Michael M. Santiago/Getty Photographs Information

Walgreens Boots Alliance (NASDAQ:WBA) shares have fallen a whopping 42.7% over the previous 5 years and are down 7.4% for the YTD. Granted, the dividend is a considerable 3.95%, however even the entire returns are unfavorable for the previous 1-, 3-, and 5-years (-0.38%, -10.1%, and -7.6% annualized returns, respectively).

Looking for Alpha

5-Yr value historical past and fundamental statistics for WBA (Supply: Looking for Alpha)

In recent times, WBA has been more and more proactive in maintaining with healthcare tendencies. The corporate’s imaginative and prescient is to turn into the “neighborhood well being vacation spot”, whereas additionally ramping up ecommerce. FY Q1 digital gross sales had been up 88% vs. final yr (see slide 6). The corporate launched an improved Walgreens client app in November and is conducting a telemedicine kiosk pilot program. Walgreens can also be constructing out a community of major care clinics.

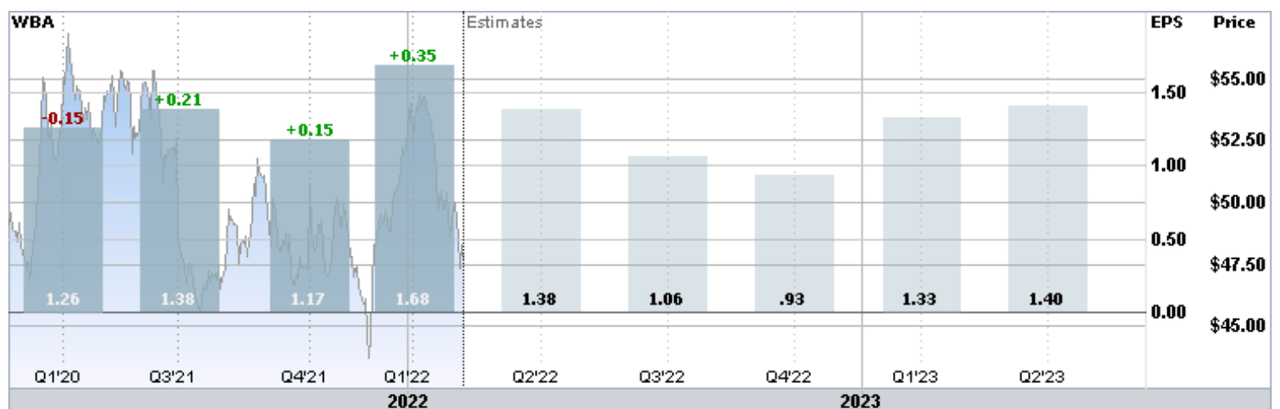

WBA has crushed analyst expectations for EPS for the previous 3 quarters, most just lately with FY Q1 2022 EPS, reported on January sixth, that was 26% above expectations. These current sturdy outcomes are a short-term COVID vaccine bump slightly than indicating sustainable progress. The consensus estimate for annualized EPS progress for the subsequent 3-5 years is 3.3% per yr.

ETrade

Trailing 4 quarters and estimated future quarterly EPS. Inexperienced (pink) values are quantities by which EPS beat (missed) consensus expectations (Supply: ETrade)

WBA has a ahead dividend yield of three.95%. The three-, 5-, and 10-year annualized dividend progress charges are 4%, 5.2%, and 9%, respectively. The declining dividend progress charges are in step with the longer-term outlook for muted earnings progress.

At first of 2021, I used to be bearish on WBA however I revised my place to impartial / maintain in my most up-to-date evaluation on September 2, 2021. Over the 5 ½ months since that score, WBA shares have fallen 7.1% and the entire return is -6.2%.

Looking for Alpha

Efficiency of WBA vs. S&P 500 since my final evaluation on September 2, 2021 (Supply: Looking for Alpha)

The important thing concerns in my September score had been (1) the muted progress outlook, (2) Wall Road consensus score was impartial, and (3) barely bearish consensus outlook from the choices market (the market-implied outlook). Associated to all 3 of those, the consensus 12-month value goal at the moment was just too low to justify the anticipated threat stage for the inventory. The Wall Road consensus value goal, mixed with the dividend, implied anticipated complete 12-month return of 5%-9%. The anticipated annualized volatility calculated from choices (a model of implied volatility) was 30%. As a rule of thumb for a sexy threat / return profile for a inventory, I wish to see anticipated complete return that’s not less than ½ the anticipated volatility. WBA fell far under this threshold.

