Sundry Pictures/iStock Editorial through Getty Photos

After we final analyzed Qorvo Inc. (NASDAQ:QRVO), we decided the corporate stood to learn from the 5G wave given its broad portfolio of modern RF options and extremely differentiated semiconductor applied sciences. Qorvo derives nearly all of its income from cellular merchandise (71%), which is closely reliant on Apple (32% of whole income). As well as, Qorvo has additionally received contracts for brand spanking new 5G telephones from Samsung Electronics, Huawei Applied sciences and LG Electronics. Its RF chips are used throughout a number of industries, and we decided on the time that Qorvo had a robust footing in BAW filters, competing with Broadcom and Skyworks.

Whereas Apple is the corporate’s main buyer accounting for 30% of its income, Qorvo has giant income publicity to Asian prospects equivalent to Samsung and main Chinese language smartphone makers which consist for 55% of its revenues in 2021. In comparison with Apple which has already launched its first era of 5G telephones in 2020, the Asian smartphone makers have but to completely roll out their 5G smartphones which we consider presents a possibility for Qorvo.

We analyzed Qorvo’s RF Fusion20 RFFE modules developed to allow 5G assist throughout lower-priced smartphones, by tackling the house constraints. We decided Qorvo had the aggressive benefit in comparison with Qualcomm and Skyworks, given the upper quantity of product benefits of its RF elements. Nevertheless, we decided by way of monetary evaluation that the corporate’s margins are weaker than its rivals, which we consider is because of their giant publicity to mid-tier smartphone makers. General, we see its development supported by its relationships with main mid-tier smartphone makers, that are within the strategy of rolling out 5G telephones.

Progress of 5G To Be Pushed By Asian Smartphone maker Prospects

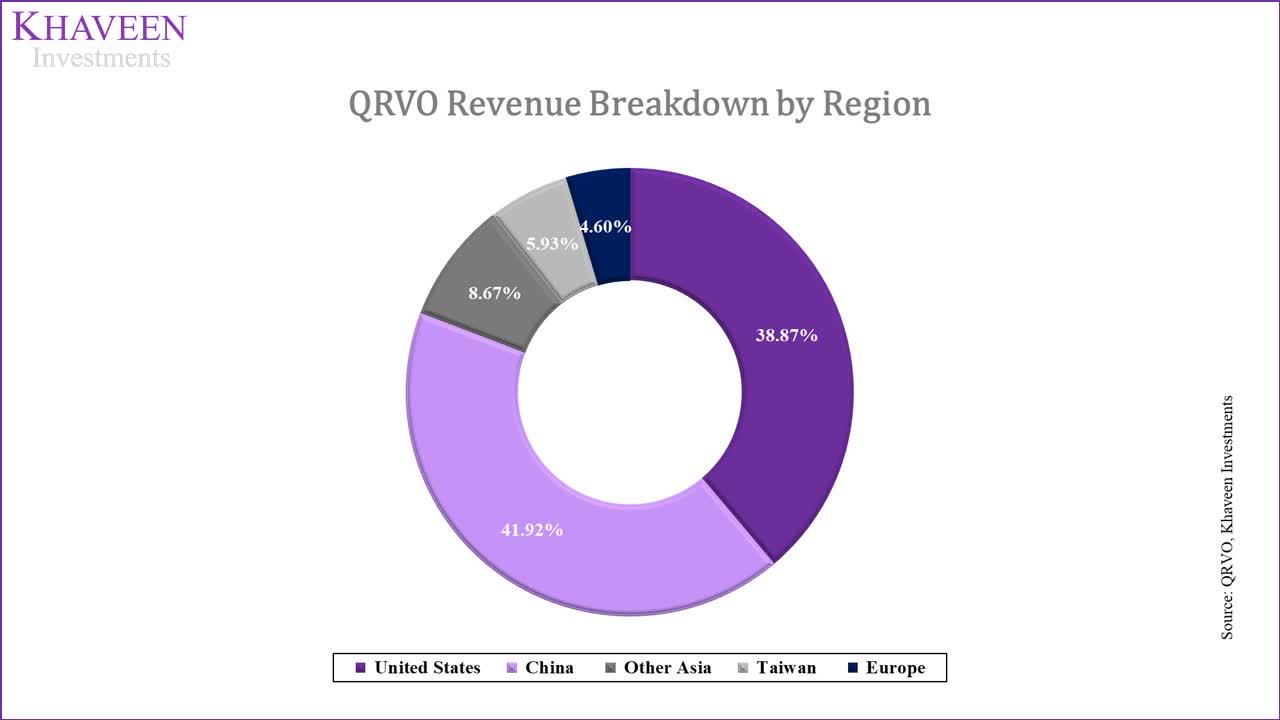

Primarily based on its annual report, Qorvo derives nearly all of revenues from the Asian area at round 55% in 2021. Round 40% of revenues have been from China and trailed the US very carefully. The corporate has ties with main Chinese language smartphone makers together with Xiaomi, Oppo, Vivo and Huawei in addition to Samsung (OTCPK:SSNLF) in Korea. As cited in our earlier evaluation, the highest 5 main smartphone makers account for 82% of the 5G smartphone market as of Q1 2021.

