Nikada/iStock through Getty Pictures

I final wrote about Broadcom Inc. (NASDAQ:NASDAQ:AVGO) in April 2021, or 17 months in the past. It has been a pillar in my portfolio, producing an 18% return then and outperforming the general market by 21%.

In my final article, I gave Broadcom a maintain (impartial) ranking, stating that:

The market is aware of about Broadcom’s progress potential, and its shares are presently valued accordingly. Almost all of Broadcom’s valuation metrics are at all-time highs. PE ratio at 53.69. PS ratio at 7.64. PEG ratio at ~2.

Based mostly on these metrics and a DCF evaluation, I give Broadcom a impartial ranking as I do not see an excellent entry level at these valuations.

– Keyanoush, April, thirtieth, 2021

Broadcom has been part of my low-volatility portfolio for over two years, and it is carried out a implausible job over this timeframe.

On the finish of my article, even after anticipating the expansion charges of the industries wherein Broadcom operates, I used to be very cautious about giving it a constructive ranking due to heightened semiconductor threat and valuation.

Introduction & Thesis

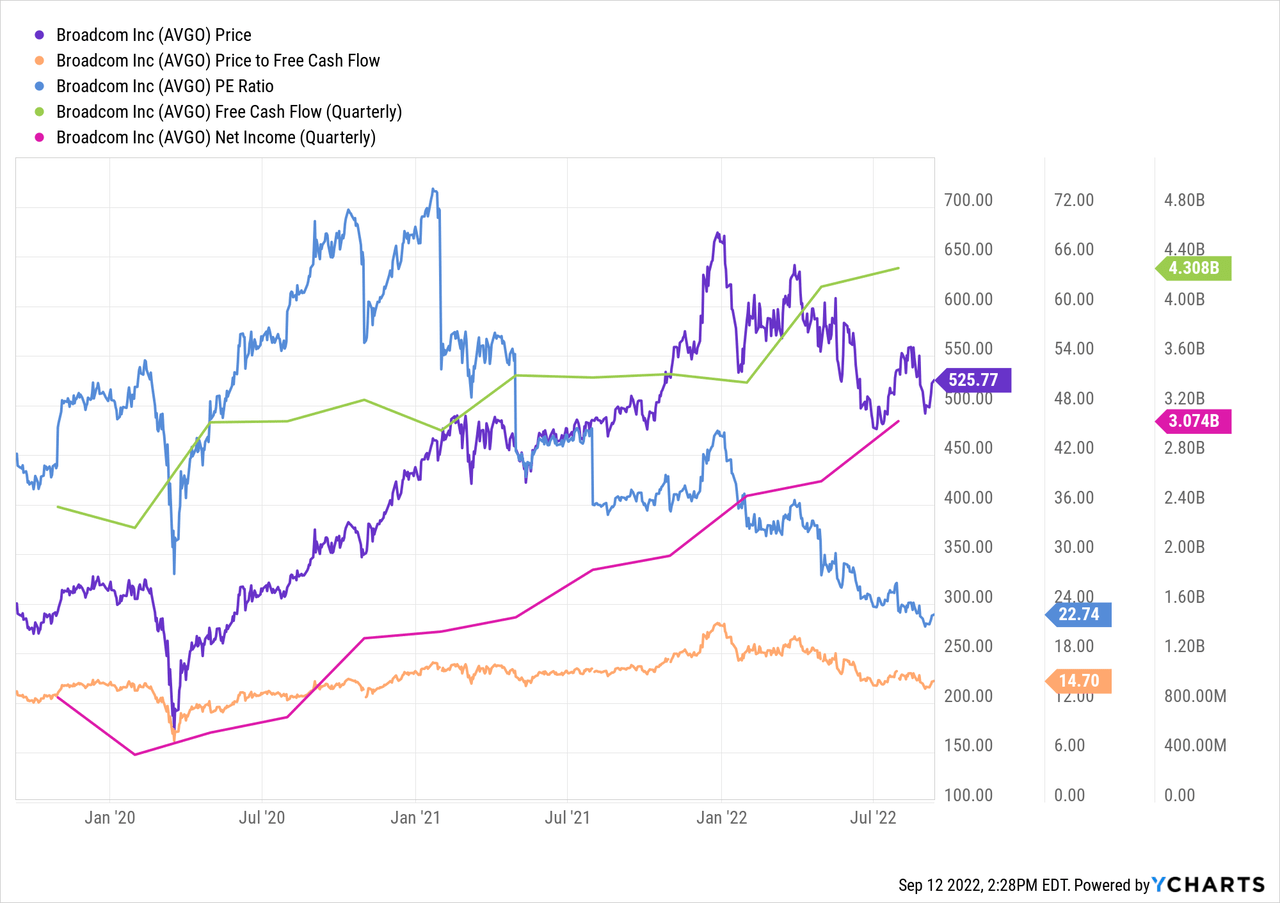

Broadcom’s enterprise has been rising during the last 17 months. Earnings growth pushed valuations down though the corporate’s share value elevated.

From December 2020 till now, Broadcom greater than doubled its internet earnings, which decreased its P/E ratio from 60 in 2020 to 23 now. Worth to FCF (free money circulation) decreased from 14.21 to 12.8 over the identical timeframe.

The broad semiconductor downturn affected Broadcom lower than many different distributors on this sector. Final yr, the utmost drawdown of the iShares Semiconductor ETF (SOXX) was 39%. Broadcom’s most drawdown over the identical interval was 28%.

Broadcom has an intensive product portfolio that’s, to a big extent, not depending on end-consumer demand. Its contracts with OEMs are, by design, non-cancellable, which suggests its backlog will not be liable to massive cancellations.

