Justin Sullivan

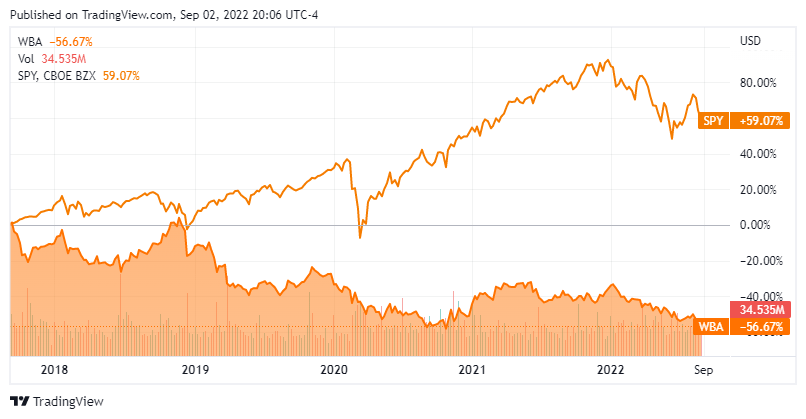

Shares of Walgreens Boots Alliance (NASDAQ:WBA) have dissatisfied shareholders currently, declining -31.88% over the previous yr and -33.53% YTD. It has been a tough street as WBA began 2022 at $53.06, and shares have slid to $35.27. Not even the big 5.45% dividend yield can get shareholders excited as new 52-week lows have been simply made. The market is not rewarding many corporations lately, however WBA generates billions in income not like many common corporations. No one is aware of when the market will, and the present weak point is creating some engaging alternatives for long-term buyers. WBA has been in a perpetual decline as shares have misplaced -56.67% of their worth over the earlier 5-years. With shares yielding over 5%, I believe it is time to think about shares of WBA for an income-focused portfolio.

Looking for Alpha

Walgreens is buying and selling at a lovely valuation though the market continues to punish its shares

This will not be the perfect atmosphere to choose winners and losers or see which corporations buyers are overlooking as the vast majority of shares are declining. The Nasdaq is in a bear market, whereas the S&P is on the verge of crossing over into bear market territory as soon as once more. WBA has declined -33.53%, underperforming the main indices in 2022. It is market cap has declined to $30.3 billion, which is now lower than the whole fairness on WBA’s stability sheet. WBA can also be getting near buying and selling at a 1:1 ratio to its e-book worth. Many information articles and segments on monetary information networks have mentioned profitless tech and the way corporations with non-existent EPS and FCF will proceed to be punished in a rising fee atmosphere. Taking a look at WBA’s financials, there are a whole lot of the reason why I get bullish on WBA.

Free Money Movement (FCF) is commonly checked out as top-of-the-line measures of profitability as FCF excludes the non-cash bills of the revenue assertion and consists of spending on tools and property in addition to modifications in working capital from the stability sheet. To some buyers, FCF is extra vital to research than web revenue as a result of it is more durable to govern as it’s a true indication of the corporate’s money. FCF can also be the pool of capital that corporations can make the most of to repay debt, pay dividends, purchase again shares, make acquisitions, or reinvest within the enterprise. With each share of inventory bought, you are getting an fairness share of the enterprise in return, and your shares characterize a portion of the income and earnings generated. In my view, companies that generate giant quantities of FCF needs to be rewarded, not discarded.

With regards to the FCF a number of, I wish to pay between 18-22 instances FCF for a corporation’s inventory, and if I can discover good corporations buying and selling at lower than 18x FCF, my curiosity instantly elevates. The FCF a number of that the market locations on an organization might be discovered by dividing an organization’s market cap by the FCF produced over the trailing twelve months (TTM). Apple (AAPL), as an illustration, trades at an FCF a number of of 23.28x ($2.5 trillion / $107.58 billion). I’m keen to pay extra for a corporation’s FCF if they’ve a bigger progress fee, and AAPL at 23.28x FCF appears to be like very intriguing.

WBA has generated $5.06 billion in money from operations and allotted $1.62 billion to CapEx placing its FCF at $3.44 billion over the TTM. WBA’s market cap is $30.3 billion, which implies its buying and selling at 8.86x its FCF. WBA trades at one of many lowest FCF ratios of all of the Dividend Aristocrats. Worldwide Enterprise Machines (IBM) trades at a FCF a number of of 14.08x ($115.42 billion market cap / $8.2 billion FCF), Johnson & Johnson (JNJ) trades at a FCF a number of of 21.45x ($427.87 billion market cap / $19.95 billion FCF), Kimberly-Clark (KMB) trades at a FCF a number of of 23.59x ($42.7 billion market cap / $1.81 billion FCF), and Caterpillar (CAT) trades at a FCF a number of of 31.28x ($95.46 billion market cap / $3.05 billion FCF).