Qorvo

Nonetheless, Apple (AAPL) is the corporate’s largest buyer accounting for 30% of revenues based mostly on its annual report. Apple was additionally the most important 5G smartphone maker with a market share of 34% in Q1 2021. Nevertheless, within the mid-tier 5G smartphone market, the foremost Chinese language smartphone makers equivalent to Vivo, Oppo, Xiaomi in addition to Samsung lead with a market share of 77% mixed in accordance with Counterpoint Analysis.

Additionally, greater than 92% of 5G smartphones are priced above $200 in Q2 2021. Primarily based on IDC’s smartphone market breakdown by value bands, smartphones beneath $200 accounted for practically half of the overall smartphone market. Thus, we consider that this reveals the large alternative for the 5G market to develop within the lower-priced smartphone market. Adoption of 5G of low and mid-tier smartphones is anticipated to proceed rising as these smartphone makers proceed to launch new designs which incorporate 5G connectivity and assist.

We calculated the portion of every smartphone maker’s 5G smartphone shipments as a proportion of their whole shipments within the desk beneath.

Following the launch of the iPhone 12 with 5G assist throughout all fashions, Apple’s 5G smartphone shipments as a % of its whole shipments stood at 26% in 2020. It is usually greater than the market common of 20.2%. Compared, Samsung, Xiaomi and different smartphone makers have a comparatively low proportion of 5G gross sales which we consider presents an enormous development alternative for Qorvo.

|

Smartphone Makers 5G Shipments (‘mln) |

5G Shipments (2020) |

Complete Shipments (2020) |

Shipments Share of Complete % |

|

Apple |

201.1 |

26.0% |

|

|

Oppo |

111.8 |

21.1% |

|

|

Vivo |

108.5 |

21.9% |

|

|

Samsung |

255.7 |

14.7% |

|

|

Xiaomi |

145.7 |

17.0% |

|

|

Others |

508.5 |

31.3% |

|

|

Complete |

1332.7 |

20.2% |

Supply: Technique Analytics, Counterpoint Analysis, Cellular World Stay, Khaveen Investments

We derived the 5-year CAGR of 5G smartphone gross sales by the main smartphone makers based mostly on an estimate of 69% of the overall smartphone market being 5G in 2025 by the IDC which we utilized to all corporations as our assumption. We forecasted Samsung and Xiaomi to have the very best CAGR of 41.3% and 37.3% respectively adopted by Oppo and Vivo however nonetheless at the next CAGR than Apple.

|

Forecast of 5G Shipments by Smartphone Makers |

% of 5G (2020) |

Complete Shipments |

5G Shipments (2020) |

Complete Shipments (2025F) |

% of 5G (2025F) |

5G Shipments (2025F) |

5-Yr CAGR |

|

Apple |

26.0% |

201.1 |

52.2 |

241.5 |

69% |

166.66 |

26.1% |

|

Oppo |

21.1% |

111.8 |

23.6 |

134.3 |

69% |

92.65 |

31.4% |

|

Vivo |

21.9% |

108.5 |

23.8 |

130.3 |

69% |

89.92 |

30.4% |

|

Samsung |

14.7% |

255.7 |

37.6 |

307.1 |

69% |

211.90 |

41.3% |

|

Xiaomi |

17.0% |

145.7 |

24.7 |

175.0 |

69% |

120.74 |

37.3% |

|

Others |

21.1% |

508.5 |

107.1 |

610.7 |

69% |

421.40 |

31.5% |

|

Complete |

20.2% |

1,333 |

269.0 |

1,601 |

69% |

1,104 |

32.6% |

Supply: Technique Analytics, Counterpoint Analysis, Cellular World Stay, IDC, Khaveen Investments

General, we consider that that is important for Qorvo because of its important publicity to the main Asian smartphone makers together with Samsung, Xiaomi, Oppo and Vivo because it derives round half of its revenues from the Asian continent. These smartphone makers dominate the 5G marketplace for mid-tier smartphones and are anticipated to exhibit the very best development charges within the subsequent 5 years as 5G penetrates mid and low-tier smartphone gadgets. As Qorvo caters to those prospects, we consider that it’s poised to learn from its prospects’ continued growth of 5G telephones as an RF provider.