Hock Tan famous: “…our backlog and our phrases are very clear. We don’t enable cancellation on our backlog.”

Broadcom’s largest end-consumer buyer is Apple (AAPL), whose iPhones are within the premium class, which wasn’t affected as a lot by dwindling demand as was the remainder of the smartphone market. The premium smartphone section appears extra resilient to the market downturn and financial misery than the final smartphone market. IDC expects the premium section even to proceed rising. This fall of 2022 is all the time a positive quarter, with Christmas in entrance of the door and a brand new iPhone launch.

I preserve a large place in Broadcom, however stay cautious with worldwide semiconductor momentum dwindling.

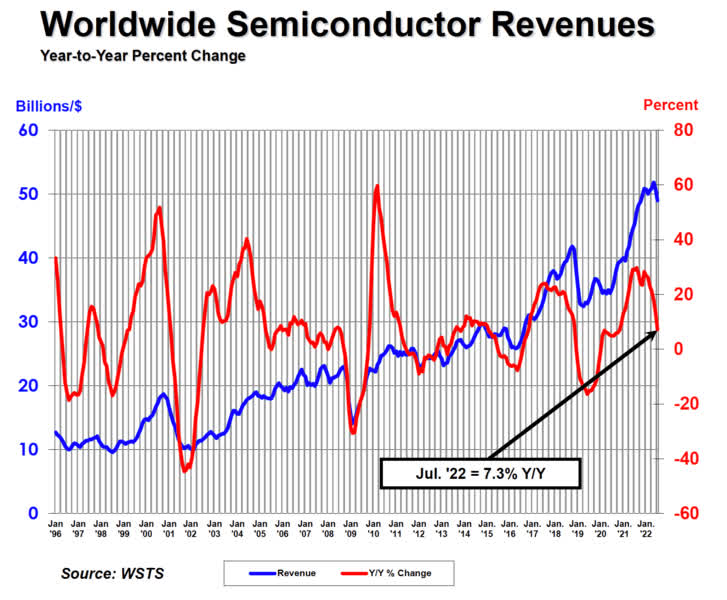

Semiconductor Market Downturn

The semiconductor market is cooling down. The macroeconomic surroundings decreased demand for luxurious items throughout the board. Some outliers embody Samsung’s foldable telephone lineup and the high-end smartphone section.

But, the broader semiconductor business is experiencing bloating stock numbers and the final concentrate on enhancing working capital as a result of lower-than-expected client demand.

I mentioned this subject in additional element once I wrote an evaluation about Qorvo (QRVO) – Qorvo – Round The Candy Spot – and about Skyworks (SWKS) – Skyworks Options: Low-cost? Sure; Low-cost Sufficient? Possibly

International Foundries warned buyers that they count on capability utilization to fall within the yr’s second half. Qorvo admitted that it wrongly estimated demand for wi-fi options within the smartphone section, which led to impairment prices in its latest quarter. Skyworks’s scenario has been higher as a result of a relentless demand from Apple, which makes up almost 60% of Skyworks’ income.

