 and 12.14 for WBA and CVS, respectively. After all, we will argue that CVS deserves increased P/S, P/B, and P/E multiples as its advantages and pharmacy providers companies provide buyers an organization with the next development and profitability trajectory. This can be a legitimate argument; however it doesn’t essentially invalidate the argument that WBA may very well be undervalued based mostly on its present multiples. Actually, utilizing information from Macrotrends, WBA’s historic common P/B is revealed to be roughly in-line with CVS’ present P/B of ~1.8. Utilizing that single information level and most-recent quarter (“MRQ”) guide worth information, we’d arrive at a share worth of $54.68.

WBA share worth by way of P/B a number of = 1.8 * $30.38 guide worth/share

= $54.68

Notes:

- MRQ guide worth/share information from Yahoo Finance.

Macrotrends equally affords historic P/E information for WBA with a mean worth of ~15. Clearly, this P/E worth would lead to a share worth greater than double what it’s proper now.

Am I saying that WBA shares are headed to $50+, or $60+, and even $70+? I don’t know precisely the place shares are headed within the near-term. Nevertheless, as Walgreens Well being turns a nook “into the black” and administration “rights the ship” with respect to the specialty pharmacy enterprise to drive higher general core efficiency, I do suppose WBA shares can be buying and selling considerably increased. Certainly, shares had been buying and selling above $70 not all that way back in early 2019.

Once more, noting that shares had been trending increased earlier than the newest opioid-case ruling, I’m betting that buyers selecting up shares now within the excessive $30s have a great likelihood to be rewarded with the potential for a better-than-expected This fall. Even when shares solely attain the typical analyst goal of $42.40 from Determine 3, shares as we speak provide greater than 10% upside, which is to say nothing of the present 5% dividend yield. I’m bullish that shares might finish the calendar 12 months as they started: above $50. Merely, I feel that the market goes to “determine” that administration is heading in the right direction, and that shares warrant the next valuation.

Sticking It Out

Usually, I think that lengthy buyers who’re “prepared to stay it out” as WBA achieves scale with Walgreens Well being and its specialty pharmacy companies are going to be rewarded. I, for one, have been (cautiously) including to my lengthy place because the inventory tanked following the Q3 FY ‘22 earnings announcement.

If I come again to my define of the three primary elements of the bear argument in opposition to WBA, I’d retort as follows based mostly on this evaluation:

1. The core enterprise carried out admirably throughout Q3 when discounting the influence from AllianceRx and investments in Walgreens Well being. This efficiency was delivered regardless of a troublesome working setting, together with excessive inflation and staffing challenges. Furthermore, administration is appearing appropriately to stabilize/develop the enterprise, significantly with respect to restructuring of the specialty pharmacy section.

2. Walgreens Well being, whereas nonetheless embryonic, is on observe to attain its CY ‘22 objectives, together with $2B in internet gross sales and the opening of 200 co-located VillageMD areas. A key distinction with WBA’s healthcare technique “this time round” is their resolution to spend money on a strategic accomplice (i.e. VillageMD) versus attempting to “go it alone”, thereby lowering their threat. Whereas the continuing transformation of Walgreens’ general enterprise will carry threat, indications up to now are optimistic.

3. With a secure/rising core, the expectation could be that WBA’s conventional retail + pharmacy operations ought to be capable of throw off adequate capital to assist Walgreens Well being growth, with out administration needing to resort to extra debt. Additional, with the profitability trajectory of VillageMD areas well-understood, older (early) areas ought to begin working “within the black” within the close to time period, thereby serving to to assist the opening of extra new areas. As extra VillageMD areas cross the brink into profitability, the cycle turns into self-reinforcing. Additionally, one of many proposed advantages of co-locating VillageMD main care workplaces subsequent to Walgreens pharmacies is to drive scripts development. So, VillageMD ought to begin to “feed” the core increasingly as time goes on, offering extra assist for Walgreens Well being growth. Lastly, I do anticipate that Boots UK can be ultimately offered; and administration will clearly make the suitable resolution at the moment if and how one can distribute that capital with respect to Walgreens Well being.

To reiterate, I feel buyers are going to “determine all this out” themselves and reward the inventory appropriately. However, what in regards to the lowered worth targets provided by analysts as seen in Determine 3? Are all these analysts merely mistaken with their unfavorable outlook on shares? It’s tough to make such an assertion. Nevertheless, it may be honest to say they’re too pessimistic of their view. I learn a report from one analyst who said, in so many phrases, that he most popular to attend and see how the story with Walgreens Well being performs out earlier than making a name on the inventory. However, for these buyers searching for undervalued companies, does it make sense to take a position after a method has confirmed itself as such an apparent success that the inventory now trades at the next valuation? In different phrases, does it make sense to take a position now with the inventory “beat up” however with indications that the corporate can be profitable within the long-term; or, does it make sense to take a position later when the inventory has “caught up” with its honest worth as a result of the market has lastly acknowledged the agency’s strategic potential? It must be clear from this report how I really feel.

As with most issues in life, there are not any ensures. Nevertheless, I reiterate that WBA’s technique is one which appears to place the agency for long-term success, which can be correspondingly mirrored within the share worth.