Qorvo’s Built-in RF Fusion20 Enabling Better 5G Adoption

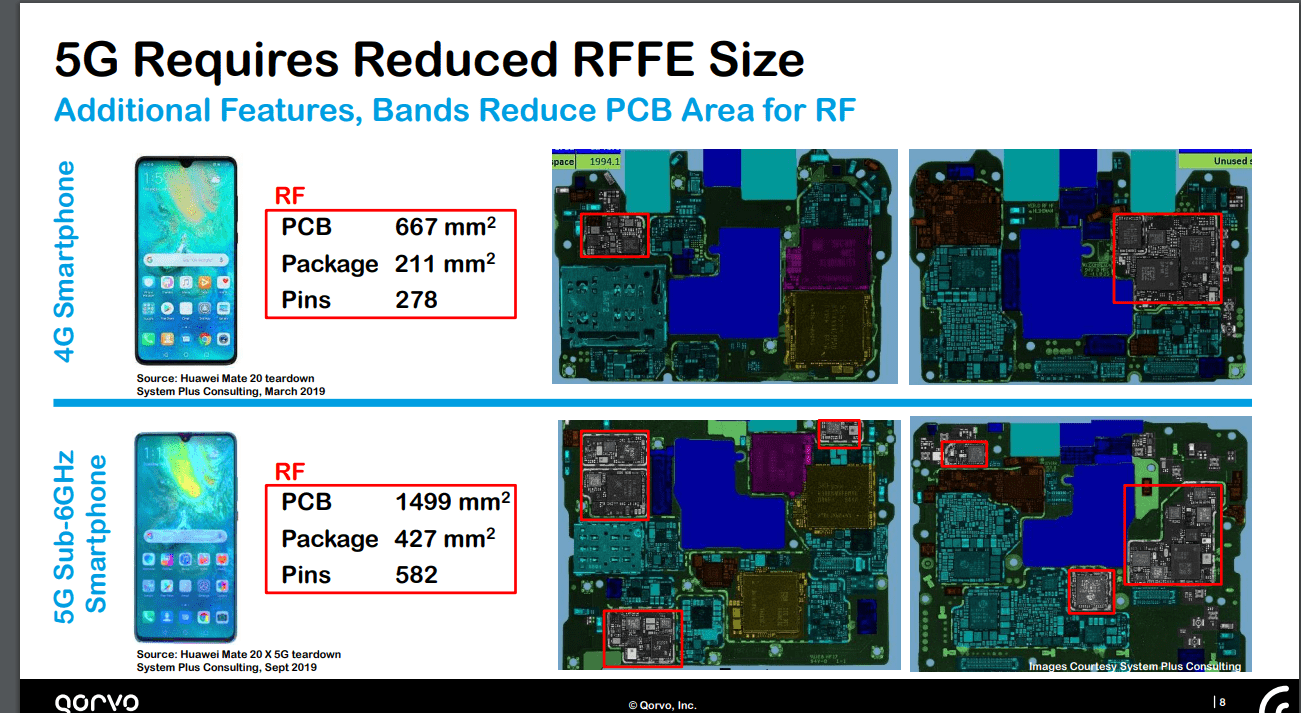

One of many headwinds of the adoption of 5G throughout lower-priced smartphone tiers is the upper value issue related to 5G elements. Based on Technique Analytics, smartphone makers require built-in RFFE merchandise to fulfill house constraints in 5G fashions. Evaluating Huawei’s Mate 20 4G mannequin with its 5G mannequin within the chart beneath from SEMI, the PCB space and package deal dimension for the 5G are greater than twice that of the 4G mannequin.

SEMI

Supply: SEMI

Qorvo has highlighted its dedication to the adoption of 5G throughout all smartphone value tiers within the growth of its RF Fusion20 RFFE modules. It claimed to combine numerous RF elements by combining its “world-class GaAs energy amplifiers, superior BAW multiplexing and built-in RF shielding” in an answer to assist its buyer’s development of low and mid-tier 5G telephones in accordance with the corporate. Qorvo highlighted the mixing of a low-noise amplifier (LNA) which helps to enhance obtain efficiency and connectivity and its RF Shielding that decrease undesirable RFFE elements’ interplay. Its advanced switches additionally allow it to assist each key sub-6GHz frequency band.