We’re nonetheless within the early innings of the semiconductor market downturn. The results are slowly transitioning all through the business and hitting totally different elements at totally different occasions.

Worldwide Semiconductor Revenues (WSTS)

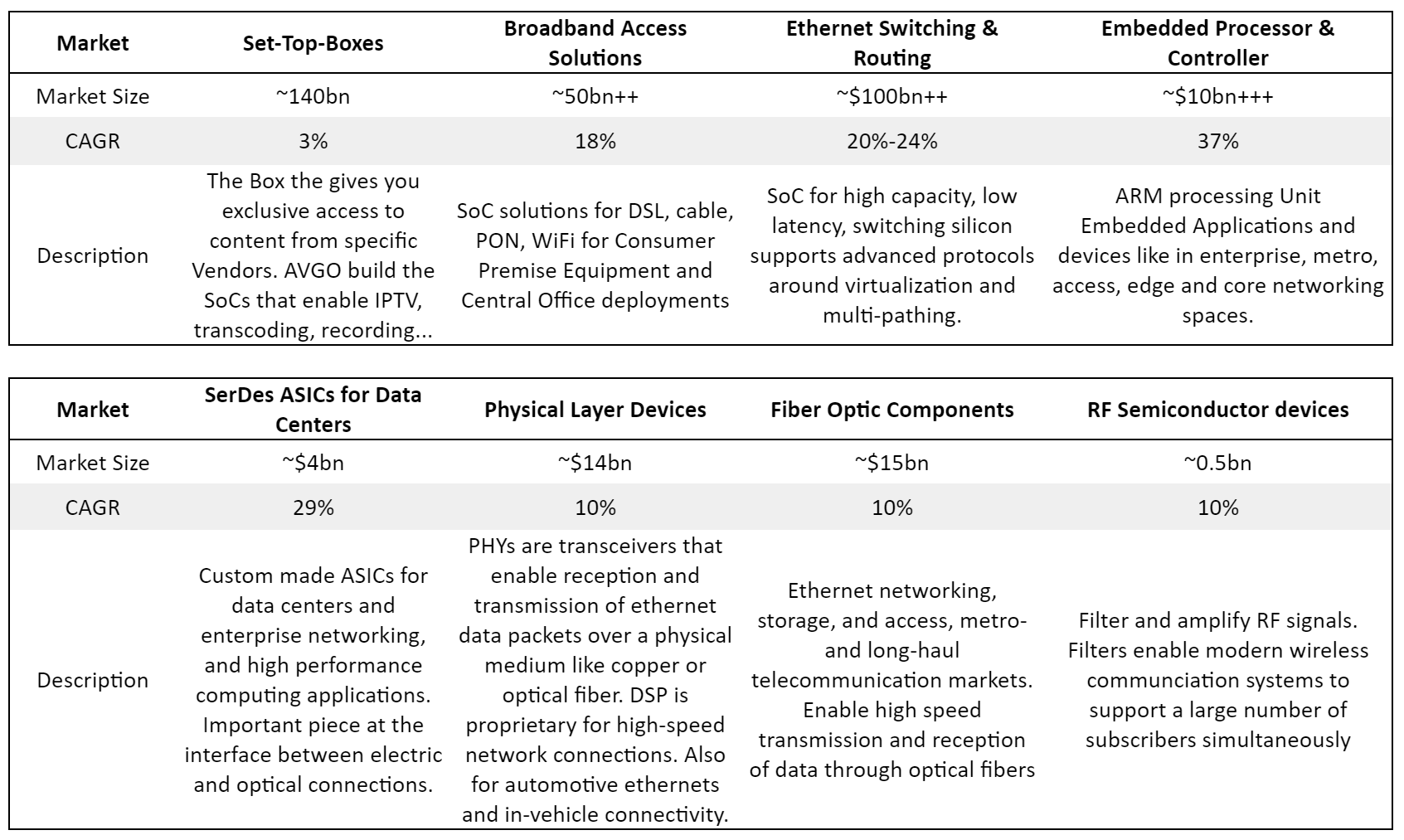

Broadcom has a slight edge as a result of its broad portfolio. Whereas it experiences some buyer focus, Apple and Broadcom’s prime 5 prospects make up 20% and 35% of its income, respectively. Its product portfolio covers industries that aren’t tight to the tip shoppers, like knowledge facilities, enterprise options, the telecom market, and embedded networking purposes.

