Justin Sullivan/Getty Pictures Information

Walgreens Boots Alliance (NASDAQ:WBA) is a traditionally sturdy performer that has underperformed not too long ago. WBA is at present reliant on the pharmacy section as their main income stream which is aligned for disruption by the present aggressive panorama. WBA administration seems to be main effectively and is correctly aligned to enhance WBA. The long run strategic objectives of WBA might present a brand new progress section that would enhance worth considerably over the long-term. WBA is at present valued at $36.93 in response to my assumptions utilizing a multi-stage weighted dividend low cost mannequin (DDM). An entrance place could also be obtainable given the present momentum of WBA via the promoting of put choices.

Evaluation Course of

When trying to research WBA, I centered my analysis on understanding the next inquiries to develop my assumptions for valuation:

- What’s the present aggressive panorama?

- How has WBA traditionally carried out and the impact at this time?

- What are the long run actions for WBA and is the administration aligned correctly?

I make the most of the outcomes of these inquiries to synthesize three potential eventualities for valuation. Then I corroborate that with the SA Quant Rankings and summarize on potential dangers. I then talk about a method for establishing an preliminary place for the valuation worth using the promoting of put choices.

Aggressive Panorama

Walgreens Boots Alliance competes within the Pharmacies and Drug Shops Business (NAICS 44611). Their main income segments are in the USA and have been divided into pharmacy (75.8%) and retail gross sales (24.2%) for FY 2021. This aggressive atmosphere has a number of layers of strategic teams in it, lots of which increase their main companies with pharmacies. WBA competes towards different massive companies resembling CVS pharmacy (CVS), Walmart (WMT), Kroger (KR), and Cigna (CI). Lots of the rivals management massive market shares of the prescription drug market (Figures 1 & 2). This excludes the net pharmacy market that has been rising with rivals like Amazon and different startups aggressively coming into the market house.

WBA was the second main pharmacy based mostly on prescription income in 2021 with $90.3 billion {dollars} whereas CVS was the dominant participant with $122.6 billion in income (Determine 1). WBA has the second largest U.S. footprint of drug retailer areas (8,760) in 2020 (Determine 2).

Determine 1. Main pharmacies in the USA in 2021, based mostly on prescription income (Statista) Determine 2. Variety of shops inn U.S 2020 (Statista)

The U.S. pharmacy market was sized at roughly $560 billion in 2021 and is predicted to develop at a CAGR of 6.3% into 2028 with a possible measurement of $861.67 billion. A number of the key drivers for the elevated projected demand are illness prevalence, growing old inhabitants, and growing healthcare expenditures. The US has had an total enhance in healthcare affected person quantity which naturally correlates with a better prescription quantity. These progress prospects shifting ahead result in a extra aggressive panorama. WBA’s 2021 Annual Report provides insightful data into the chance and competitiveness of their business.

Danger of recent entrants

The danger of recent entrants is excessive within the present retail-pharmacy industries. This is because of different effectively financed companies that may leverage their pre-existing enterprise fashions to synergistically enter the market. New entrants might have this functionality as a consequence of their present logistical capabilities and in depth capital. There are minimal switching prices for customers who can change supplier with fluidity. There’s authorities regulation which may disincentivize new entrants for the reason that legal guidelines on pricing may restrict potential margins. New entrants may create worth wars that harm the already tight margins with out a appreciable reapproach to price chopping methods and know-how. A second layer of on-line pharmacy competitors may lower the retail-pharmacy market measurement. WBA is at a excessive threat for brand new entrants putting aggressive pressures on their market share. Happily, WBA has a scale economic system, has progressive methods, and has massive market share to assist fight these threats.

Energy of suppliers

The facility of suppliers within the pharmacy business is insubstantial. Giant companies can backwards combine into generic manufacturing and solely the patent protected merchandise have any negotiating leverage. There are additionally nationwide and worldwide suppliers which locations strain on the suppliers to be extra amiable. WBA is at a low threat from provider energy.

Energy of patrons

WBA sells to quite a few wholesalers and retail prospects. No single buyer accounted for greater than 10% of WBA gross sales. Most gross sales are coated by third-party payers like insurance coverage corporations and authorities businesses. This can be a double-edged sword within the sense that it doubtlessly offers the first third-party payers leverage however the retail prospects are usually detached since they’re often not overlaying the prices. WBA is at a low threat from purchaser energy.