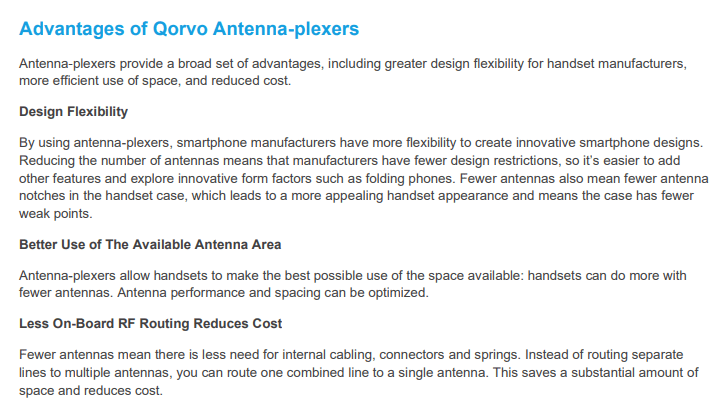

Moreover, the built-in resolution additionally options Qorvo’s antenna-plexers. Based on Cellular Techniques, an antenna catches ‘radio waves and turns them into electrical indicators into cellphone or tv’. It performs a vital position within the growth and deployment of 5G. A 4G smartphone usually wants 4 to eight antennas and therefore 5G will want greater than that. Nevertheless, new traits in smartphone designs equivalent to greater batteries, extra cameras, movement sensing and fingerprint/facial recognition cut back the house out there for extra antennas.

Lowering the necessity for antennas brings two predominant benefits. Firstly, the smartphone designers might have extra modern designs because the restriction turns into fewer for the reason that variety of antennas is decreased. Designers could make the cellphone do extra with optimized antenna spacing. The following one is value financial savings. Because the required antennas develop into fewer, it means there may be much less want for inner cabling, connectors and is derived which save house and cut back prices.

Qorvo

Supply: Qorvo

Evaluating Qorvo in opposition to rivals equivalent to Qualcomm and Skyworks, we analyzed the built-in RFFE modules for these corporations when it comes to their RF elements and their predominant benefit. Qorvo’s Fusion 20 integrates a low-noise amplifier and RF Shielding, which offers a key benefit in higher connectivity and indicators receiving and minimizing undesirable interactions between RFFE elements respectively. Stopping undesirable interactions between RFFE elements permits producers to simplify growth and speed up time to market. Its advanced switches additionally enable it to assist all sub-6GHz frequency bands. Whereas Qualcomm’s built-in RFFE resolution stands out in receiving mmWave because it integrates mmWave antennas in its options.

|

Firm |

RF Elements |

Key Benefit |

|

Qorvo (Fusion20) |

|

|

|

Qualcomm |

|

|

|

Skyworks (Sky5) |

|

Supply: Qorvo, FierceWireless, Skyworks, Omdia

Primarily based on our 5G RF content material development fee of 1.93x derived from our earlier evaluation pushed by greater RF content material necessities to assist larger RF complexities and frequencies of 5G, we projected the RF demand development from Apple and different smartphone makers by way of 2025 assuming 69% of smartphone gross sales are 5G. For Apple, we derived a CAGR of 6.96% and seven.76% for different smartphone makers.

|

Qorvo MP Income Breakdown |

Apple |

Others |

Complete |

|

5G Shipments (2020) |

52.2 |

216.8 |

269.0 |

|

% of 5G (2020) (‘a’) |

26.0% |

19.2% |

20.2% |

|

5G Shipments (2025) |

174.8 |

982.1 |

1156.9 |

|

% of 5G (2025F) (‘b’) |

69.0% |

69.0% |

69.0% |

|

5G RF Content material Enhance (‘d’) |

1.93 |

1.93 |

1.93 |

|

5G Share Enhance (‘c’) |

43.04% |

49.82% |

48.79% |

|

5G RF Content material Progress % (‘e’) |

39.97% |

46.26% |

45.31% |

|

5-Yr CAGR (‘f’) |

6.96% |

7.90% |

7.76% |

*c = b – a

e = [(c x d) + (1 x (1-c)]-1

f = (1+e)^(1/5)-1

Supply: Qorvo, Khaveen Investments

With this, we projected Qorvo’s Cellular Merchandise Phase revenues in FY2022 based mostly on its prorated Q1 to Q3 outcomes adopted by our derived RF forecast CAGR past that and tapering by 0.5% per 12 months as a conservative estimate.

|

Qorvo Cellular Merchandise Phase ($ mln) |

2020 |

2021 |

2022F |

2023F |

2024F |

2025F |

2026F |

|

Apple Revenues |

791 |

857 |

1,072 |

1,147 |

1,221 |

1,293 |

1,364 |

|

Apple RF Income Progress % |

8.3% |

25.1% |

6.96% |

6.46% |

5.96% |

5.46% |

|

|

Others Revenues |

1,607 |

2,000 |

2,501 |

2,699 |

2,899 |

3,099 |

3,297 |

|

Others Progress % |

24.5% |

25.1% |

7.90% |

7.40% |

6.90% |

6.40% |

|

|

Complete Income |

2,398 |

2,857 |

3,573 |

3,846 |

4,119 |

4,392 |

4,661 |

|

Complete Progress % |

19.1% |

25.1% |

7.6% |

7.1% |

6.6% |

6.1% |

Supply: Qorvo, Khaveen Investments

Thus, along with its publicity to main mid-tier Asian 5G smartphone makers, we consider that the corporate’s dedication is highlighted by the event of its Fusion20 built-in RFFE modules which combine numerous RF elements to take care of the prices and house constraints headwinds related to introducing 5G connectivity for low to mid-tier smartphones. Nevertheless, on the similar time, we additionally consider that Qualcomm and Skyworks supply a lovely built-in RF resolution which can pose a aggressive menace to Qorvo.