Whereas most readers might be aware of the Wall Road analyst consensus outlook, many is not going to have encountered the concept it’s potential to extract a consensus view from the choices market. The value of an choice on a inventory displays the market’s consensus estimate of the likelihood that the inventory value will rise above (name choice) or fall under (put choice) a particular stage (the choice strike value) between now and when the choice expires. By analyzing the market costs of name and put choices at a spread of strike costs, it’s potential to calculate a probabilistic value outlook that reconciles the choices costs. That is referred to as the market-implied outlook and represents the implicit consensus view from throughout the choices market. For a extra detailed dialogue of this strategy, see the assets from the Minneapolis Fed and this glorious monograph revealed by the CFA Institute.

I’ve calculated up to date market-implied outlooks for WBA and in contrast these with the Wall Road consensus outlook, as in my earlier evaluation.

Wall Road Consensus Outlook for WBA

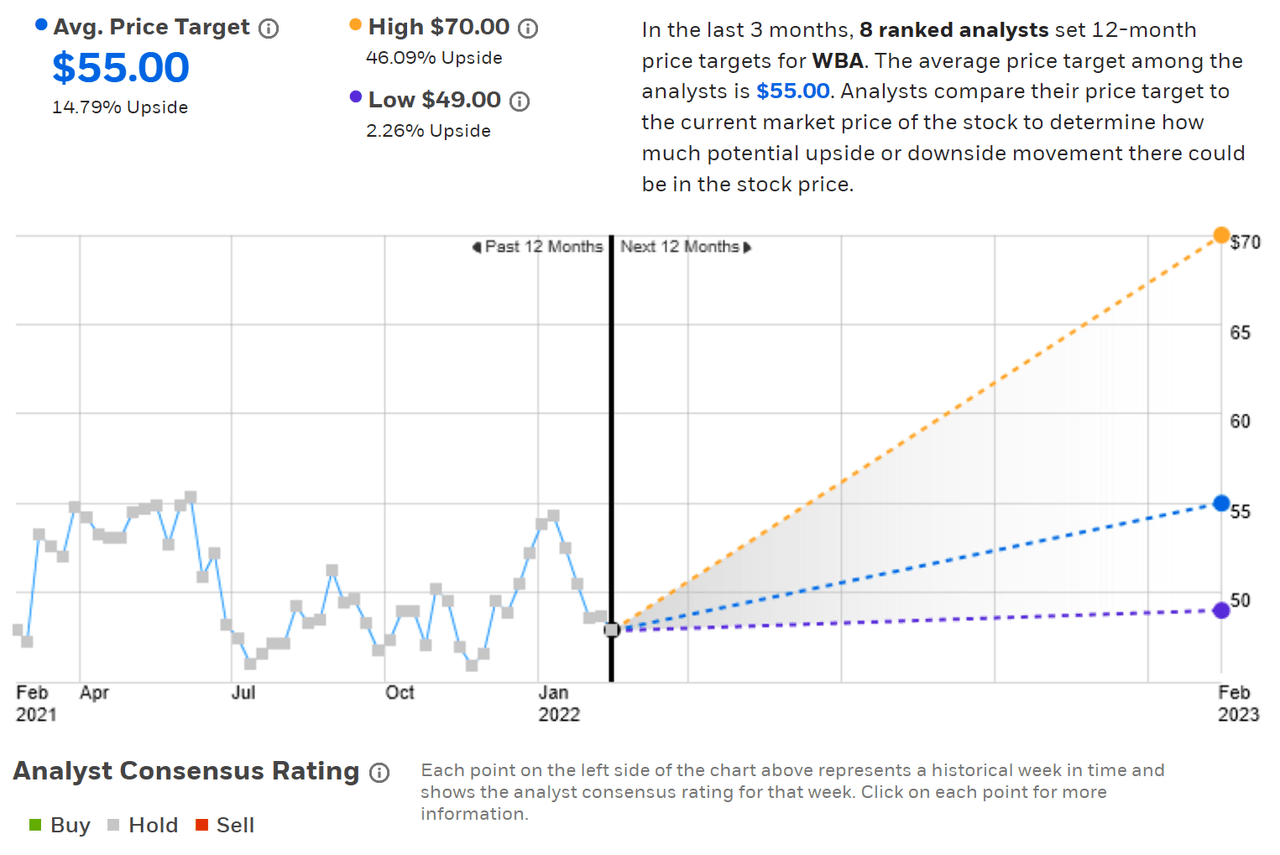

ETrade calculates the Wall Road consensus outlook by combining the views of 8 ranked analysts who’ve revealed scores and value targets for WBA inside the previous 90 days. The consensus score for WBA is impartial and the consensus 12-month value goal is $55, 14.8% above the present share value. For my evaluation in September, the 12-month value goal was $54.11, so the value goal may be very related however the share value has declined since September, leading to a better anticipated value appreciation right this moment. It is usually price noting that the bottom of the person analysts’ 12-month value targets is barely above the present value.