Wanting additional by WBA’s financials, I discovered two metrics that have been additionally attention-grabbing. WBA has $31.16 billion of complete fairness on its stability sheet. As WBA’s market cap is $30.3 billion, it is at present buying and selling at a -2.75% low cost to the fairness on its stability sheet. Most corporations commerce at a premium to fairness, and WBA has now fallen under a 1:1 ratio. The opposite side that appears attention-grabbing is WBA’s e-book worth. On WBA’s stability sheet, its e-book worth per share is $30.38. WBA at present trades at a 16.1% premium to its e-book worth. For worth buyers, the P/B ratio is a timeless methodology for locating shares that might be mispriced. A P/B ratio of lower than 1 might be an indicator that the market has misunderstood an organization and undervalued it. As WBA is buying and selling near a 1:1 e-book worth, there might be an underlying alternative in its shares.

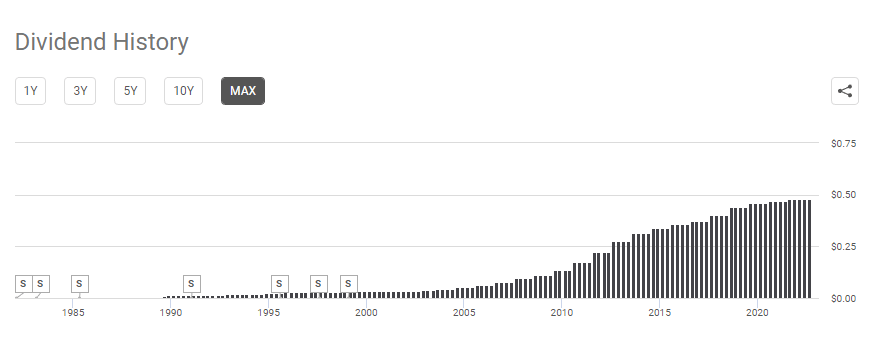

WBA is approaching Dividend King standing and continues to allocate capital again to shareholders

WBA is a Dividend Aristocrat approaching Dividend King standing because it elevated its annual dividend for 46 consecutive years. WBA’s share worth has been declining, however that hasn’t stopped WBA from rewarding its shareholders with a rising dividend and buybacks. WBA generates billions in FCF and places that pool of capital to work. With each share repurchased, shareholders personal a bigger a part of the fairness in WBA, and with each dividend improve, shareholders obtain a bigger portion of the earnings every share generates.

Since WBA’s final inventory cut up in 1999, its quarterly dividend has elevated by 1,377% going from $0.0325 to $0.48. WBA pays a dividend of $1.92 per share, which is a 5.45% yield. Within the TTM, WBA has generated $6.22 in EPS, inserting its annual payout ratio at 30.87% of its earnings. WBA’s dividend has a 5-year progress fee of 4.63%, with 46 years of consecutive will increase. At immediately’s costs, WBA is producing appreciable quantities of revenue and, after 4 extra will increase, shall be thought-about a Dividend King.

Looking for Alpha

WBA has additionally used its income to purchase again shares. In 2015 WBA had 1.09 billion shares excellent. Since then, WBA has used its FCF to purchase again 224.5 million shares, decreasing its excellent shares by -20.62%. With every buyback, WBA will increase the quantity of fairness its remaining shares characterize, and its EPS and income per share are unfold amongst a decrease float. Whereas many corporations proceed to concern shares and dilute shareholders, WBA not solely will increase fairness for its buyers however has offered many years of dividend will increase. I believe that is one thing that’s neglected and that corporations who create worth for shareholders by buybacks and dividends needs to be rewarded, not discounted. WBA is doing this from a place of economic stability, not weak point.

Conclusion

I imagine shares of WBA have gotten too low-cost and misplaced within the havoc created by the declining indices. Right now, WBA trades at 8.86x FCF, trades at a reduction to its fairness, and is getting near a 1:1 P/B. WBA generates $134.52 billion in income and billions in income. Right now you’ll be able to decide shares up at a steep low cost and receives a commission a dividend that exceeds 5% when you watch for a turnaround. I believe WBA might be a terrific revenue inventory and a capital appreciation generator if you happen to take a long-term strategy. For buyers who WBA has burned, perhaps now could be the time to contemplate greenback value averaging into the place and reinvesting the dividend. WBA’s observe document means that future buybacks and dividend will increase will happen as they’ve an impeccable observe document of producing FCF. When the markets lastly recuperate, I may see WBA buying and selling over $50 per share as soon as once more.