Justin Sullivan

Introduction

As a dividend development investor, I always search alternatives to purchase income-producing belongings at engaging costs. With the S&P 500 nearly 20% down 12 months to this point, there could also be some alternatives to search out engaging investments. I generally add to my current positions to capitalize on engaging valuations, and generally I add to new ones to diversify my holdings.

I analyzed the shares of Walgreens (NASDAQ:WBA) up to now. Regardless of fascinating risk-reward performs, I discovered it a HOLD and most well-liked CVS (CVS) for my portfolio. Since I final analyzed Walgreens, the corporate’s share value has declined considerably. It’s time for me to revisit the corporate and see if the present decline within the share value made it a horny funding.

I’ll analyze the corporate utilizing my methodology for analyzing dividend development shares. I’m utilizing the identical technique to make it simpler to match researched corporations. I’ll look at the corporate’s fundamentals, valuation, development alternatives, and dangers. I’ll then attempt to decide if it is a good funding.

Searching for Alpha’s firm overview exhibits that:

Walgreens Boots Alliance operates as a pharmacy-led well being and retail magnificence firm. It operates via two segments, the USA and Worldwide. Walgreens sells pharmaceuticals and an assortment of retail merchandise, together with well being, wellness, magnificence, private care, consumable, and common merchandise. Walgreens Boots Alliance was based in 1901 and is predicated in Deerfield, Illinois.