ETrade

Wall Road analyst consensus score and 12-month value goal for WBA (Supply: ETrade)

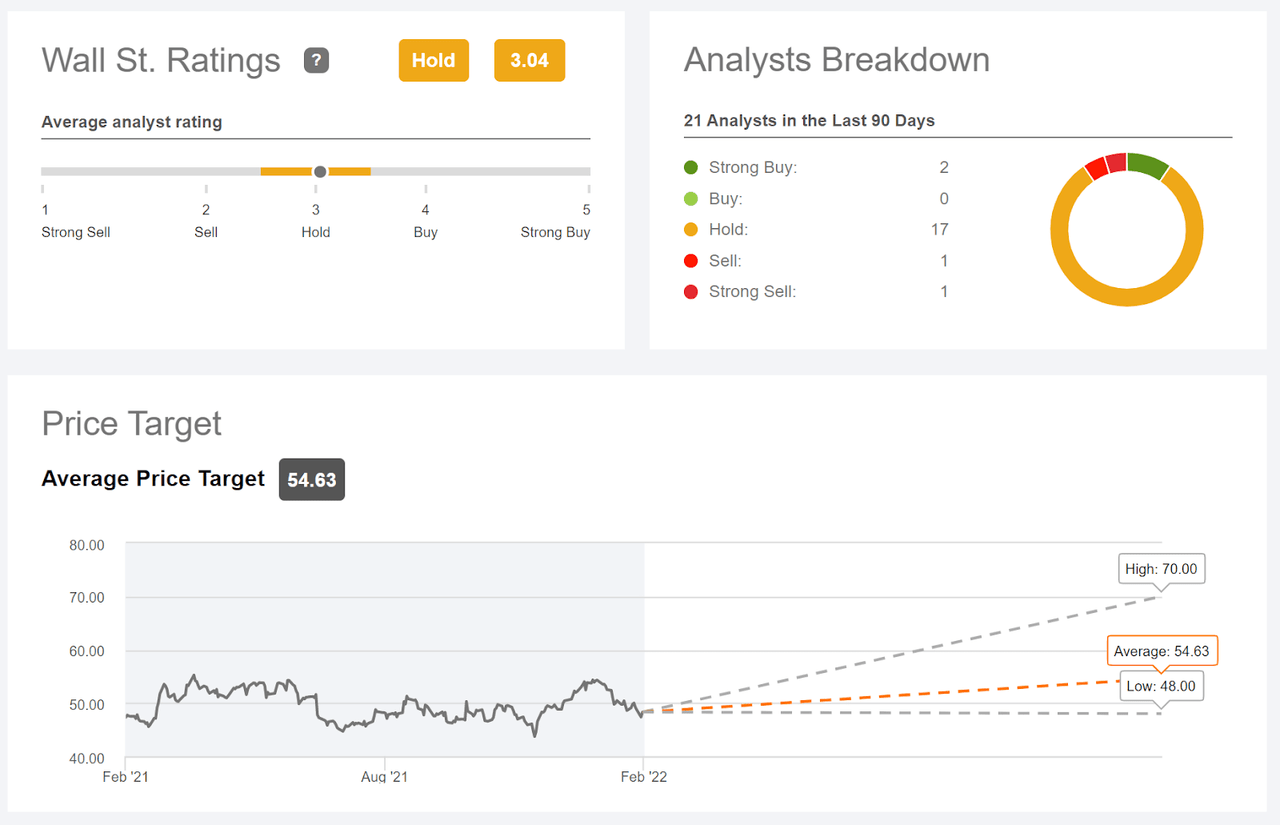

Looking for Alpha’s model of the Wall Road consensus is calculated utilizing scores and value targets from 21 analysts who’ve up to date their views over the previous 90 days. The consensus score is impartial and the consensus 12-month value goal is $54.63, very near the ETrade worth (14.1% above the present share value).