Superior Margins of RF Phase Than IDP Phase

When it comes to working margins, the corporate’s Cellular Merchandise phase has superior margins to its Infrastructure and Protection Merchandise phase. In 2021, the MP phase had working margins of 35.3% in comparison with 24.5% of the IDP phase based mostly on its annual report. The IDP phase consists of basic analog merchandise equivalent to energy semiconductors and MEMs.

|

Phase Working Margins % |

Cellular Merchandise |

Infrastructure and Protection Merchandise |

|

Income |

2,856 |

1,158 |

|

Working Revenue |

1,008 |

283.5 |

|

Working Margins |

35.3% |

24.5% |

Supply: Qorvo

The superior margin of MP highlights the comparatively concentrated RF market with the highest 5 accounting for nearly 80% of the market share of RF semiconductors. We consider this means the comparatively weaker bargaining energy of consumers in comparison with the analog market.

Nevertheless, as compared with rivals, the corporate’s margins are weaker because it has decrease market shares than Murata, Broadcom and Skyworks and decrease scale. Its gross margins have a 5-year common of 41% which is beneath the typical of fifty.8% as properly decrease than common internet and FCF margins. Its SG&A as a % of income is the very best amongst rivals.

|

Firm |

Gross Margins – 5 yr Avg |

Web Revenue Margins – % 5 yr Avg |

FCF Margins – 5 yr Avg |

R&D as % of Income – 5yr Avg |

SG&A as % of Income -5yr Avg |

|

Qorvo |

41% |

6.06% |

19.17% |

14.85% |

14.18% |

|

Skyworks |

49.45% |

26.15% |

19.56% |

11.21% |

5.95% |

|

Murata (OTCPK:MRAAY) |

37% |

12.78% |

0.09% |

6.69% |

13.80% |

|

Qualcomm |

59% |

10.49% |

21.30% |

23.68% |

9.79% |

|

Broadcom |

68% |

19.03% |

40.20% |

19.71% |

6.09% |

|

Common |

50.79% |

14.90% |

20.06% |

15.23% |

9.96% |

Supply: Firm Information, Khaveen Investments

Although, its R&D and SG&A spending as a % of income have been reducing barely on a 10-year common in comparison with its 5-year common as the corporate’s scale grew.

|

Qorvo |

5-Yr Common |

10-Yr Common |

|

R&D as % of income |

14.85% |

15.96% |

|

SGA as % of Income |

14.18% |

14.47% |

Supply: Qorvo

We count on its margins to proceed to enhance by way of 2026 as the corporate’s scale improves. General, the corporate’s RF phase which isn’t solely its largest phase however can also be extra worthwhile with greater margins. We attribute this to the corporate’s established market positioning within the comparatively concentrated RF semiconductor market in comparison with the analog market.

Qorvo, Khaveen Investments

Danger: Apple In-Home Growth

Whereas the corporate has buyer relationships with the world’s main smartphone markers, the corporate’s largest buyer, Apple, nonetheless represents round 30% of revenues. This highlights its focus danger from a single buyer. Moreover, Apple has been reportedly in search of to develop RF chips in-house which might influence its future enterprise with the corporate. In comparison with rivals, Qorvo has the second-highest income publicity to Apple at 30% trailing behind Skyworks at 59% of revenues. Comparatively, Broadcom and Qualcomm have a broader enterprise mannequin and are bigger than Qorvo. All in all, this might place Qorvo in danger if Apple decides to develop its in-house capabilities.