Fundamentals

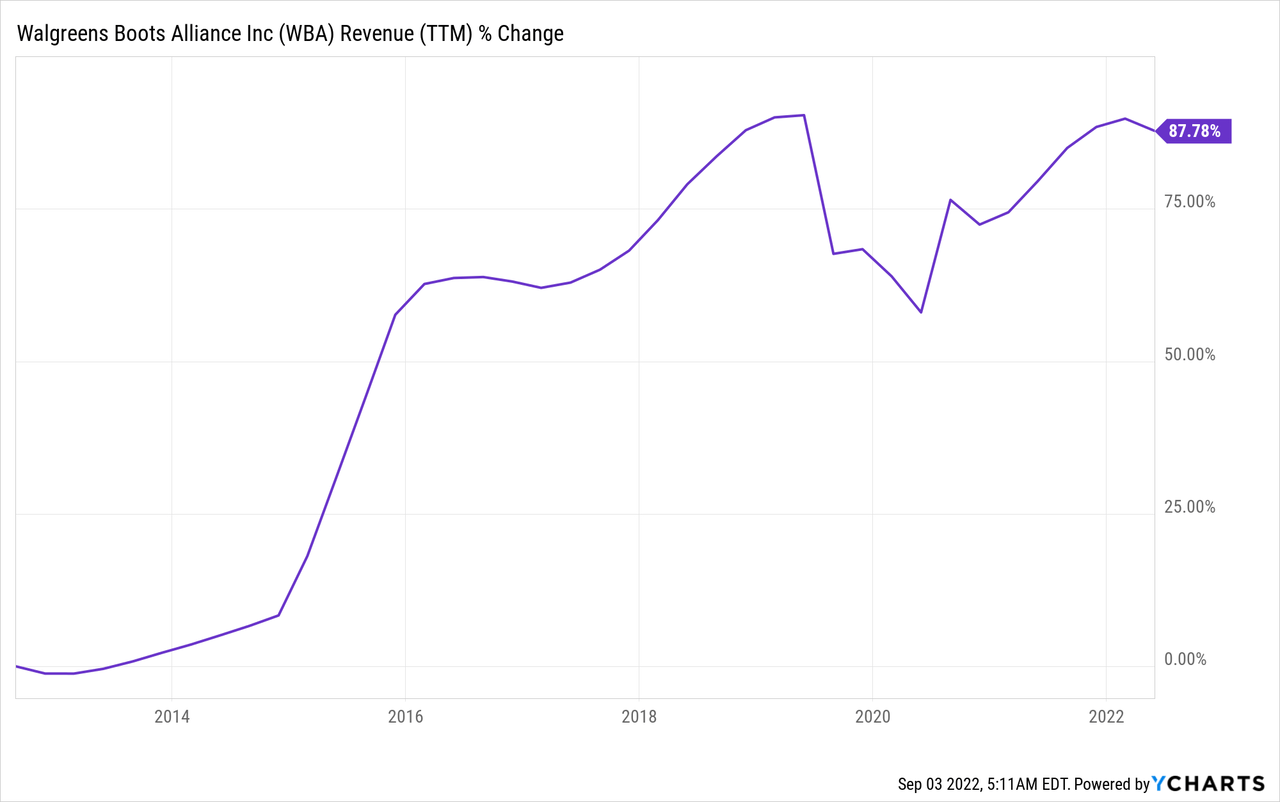

The revenues of Walgreens elevated considerably over the past decade. Revenues are up nearly 90% over the earlier ten years. The expansion in gross sales occurred organically as the corporate grew gross sales in shops and on-line and thru M&A exercise. Probably the most notable acquisition was the Ceremony Assist acquisition in 2015 for nearly $20B. Sooner or later, analysts’ consensus, as seen on Searching for Alpha, expects Walgreens to continue to grow gross sales at an annual fee of ~2% within the medium time period.