Looking for Alpha

Wall Road analyst consensus score and 12-month value goal for WBA (Supply: Looking for Alpha)

Having a consensus score of impartial and an anticipated 12-month complete return of greater than 18% appears considerably unusual. My finest interpretation is that the analysts consider that the shares are oversold (the share value has fallen 12% from highs in mid-January), in order that the shares have some upside regardless of the muted longer-term progress outlook.

Market-Implied Outlook for WBA

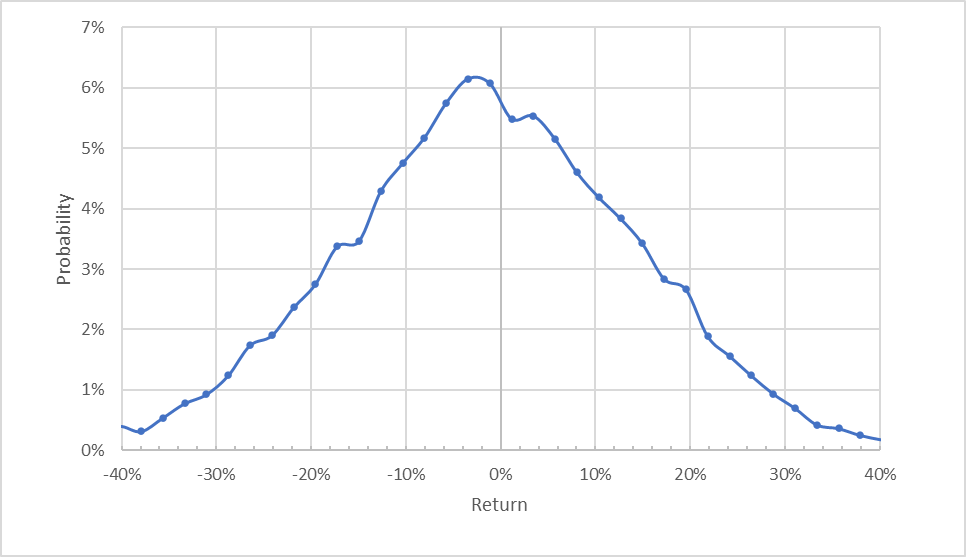

I’ve calculated the market-implied outlook for WBA for the 4-month interval from now till June 17, 2022 and for the 11.1-month interval from now till January 20, 2023 utilizing choices that expire on these dates. I chosen these two expiration dates to supply a view to the center of 2022 and thru the yr.

The usual presentation of the market-implied outlook is a likelihood distribution of value return, with likelihood on the vertical axis and return on the horizontal.

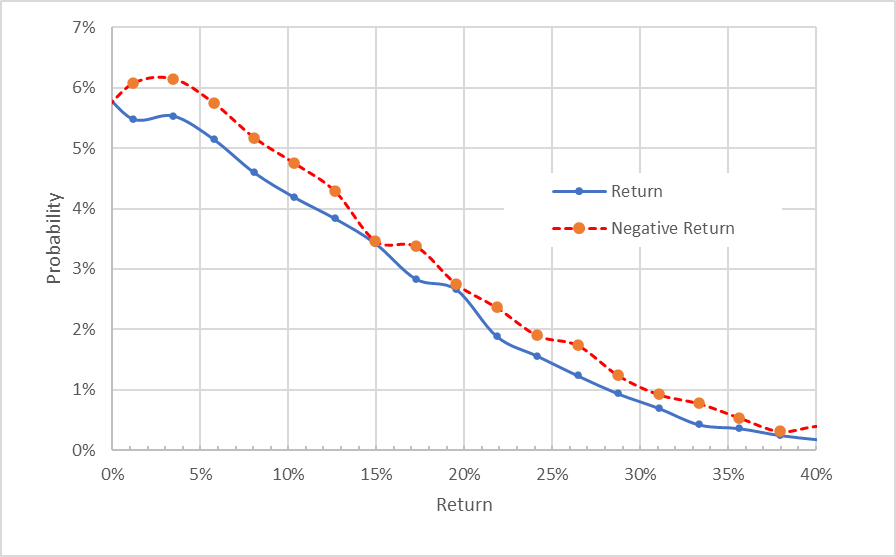

Geoff Considine

Market-implied value return possibilities for WBA for the 4-month interval from now till June 17, 2022 (Supply: Creator’s calculations utilizing choices quotes from ETrade)

The market-implied outlook to June seventeenth is mostly symmetric, though the height likelihood outcomes are barely tilted to favor unfavorable value returns. The utmost likelihood corresponds to a value return of -3%. The annualized volatility calculated from this distribution is 31.5%, very near the 30% anticipated volatility that I calculated in September.