Present rivals’ depth

The retail pharmacy business is extremely aggressive as represented above (Figures 1, 2). The business progress is anticipated at a progress of 6.3% and the net pharmacy market is predicted to increase quickly which relieves some strain on the present aggressive atmosphere to share a bigger pie. The strongest rivals have alternative ways of offsetting their fastened prices which additionally helps ease the aggressive strain. There are a lot of massive corporations with a big proportion of market share which intensifies the aggressive impact since they’re so reliant on these income streams. The web pharmacy continues to be a comparatively new idea however will proceed to realize momentum and enhance aggressive depth into the long run. WBA is at a excessive threat from aggressive depth.

Danger of substitutes

Pharmaceutical merchandise are usually at a low threat for substitutes. The danger of substitute merchandise is predominantly between “model” identify and “generic” in terms of pharmaceutical merchandise. For intermediate companies like WBA, the generic model of a drug has greater margins whereas bringing in decrease income {dollars}.

Historic Efficiency

Walgreens has a powerful historical past of efficiency. They outperformed the S&P 500 from roughly 1995 to 2020 (Determine 3). Nevertheless, for the reason that S&P 500 throttled positively the previous two years coinciding with WBA’s critical underperformance, they’ve now roughly equalized their return over the proven interval.

Determine 3. Complete Returns vs. S&P 500 (TIKR Terminal)

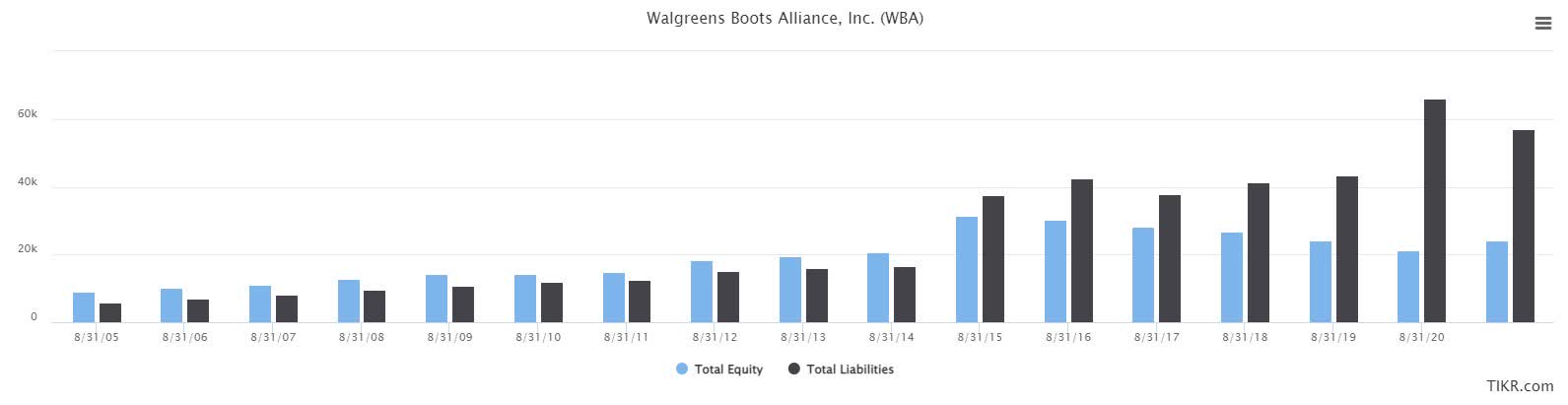

WBA had a big enhance in complete liabilities in 2015 and the D/E ratio has proven a rise since (Determine 4). This may occasionally signify how administration used capital construction and leverage to raise the inventory worth over the identical interval. This may occasionally have helped WBA outperform over a short while interval, however it has positioned long run debt issues which are effecting current day, the businesses selections, and efficiency at present. WBA at present has a Moody’s long run debt score of Baa2 and a adverse outlook together with a Normal & Poor’s score of BBB and a secure outlook. As of March 30, 2022, these rankings place WBA within the area of medium threat and funding grade.