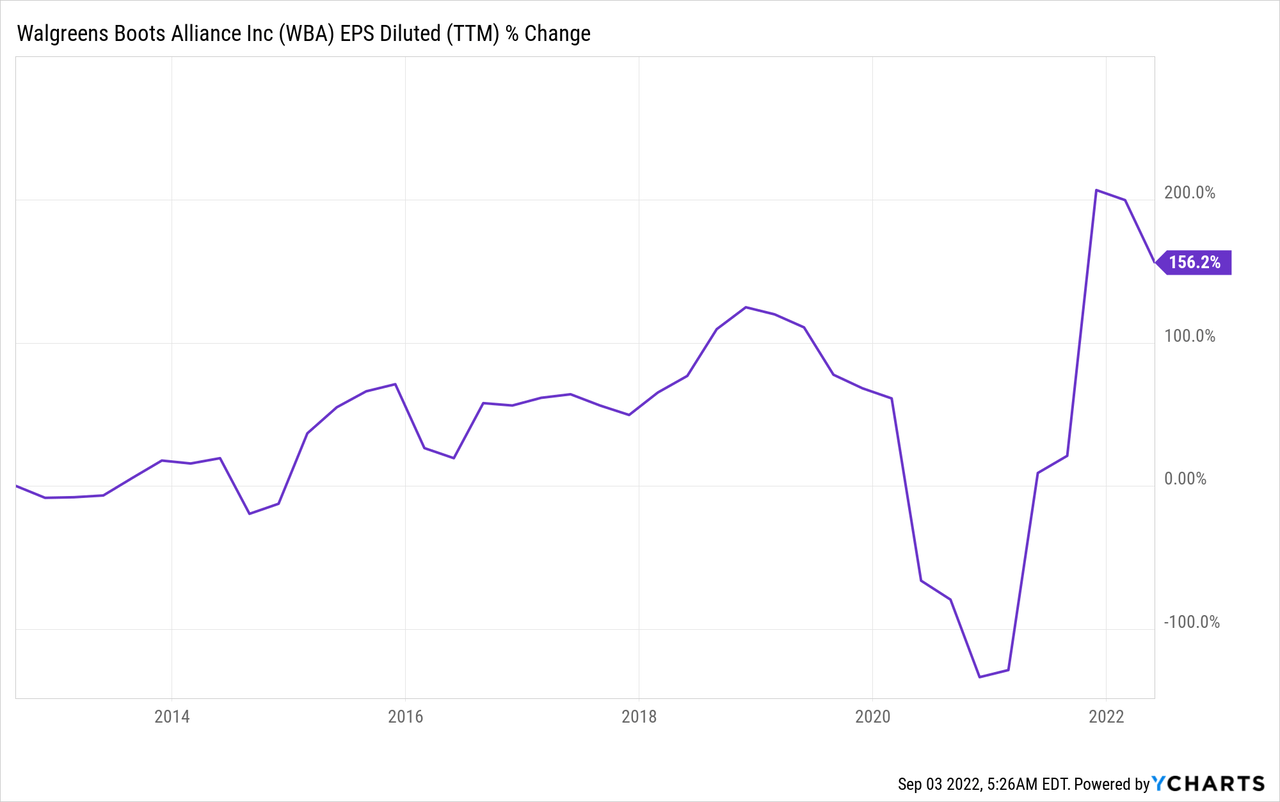

The EPS (earnings per share) grew quicker over the past decade. With EPS up greater than 150%, the state of affairs could look promising for Walgreens. Nevertheless, utilizing non-GAAP earnings, the corporate has struggled to develop since 2018. Regardless of some buyback actions, the working margin decreased from 5% a decade in the past to three% in 2021, hindering development. Sooner or later, analysts’ consensus, as seen on Searching for Alpha, expects Walgreens to continue to grow EPS at an annual fee of ~3% within the medium time period.

Walgreens has been paying a rising dividend for 46 years. The corporate is on its observe to reaching a dividend king standing. The dividend of Walgreens is engaging with a 5.4% yield, and it is usually comparatively secure with a 31% GAAP payout ratio and a 35% non-GAAP payout ratio. The corporate raised the dividend by 0.5% in July. Traders ought to anticipate decrease dividend will increase within the medium time period as the corporate is engaged on its turnaround plan to return to development.