To make it simpler to immediately examine the chances of unfavorable and optimistic returns of the identical magnitude, I rotate the unfavorable return aspect of the distribution in regards to the vertical axis (see chart under).

Geoff Considine

Market-implied value return possibilities for WBA for the 4-month interval from now till June 17, 2022. The unfavorable return aspect of the distribution has been rotated in regards to the vertical axis (Supply: Creator’s calculations utilizing choices quotes from ETrade)

This view highlights the small however persistent elevated possibilities of unfavorable returns relative to optimistic returns of the identical dimension (the pink dashed line is persistently above the strong blue line). Idea predicts that the market-implied outlook ought to have a unfavorable bias as a result of risk-averse buyers are inclined to pay greater than truthful worth for draw back safety. There is no such thing as a strong technique to confirm that such a bias exists for any given inventory or index. Contemplating this potential bias, nonetheless, signifies that the perfect interpretation for a slight unfavorable tilt within the market-implied outlook is that the view is impartial.

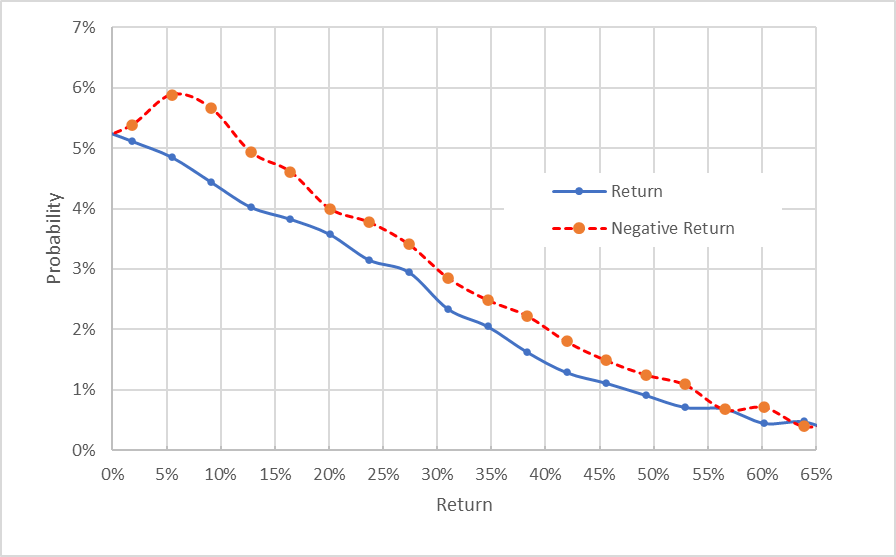

Searching 11.1 months to January 20, 2023, the market-implied outlook may be very related, albeit with a barely extra pronounced tilt favoring unfavorable value returns. The height likelihood corresponds to a value return of -5.5% and the anticipated (annualized) volatility is 31.4%. There’s subjective judgment as to when the unfavorable tilt begins to look bearish. I interpret this outlook as impartial to barely bearish.

Geoff Considine

Market-implied value return possibilities for WBA for the 11.1-month interval from now till January 20, 2022. The unfavorable return aspect of the distribution has been rotated in regards to the vertical axis (Supply: Creator’s calculations utilizing choices quotes from ETrade)

The 4-month and 11.1-month market-implied outlooks inform a constant story. The view to the center of 2022 is impartial, shifting to very barely bearish for the total yr. The anticipated volatility is about 31.5%.

Abstract

WBA is in a difficult transition interval as the corporate tries to maintain tempo with adjustments throughout the healthcare business. The market judges the corporate as being in decline, with the market cap declining 40% over the previous 5 years. The earnings progress outlook isn’t very encouraging. On the present value, the shares look fairly low cost, however the market has not been favoring corporations with low-growth outlooks. WBA will proceed to get some consideration from revenue buyers due to the 4% yield and Walgreens is a Dividend Aristocrat, with a protracted historical past of sustaining and elevating its dividend. The Wall Road consensus score on WBA is impartial, with a consensus value goal that suggests an 18% complete return over the subsequent yr. This anticipated return is larger than ½ the anticipated annualized volatility (31.5%), which suggests a typically favorable risk-return tradeoff. The market-implied outlook is impartial to mid-2022 and impartial to barely bearish for the total yr. I’m sustaining my impartial score on WBA, though a coated name technique can basic substantial revenue between the dividend yield and the decision choice premium.