|

Firm |

Contribution of Apple Income as % of Complete Income |

|

Skyworks (SWKS) |

|

|

Qorvo |

30% |

|

Broadcom (AVGO) |

|

|

Qualcomm (QCOM) |

Supply: Skyworks, Qorvo, Broadcom, Qualcomm, Murata

Valuation

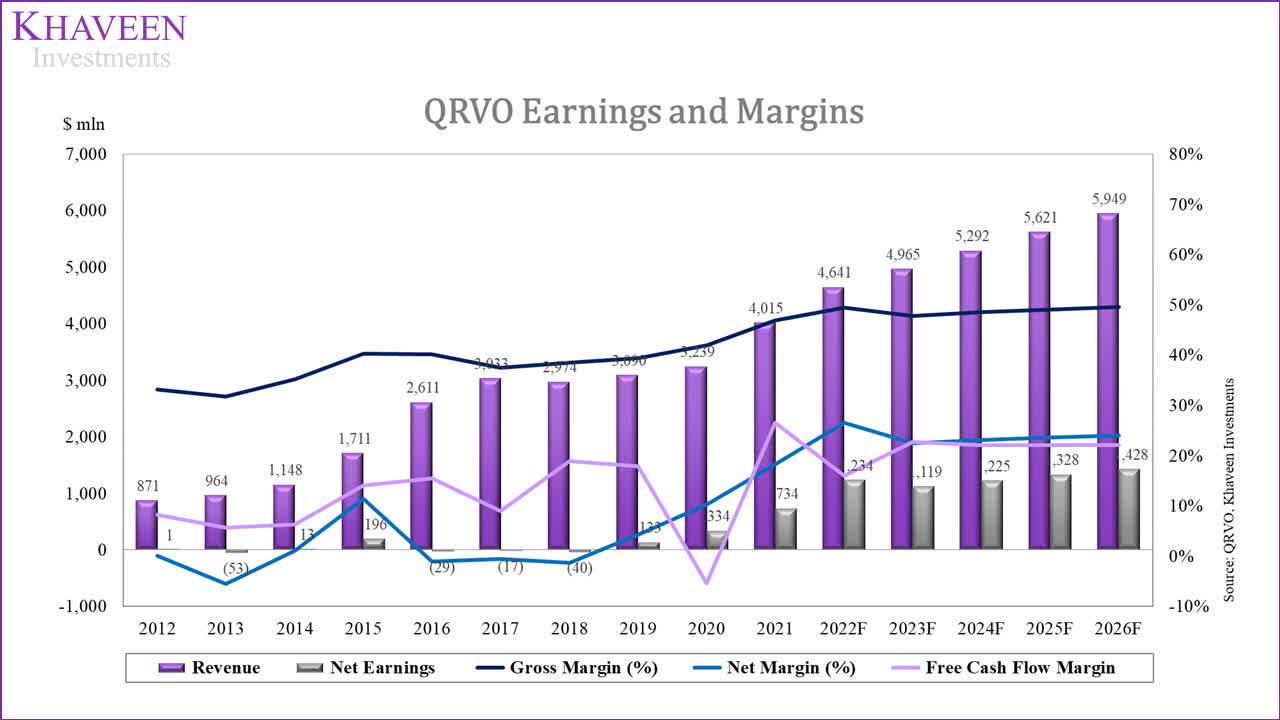

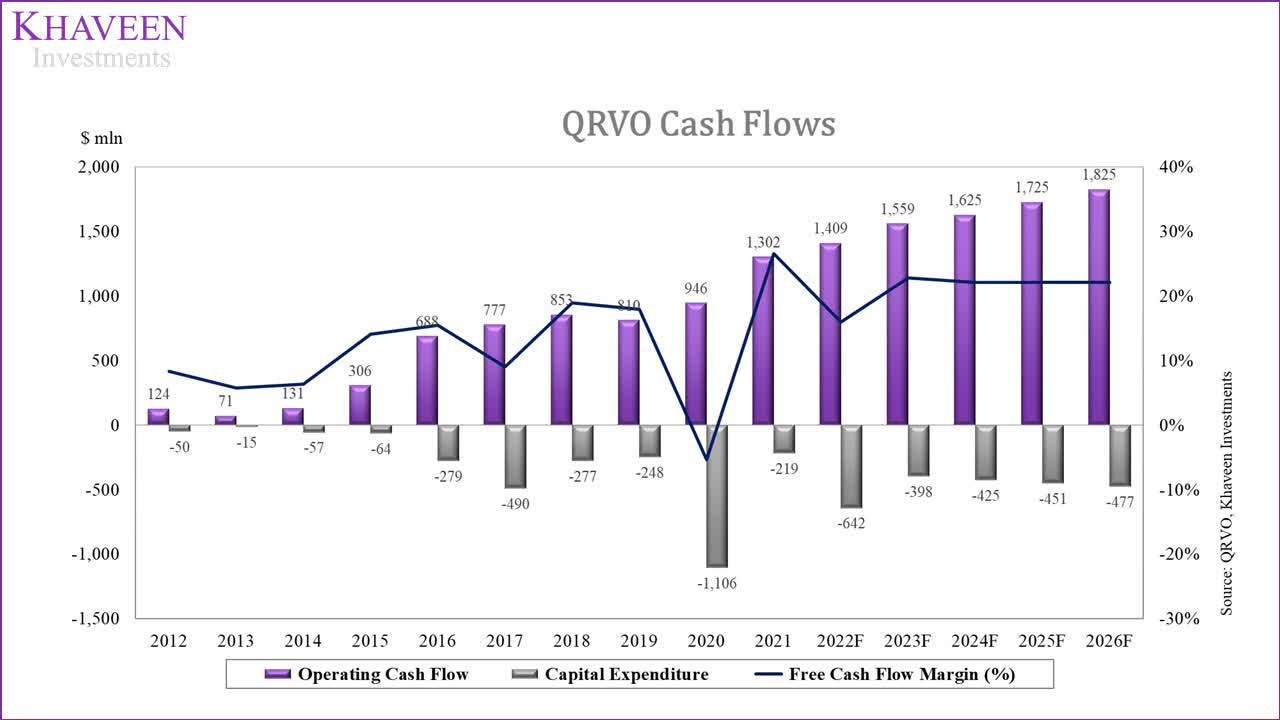

The corporate has had a median free money movement margin of 14.18% for the previous 5 years. The corporate acquired 4 