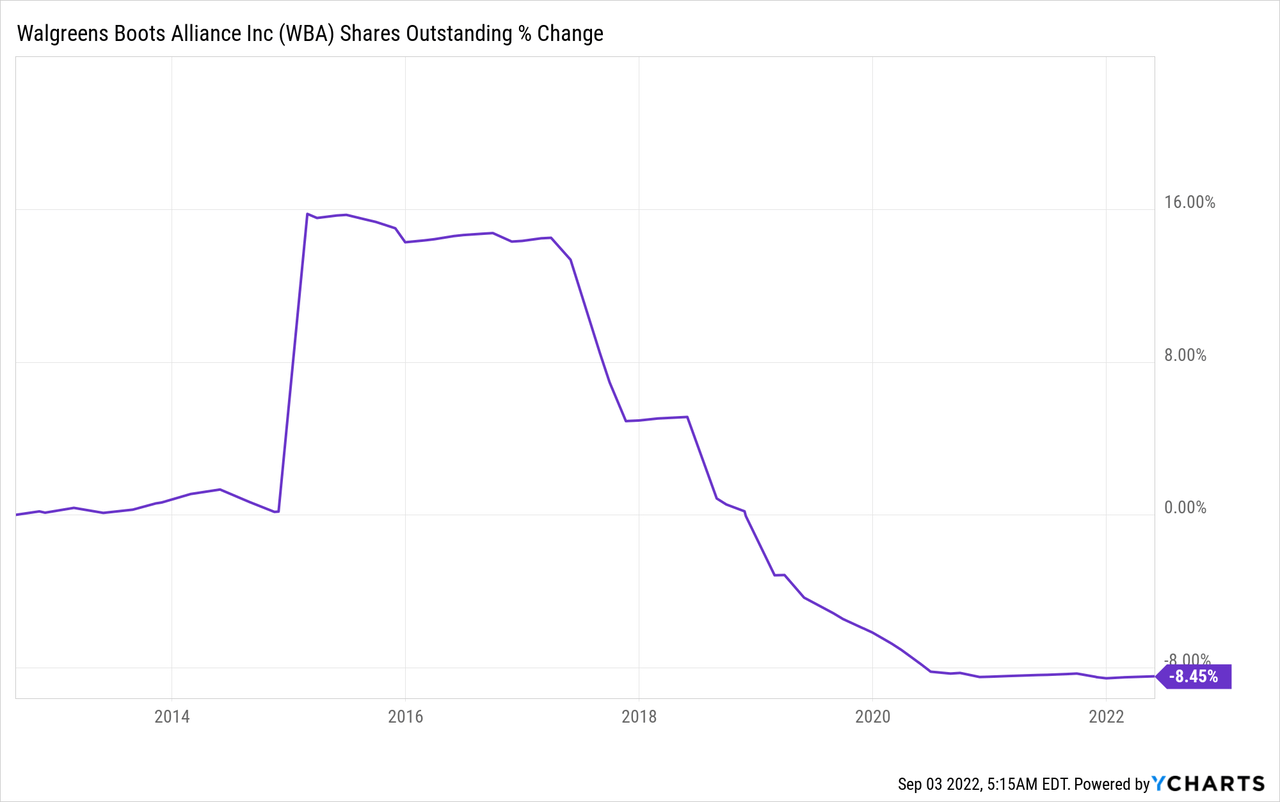

Along with the dividends, Walgreens returns capital to shareholders through buybacks. Buybacks are an environment friendly option to complement EPS development by reducing the variety of shares. They’re environment friendly when an organization is rising because it helps development. Walgreens purchased again nearly 8.5% of its shares within the final decade regardless of the large share issuance wanted to purchase Ceremony Assist. As the corporate invests in development, much less capital is allotted for buybacks.