Determine 4. Fairness & liabilities (TIKR Terminal)

With the modifications to capital construction augmented with the rise in annual revenues and constant web revenue margins, the ROE stayed effectively above 10% till 2019 (Determine 5). The ROA has been constantly declining over the identical interval.

Determine 5. ROE, ROA, NI margin (TIKR Terminal)

WBA traditionally splits its U.S. income streams between two main product lessons (pharmacy and retail). WBA dependence on their pharmacy section has been rising from 2013 to 2021 from 63% to 76% of complete income within the U.S. (Determine 6). This development exhibits a deepening entrenchment into a really aggressive business.

Determine 6. Phase income (Statista)

WBA has been offering a dividend to its shareholders for 45 years. The dividend progress has maintained an distinctive CAGR of seven.81% and 4.95% for the previous 10 and 5 years respectively (Determine 7). WBA at present has a yield (TTM) of 4.43% which is greater than it is 4-year common yield of three.56%. The dividend progress charge has significantly lowered for the reason that 2005-2012 interval.

Determine 7. Dividend historical past and progress (TIKR Terminal)

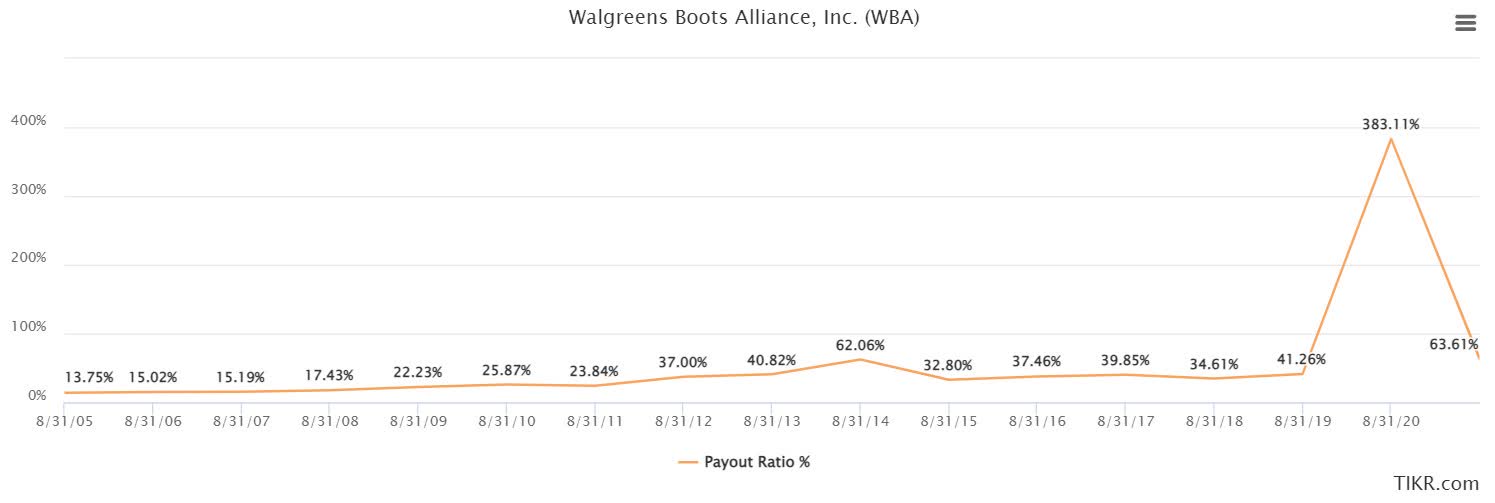

The payout ratio sometimes developments round 30-40% implying the dividend is often effectively coated and has ample room for progress (Determine 8). The dividend side is appetizing for a lot of buyers and WBA has traditionally been a powerful contender augmenting dividend centered portfolios.

Determine 8. Payout ratio (TIKR Terminal)

WBA has traditionally been a powerful performer augmented by their dividend and progress. The previous 3 years present a steep decline within the effectiveness of the agency. They’ve doubtlessly over-leveraged themselves, entrenched deeper right into a aggressive market that’s prime for disruption, and their profitability metrics are lower than ultimate. My perspective exhibits a agency that has deteriorated from their prime and desires new life to reinvigorate themselves or they could proceed to deteriorate or stagnate for a protracted time frame.