Keyanoush’s Compilation of Broadcom’s Market Phase (Broadcom Annual Report)

Within the desk above, you see the markets wherein Broadcom operates. Apart from the Set-Prime Packing containers section, every section has a progress fee larger than 10% over the subsequent 5 years.

There will definitely be a slowdown within the progress charges of every section by way of 2022 and 2023, however total, Broadcom’s broad product portfolio appears to be like promising.

Dangers

Apple’s provide and licensing agreements with Broadcom finish in 2023, and we’re dealing with some uncertainty about whether or not Apple is already in a position to produce its WiFi and Bluetooth chips in-house.

In that case, we may see Broadcom’s Semiconductor section take a success. 20% of Broadcom’s income outcomes from its provide and licensing agreements with Apple. Apple would rely extra on Broadcom’s licenses and fewer on the provision of latest chips. The transition will probably be attention-grabbing. I would not be stunned if Apple’s contribution to Broadcom’s income is minimize in half.

The semiconductor tremendous cycle involves an finish. Although Broadcom’s backlog stays stable, I do not count on this development to be sustainable all through 2023 when hyperscalers, OEMs, and telecom cut back their CAPEX.

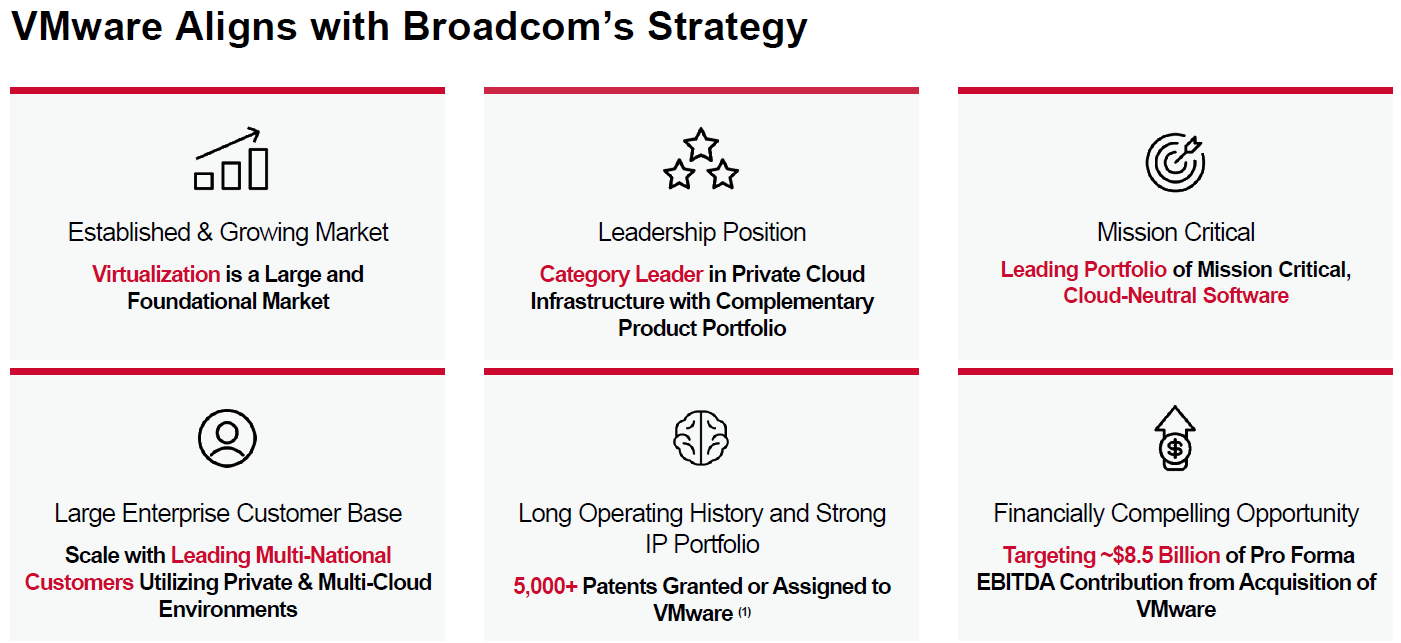

VMWare Acquisition

VMware (VMW) is a superb firm within the virtualization area. I work within the telecom business, the place it repeatedly crosses my path. Main telecom suppliers use VMware virtualization choices to construct their digital RAN platforms.