Valuation

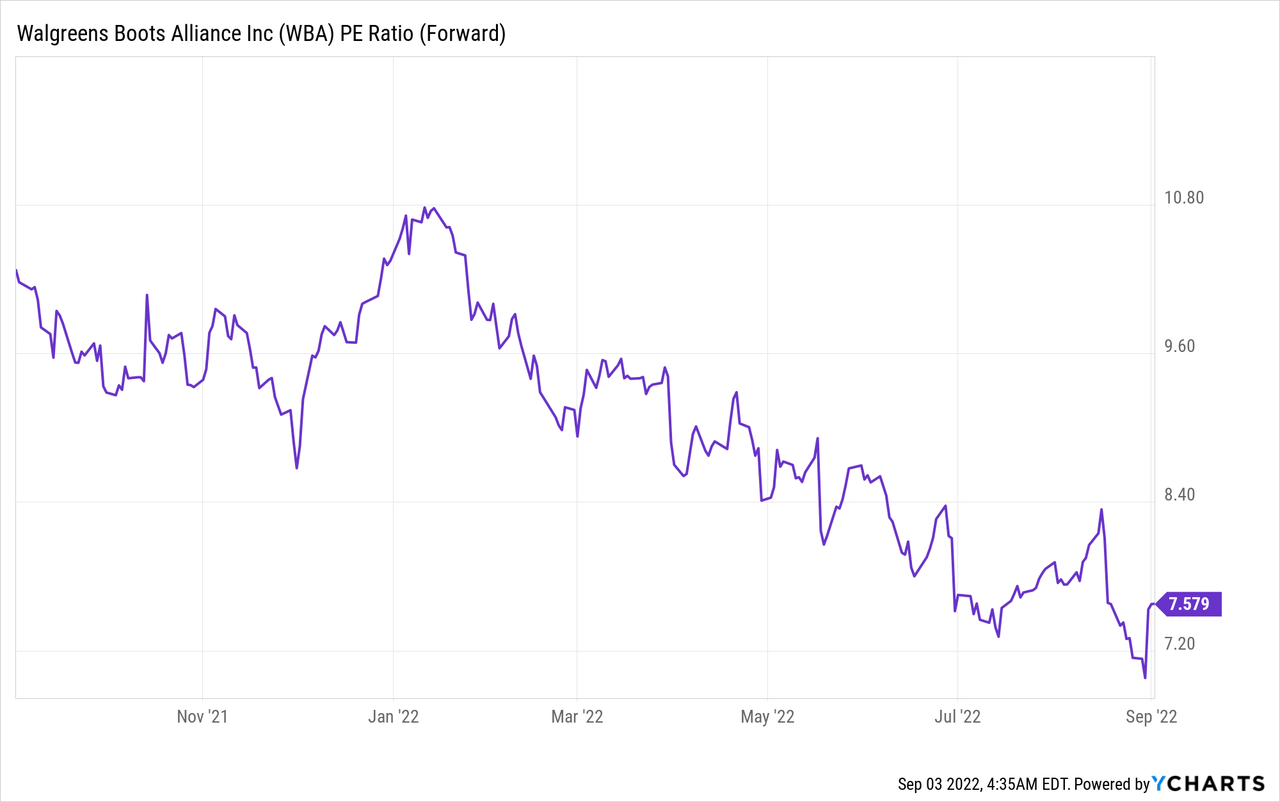

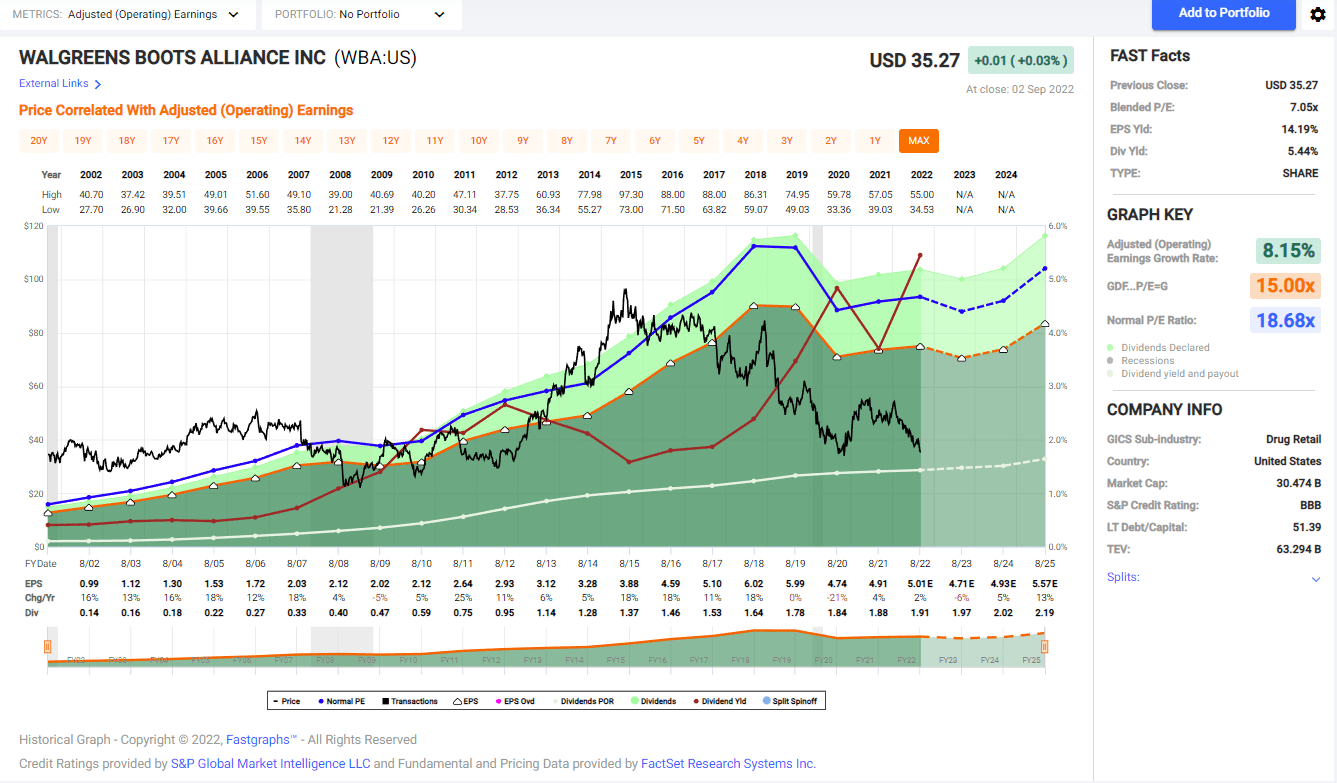

The corporate’s P/E (value to earnings) ratio has decreased over the past twelve months. Utilizing the forecasted EPS for 2022, the corporate’s future P/E ratio is roughly 7.5. It’s a horny valuation for a corporation that maintains its fundamentals. If the corporate can cease the EPS bleeding, that is a horny valuation because it plans to reignite development.

