Walgreens Boots Alliance, Inc. (NASDAQ: WBA) has been busy enhancing its capabilities in healthcare supply recently, by varied initiatives together with M&A offers. After being hit by the pandemic-related disruption initially, buyer site visitors recovered as folks flocked to Walgreens shops for coronavirus checks and vaccination. The excessive demand for COVID-related gadgets, together with booster dose and at-home check kits, resulted in a file improve in same-store gross sales.

The Inventory

After slipping to multi-year lows, Walgreens’ inventory made regular features early final yr although the momentum waned within the second half. It prolonged the downturn into 2021 and principally traded under the $50-mark. Market watchers, generally, are bullish on WBA’s prospects, which is anticipated to achieve about 15% within the 12-month interval.

Learn administration/analysts’ feedback on Walgreeens’ Q1 2022 earnings

Nevertheless, it’s advisable to attend till the upcoming earnings launch earlier than investing. Walgreens has hiked the dividend frequently through the years. It presently presents a yield of 4.2%, which is far larger than the S&P 500 common. Contemplating the corporate’s promising long-term prospects and favorable valuation, WBA is a perfect possibility for earnings buyers.

From Walgreen’s This fall 2021 earnings name transcript:

“Trying forward of 2022, contemplating the macro uncertainties, we are going to proceed to take prudent working technique as all the time. From what we now have discovered from previous success, we consider that holding a prudent and regular method in each day operation is the golden normal for the fintech enterprise when macro uncertainties come up. After all of the rectification in 2021, we count on to see a a lot clearer regulatory framework for the fintech trade in 2022, which ought to permit trade members to be extra targeted on long-term enterprise improvement.”

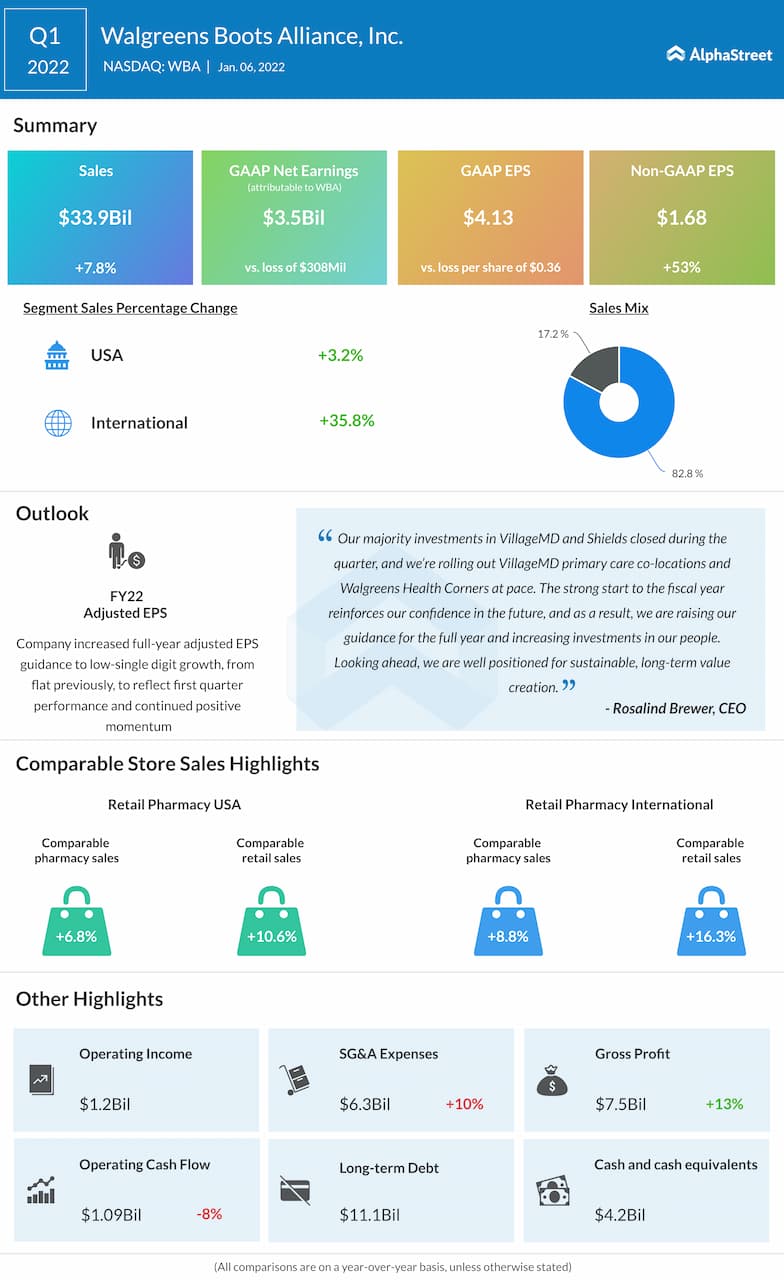

Monetary Efficiency

Apparently, Walgreen reported stronger-than-expected earnings and revenues because the onset of the virus disaster. It began the brand new fiscal yr on an upbeat notice, reporting a 53% development in adjusted earnings for the primary quarter. The spotlight of the quarter was a 36% development within the worldwide enterprise, which far outperformed the core home phase.

Retail comparable retailer gross sales elevated in double digits in the course of the three-month interval. At $34 billion, complete revenues had been up 8% year-over-year. The important thing numbers additionally surpassed the market’s projections. Buoyed by the constructive momentum, the administration raised its full-year 2022 earnings outlook. When the corporate reviews second-quarter outcomes on March 31 earlier than the opening bell, the market will probably be searching for a ten% improve in earnings to $1.38 per share, on revenues of $33.4 billion.

Past COVID

In the meantime, there are considerations that gross sales would decelerate as soon as the COVID scenario improves additional and normalcy returns. A pullback in buyer site visitors would weaken comparable retailer gross sales, which doesn’t bode effectively for the corporate’s stakeholders.

Costco bets on robust buyer loyalty to beat COVID blues

In October final yr, the corporate raised its stake in healthcare administration companies supplier VillageMD to 63% by investing $5.2 billion. The deal will permit it to open Village Medicals items at Walgreens shops. In the same deal, it additionally acquired a majority stake in well being administration firm CareCentrix.

Over the previous twelve months, Walgreens’ inventory misplaced about 9% and slipped under its 52-week common. WBA traded barely decrease on Tuesday afternoon.