corporations within the fiscal 12 months 2020, i.e. Lively-Semi, Cavendish, Customized MMIC and Decawave with Decawave standing virtually 50% of the entire acquisition quantity.

Qorvo, Khaveen Investments

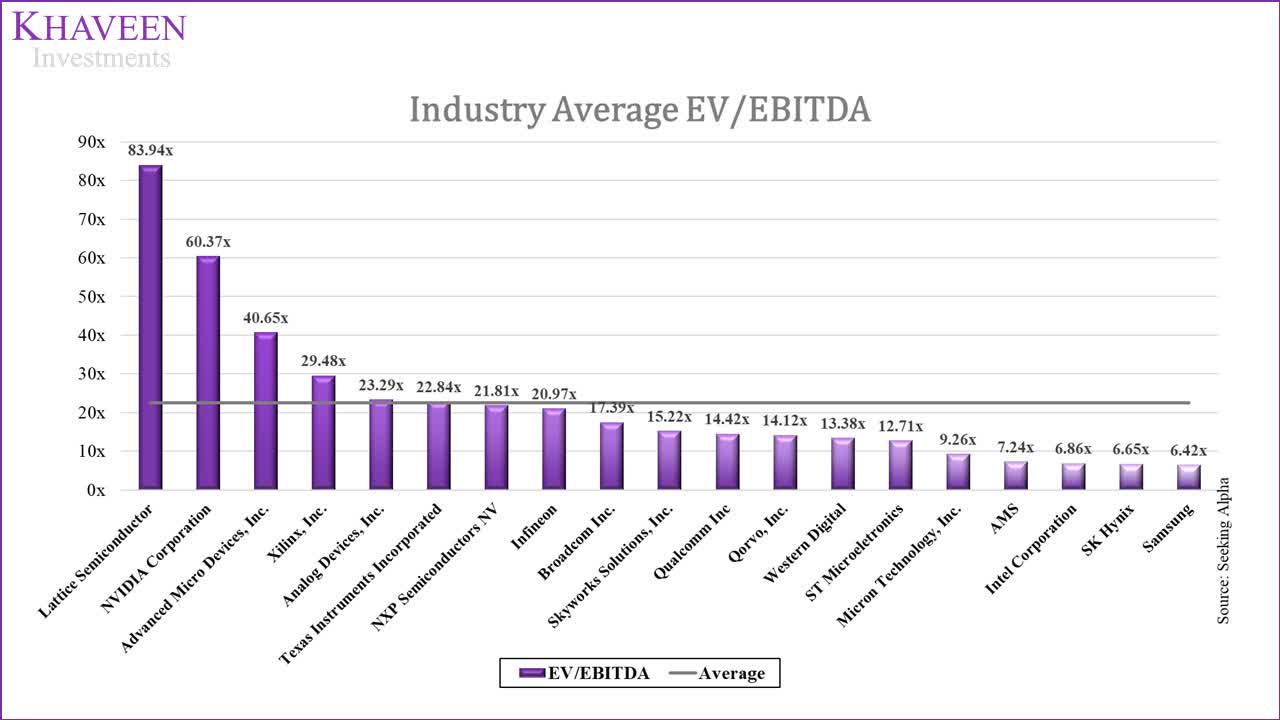

To worth the corporate, we used a DCF evaluation as we count on its money flows to stay optimistic going ahead. We based mostly our terminal worth on the chipmaker trade common of 24.15x.