Future Path

WBA is making large strategic shifts shifting into the long run and growing a healthcare section. Of their quarterly report ending 28 February 2022, they expressed massive motion into their formidable future path. WBA is turning into a extra complete care heart for customers and have been positioning themselves accordingly. The plan is to grow to be a “main supplier of native medical care providers by leveraging its consumer-centric know-how and pharmacy community to ship value-based care.” WBA is specializing in enhancing care, shopper well being, and reducing their prices.

WBA created a brand new section in fiscal 12 months 2022 often known as Walgreens Well being. Walgreens Well being “is a technology-enabled care mannequin powered by a nationally scaled, regionally delivered healthcare platform.” Walgreens Heath will combine the WBA international scale with a number of well being care capabilities and speed up WBA into greater than only a pharmacy with a retail part. The aim of Walgreens Well being is to enhance well being associated outcomes and make healthcare extra reasonably priced and accessible at a extra localized group degree.

The Walgreens Well being initiative has nice potential. WBA as of August 2021 has entry to roughly 78% of the uspopulation inside a 5-mile radius of any given WBA location and is positioned effectively to combine healthcare into native communities. WBA has purchased majority investments in Village Apply Administration Firm (VillageMD), Shields Well being Options (Shields), and CareCentrix together with different investments to assist actualize their future path.

VillageMD is “a number one, nationwide supplier of value-based main care providers.” Shields gives progressive well being care fashions and know-how to raise well being system efficiency. CareCentrix is a number one unbiased home-centered platform that focuses on shopper outcomes. WBA plans to have 600 in-store VillageMD clinics by 2025 and 1,000 by 2027 with a concentrate on underserved communities. WBA anticipates this transition to stagnate progress till 2024 as a result of massive investments and debt that’s required to reposition themselves. The administration group forecasts the income progress to be within the 11-13% vary after the transition which may very well be reinvigorating.

The success of this transition will dictate the longevity of WBA as a powerhouse firm. The aggressive panorama is to aggressive for WBA to not be proactive. They’ll both efficiently adapt and speed up into their new technique, or they may fail to execute whereas their market shares get chiseled away. I do consider that WBA has the potential to execute on their future plans.

Management

WBA has a really broad and numerous management group that brings expertise from a number of industries and walks of life. A number of sitting Administrators have elaborate expertise within the healthcare business as administrators, executives, educators, and practitioners. The senior administration has distinctive operational expertise and supply a powerful breadth of data for WBA shifting ahead. Whereas the Board and Government group are all vital members for the way forward for WBA. The CEO Rosalind Brewer joined WBA in March of 2021 and has constructed her functionality from a number of roles at dominant corporations all through her profession together with Kimberly Clark (KMB), Walmart, and Starbucks (SBUX). Ms. Brewer ranks as one of many prime most influential and highly effective girls in enterprise, and having her main the ship may be very affirming.

Insider Buying and selling

The insiders at WBA don’t appear to promote their holdings usually which is insightful into the behaviors and notion of firm management. WBA offered $900,000,000 value of Amerisourcebergen (ABC) shares on Could 11, 2022 (Determine 9). The public launch from WBA states that the proceeds shall be used “primarily for debt paydown and the continued help of its strategic priorities.” A director additionally offered 2,725 shares in November of 2021 at a worth of $47.16 per share. I theorize that the administration group thinks the inventory worth is at present undervalued and that they’re contemplating the way forward for WBA protected sufficient to carry a portion of their wealth.

Determine 9. Insider buying and selling (SecForm4)

Valuation

Assumptions

WBA has a powerful alternative to capitalize sooner or later. I do weigh the strategic shift favorably contemplating the current historic efficiency and strain from the present aggressive atmosphere.

I’ll make the most of a multi-stage DDM as a result of WBA has a historic efficiency of constant dividends. A DDM permits for less complicated estimations and a greater built-in margin of security since they’ve established consistency as their popularity.

The low cost charge shall be 9% for the mannequin which is the present price of fairness (8.4%) augmented with a margin of security. I may also assume the payout ratio stays fixed. WBA has a powerful historical past of dividends and can probably not minimize their dividend except there’s an emergent scenario requiring it. Their payout ratio is at present 33% and has room to securely enhance on the present working efficiency of the agency.

I’ll assume establishing a place earlier than the August dividend. August can also be sometimes the timeframe that WBA will increase their dividend.