But, I noticed uncertainty round this deal. VMware grows a lot slower than Broadcom’s semiconductor enterprise, and its choices deviate from Broadcom’s. Possibly a dialogue inside the remark part helps to carry mild into the darkness.

Broadcom’s CEO has a monitor report of making worth from mergers. They’ve carried out so with LSI, Broadcom, Brocade, CA Tech, and lately Symantec.

Broadcom VMware Synergies (Broadcom)

VMware has an EBITDA of $3bn, which is $5.5bn under the $8.5bn Professional Forma contribution Hock Tan confirmed to legitimize the merger. VMware’s complete income is $10.7bn with $2.2bn COGS, $5bn in SG&A and $3bn in R&D bills.

Essentially the most vital alternative may very well be the Telcos, with whom Broadcom already has shut ties. However even once we take into account that Hock Tan can cut back SG&A realistically by half to $2.5bn, we’re nonetheless lacking these additional $3bn.

Broadcom will not be very clear about how they’d generate these synergies and wherein space they lie. The uncertainty, in addition to the quantity of leverage and dilution Broadcom is including, results in a discount in my ranking.

Outlook

The short-term outlook is murky at finest. As mentioned beforehand, the semiconductor market is experiencing a downturn. Broadcom has been much less affected, however I count on progress charges to fall in 2023.

Utilizing this data and inserting them into a reduced money circulation (“DCF”) evaluation can present us with an outlook on Broadcom’s progress potential.

Broadcom simply ended the third quarter, which has been fairly sturdy. For the yr 2022, I used a progress fee of 16%, which places Broadcom’s income at ~$32bn. For 2023, 2024, 2025, and 2026 I used 10%, 5%, 10%, and 10% as progress charges respectively.

Curiosity bills are a slight fear of mine. With almost $40bn in long-term debt, Broadcom is paying virtually $2bn in curiosity. These are my tough unlevered FCF projection for the subsequent 5 years.

Unlevered Free Money Move Broadcom – Projected till 2026 (Keyanoush)

Inserting these numbers into our EBITDA a number of DCF evaluation, we get the next projections.

DCF Evaluation – Broadcom (Keyanoush)

With the expansion charges, improve in working capital, and high-interest funds, the DCF evaluation exhibits a comparatively impartial outlook. The variance of this projection is large. If Broadcom experiences a valuation growth, the returns may very well be favorable.

Conclusion

Broadcom is a combined bag. Broadcom sells its merchandise throughout numerous industries, most of which aren’t straight tight to finish client demand. This might’ve led to Broadcom’s outperformance in opposition to its friends.

The market downturn may have delayed results on Broadcom. Broadcom is processing a >$60bn deal to purchase VMware, offering little steering for buyers about its impression on margins and the way VMware could be newly structured within the mixed firm.

Broadcom operates in lots of progress segments, and an space that I particularly like is its customized silicon accelerators. Broadcom designs and manufactures ASICs for the information heart and transport and routing section. Basic computing is inherently inefficient in doing advanced task-specific calculations. An ASIC does one kind of calculation or course of exceptionally effectively, thus lowering energy consumption and processing duties a lot sooner. Designing and manufacturing ASICs requires area experience inside the space wherein they’re deployed, which creates dependencies on Broadcom.

Based mostly on my DCF evaluation and a murky business outlook, I’ve a impartial stance on Broadcom’s inventory efficiency. Broadcom stays part of my low-volatility portfolio, as it is a money circulation producing and dividend-paying firm with a steady outlook.