SeekingAlpha, Khaveen Investments

We projected its revenues based mostly on its MP and IDP segments. For MP, we utilized our derived CAGR by way of 2026 as we count on its development to be supported by its relationships with main mid-tier smartphone makers. For IDP, we based mostly its development on the analog market CAGR of 4.8% by Market Analysis by way of 2027.

|

Income Forecast by Product Phase ($ mln) |

2019 |

2020 |

2021 |

2022F |

2023F |

2024F |

2025F |

2026F |

|

Cellular |

2,198 |

2,398 |

2,857 |

3,573 |

3,846 |

4,119 |

4,392 |

4,661 |

|

Progress % |

0.8% |

9.1% |

19.1% |

25.1% |

7.6% |

7.1% |

6.6% |

6.1% |

|

Infrastructure & Defence Product |

893 |

841 |

1,158 |

1,067 |

1,119 |

1,172 |

1,229 |

1,288 |

|

Progress % |

13% |

-6% |

38% |

-8% |

4.80% |

4.80% |

4.80% |

4.80% |

|

Complete |

3,091 |

3,239 |

4,015 |

4,641 |

4,964 |

5,292 |

5,621 |

5,949 |

|

Progress % |

4.0% |

4.8% |

24.0% |

15.6% |

7.0% |

6.6% |

6.2% |

5.8% |

Supply: Qorvo, Market Analysis, Khaveen Investments

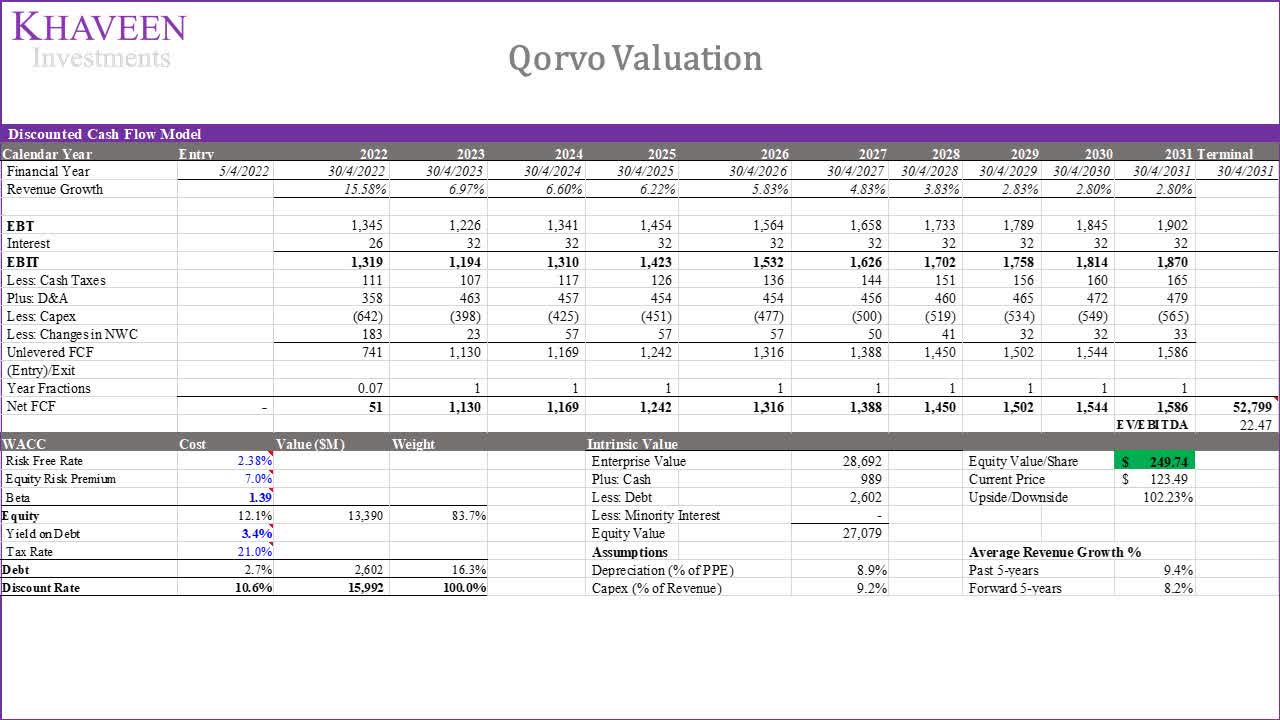

Primarily based on a reduction fee of 10.6% (firm’s WACC), our mannequin reveals its shares are undervalued by 102%.

Khaveen Investments

Verdict

All in all, we analyzed its income publicity by geographic areas the place its Asian based mostly prospects contribute the bulk (55%) of its revenues. We consider its buyer relationships with main Asian smartphone makers accounting for 77% of the mid-market 5G smartphone profit the corporate’s development outlook as adoption of 5G is anticipated to extend to 69% of the market by 2025 at a CAGR of 33%. Moreover, we consider it’s well-positioned to learn from this development with its RF portfolio together with its Fusion20 built-in RF resolution which highlights its dedication towards 5G adoption for the mass market. We projected its Cellular Merchandise to develop by 7.6% in FY2023 based mostly on our forecast of the rise within the share of 5G. Lastly, we consider its greater development RF enterprise can also be extremely engaging to its financials with greater revenue margins than its IDP phase and count on its whole gross margins to extend to 49.5% by 2026. General, we fee the corporate as a Sturdy Purchase with a goal value of $249.74.