We’ll assume that the dividend progress charge will match the income progress charge of the agency. This doesn’t think about a wide range of different estimate inputs like margin variance, share repurchases, and so on. The belief is the expansion of the corporate will stay fixed together with the payout ratio. Searching for Alpha consensus dividend estimates for 2023 present a progress charge of roughly 2.6%. This would be the preliminary progress charge inputted into the mannequin till 2024 when WBA will start to actualize their new technique and enhance their progress charge.

The three eventualities are as follows:

Situation 1: WBA has a 2.6% progress charge till 2024. They can not capitalize on their new aggressive edge and progress stays gradual. On this scenario, the expansion stabilizes on the long-term progress charge of a mature enterprise of three% over the quick time period and a pair of.5% in perpetuity. This state of affairs shall be weighted as a 30% chance (Determine 10).

Determine 10. Dividend low cost mannequin state of affairs 1 (Writer)

Situation 2: WBA has a 2.6% progress charge till 2024. Walgreens Well being good points momentum and turns into a worthwhile section for the agency. The expansion charge within the mid-term good points is optimistic however not on the expectation put forth by administration. Since there’s probably an expertise curve and a heavy aggressive atmosphere to include, 2025-2030 will present a 4% progress and enhance by 0.5% till 2030 the place the perpetuity worth shall be at 2.5%. This state of affairs shall be weighted as a 40% chance (Determine 11).

Determine 11. Dividend low cost mannequin state of affairs 2 (Writer)

Situation 3: WBA has a 2.6% progress charge till 2024. Walgreens Well being strikes strongly in step with the administration group’s expectation of progress of 11% in 2025 to 13% in 2030. The enterprise will develop in perpetuity at 2.5% afterward. This state of affairs shall be weighted as a 30% chance (Determine 12).

Determine 12. Dividend low cost mannequin state of affairs 3 (Writer)

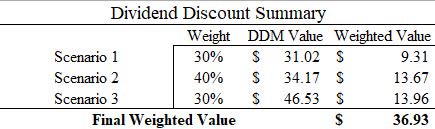

WBA is at present valued as a weighted common of the three eventualities offered. The acquisition worth aim is $36.93 which is about 10-15% decrease than the present buying and selling worth (Determine 13). This valuation together with the present worth signify a “maintain” score from my perspective. The assumptions have been made off of my private synthesizing of data, threat tolerance, and the valuation which is extremely topic to enter variables. This valuation might current as a chance within the close to future for the reason that inventory worth has had adverse momentum over the quick time period. I theorize this momentum might create an entrance worth for a long-term worth play.

Determine 13. Dividend low cost mannequin abstract (Writer)

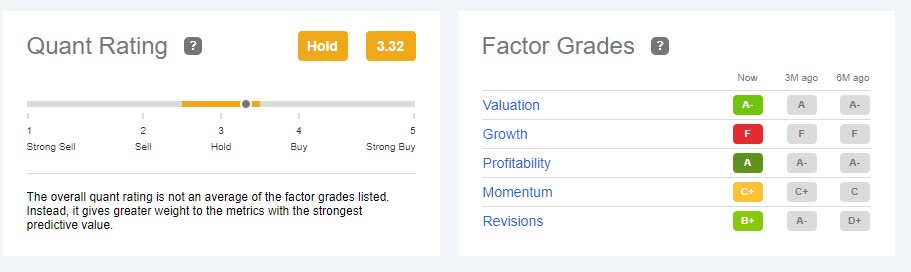

The present Quant Score from searching for alpha additionally has WBA at present rated as a “Maintain” with a score of three.3/5 (Determine 14). The analysts are estimating poor progress into mid 2023 that means WBA might proceed to development downwards in inventory worth. WBA has had a poor momentum development having dropped greater than the sector median and the S&P 500 total. The shifting averages are trending downward with the 10-day ($43.12) < 50-day ($43.93) < 100-day ($46.22) < 200-day ($47.67), as of this writing.

Determine 14. Quant Score (Searching for Alpha)

Dangers

There are a lot of potential dangers related to the WBA. Their main pharmacy income section is in a extremely aggressive business that’s vulnerable to modifications. WBA inventory worth not too long ago has had adverse momentum which may aggressively proceed downwards over the quick time period. The present macro-environment may create systematic threat via elements resembling inflation, rates of interest, and provide chain issues. WBA has a big debt place that does have some publicity to variable rates of interest. WBA may additionally fail sooner or later to execute on their Walgreens Well being section which has massive alternative prices and capital investments.