The graph under from Fastgraphs emphasizes what a chance Walgreens could supply. The corporate’s present P/E ratio is lower than half the typical P/E ratio of 18.7 that we’ve seen over the past twenty years. The expansion fee can be considerably decrease than the typical development fee of 8.15%. If Walgreens succeeds in stabilizing and rising its enterprise, buyers can have a big upside.

Fastgraphs

To conclude, Walgreens is struggling in the meanwhile. The corporate seeks its path for development whereas stabilizing its core enterprise. The anticipated development remains to be sluggish, however the dividend is engaging. On the similar time, the corporate enjoys a big low cost on its common valuation. Due to this fact, the corporate presents struggling fundamentals. It’s a horny funding if the corporate has a constructive development path.

Alternatives

Stabilization of the core enterprise appears to be succeeding. The corporate loved elevated revenues on account of Covid vaccines, and because the pandemic fades, it must continue to grow utilizing its legacy pharmacy enterprise. A secure core enterprise is essential for Walgreens to chase development alternatives past the core. Within the final quarter, retail gross sales are up 2.4%, excluding tobacco. Furthermore, following the pandemic, shops return to common opening hours regardless of labor scarcity.

As well as, the corporate additionally sees enchancment in its on-line enterprise. Walgreens attracted nearly 100M customers to its myWalgreens app, growing engagement with its purchasers. U.S digital gross sales are up 25% in Q3, following a 95% enhance final 12 months, with 2.8 million same-day pick-up orders. Shoppers get pleasure from each the supply choices and the choice to select up from Walgreens shops that at the moment are open for longer occasions.

Along with its core enterprise, and its enlargement with a digital and omnichannel providing, Walgreens is making an attempt to develop with its Walgreens Well being providing. The providing consists of important development of its pharmacy enterprise and mixing it with affected person care. The corporate invested in VillageMD and Shields to supply doctor care along with pharmacy merchandise and to supply specialised pharmacy providers to hospitals. Walgreens is making an attempt to change into a extra customer-centric enterprise and supply its purchasers a extra complete worth proposition.

Dangers

Probably the most important threat for Walgreens is execution failure. Turning round its core enterprise that seeks development and constructing a brand new enterprise is difficult. We noticed many giant caps like Walgreens searching for a turnaround. Some succeed, like McDonald’s (MCD) and Procter & Gamble (PG). Others have extended, just like the turnaround of IBM (IBM), and a few even fail, like Yahoo. Due to this fact, an important facet to comply with is whether or not the corporate manages to achieve traction.

The second threat is competitors. Even when we assume that the turnaround can be profitable, we see the next aggressive depth. With its completely different technique for coming into the insurance coverage enterprise, CVS is the closest competitor. But we additionally see on-line retailers, most notably Amazon (AMZN), coming into the sector. Walgreens has the benefit of its shops and the ecosystem it builds, however it’s nonetheless prone to stress the margins.

The third threat is inflation and fee hikes. Greater inflation means the corporate must enhance costs in a extremely aggressive setting. It occurs when the working margins are already low at 3%, and the corporate is making an attempt to stabilize the enterprise. Furthermore, with a debt to EBITDA ratio increased than 4, the corporate can even be affected by the rise in rate of interest, limiting its capability to accumulate extra corporations.

Conclusions

Walgreens is a wonderful American model identify with a big problem forward. The corporate is coping with difficult fundamentals because it struggles to develop. The corporate has a number of development alternatives to assist future gross sales and EPS development. Nonetheless, it has to execute its plan nicely in a difficult enterprise setting with increased inflation and rates of interest.

There’s additionally the aggressive threat and the execution and macro dangers. The present valuation appears very engaging within the optimistic situation, but if the pessimistic situation materializes, there may be extra room for a draw back. Due to this fact, Walgreens is a dangerous play for affected person buyers keen to have little publicity to the corporate to achieve important upside within the subsequent 3-5 years whereas having fun with the dividend. It’s nonetheless a HOLD for many buyers, because the dangers are substantial.