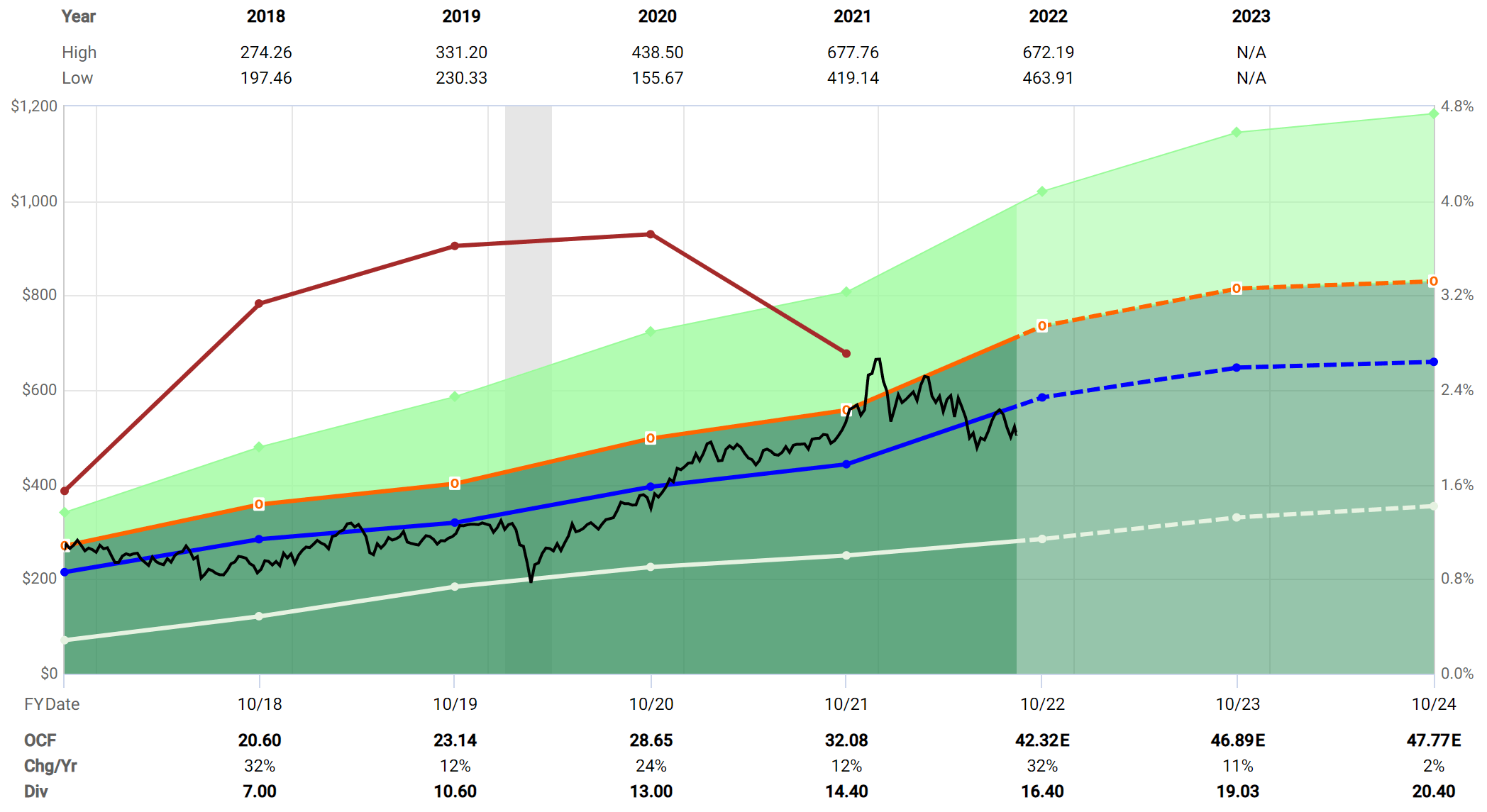

Broadcom Fastgraphs Historic (Fastgraphs)

Traditionally, Broadcom is buying and selling proper round its historic valuation. The margin of security of investing in Broadcom on the present valuation and the macroeconomic surroundings is meager.

This text ought to solely be thought to be step one in your due diligence course of.

I all the time welcome constructive criticism and open discussions. Please be at liberty to remark about my calculations and/or sources that I exploit in my articles.