Potential Entrance Positions

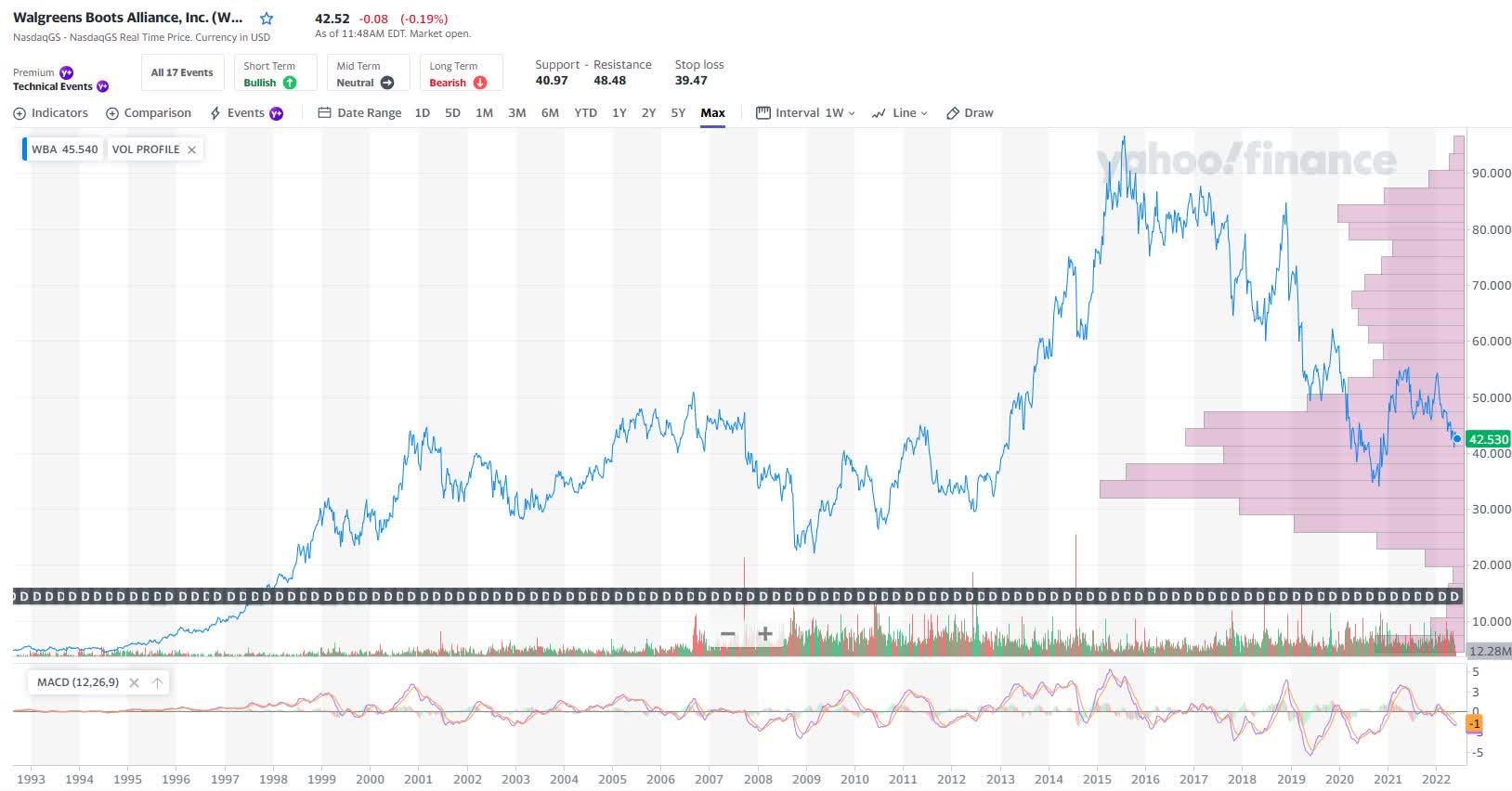

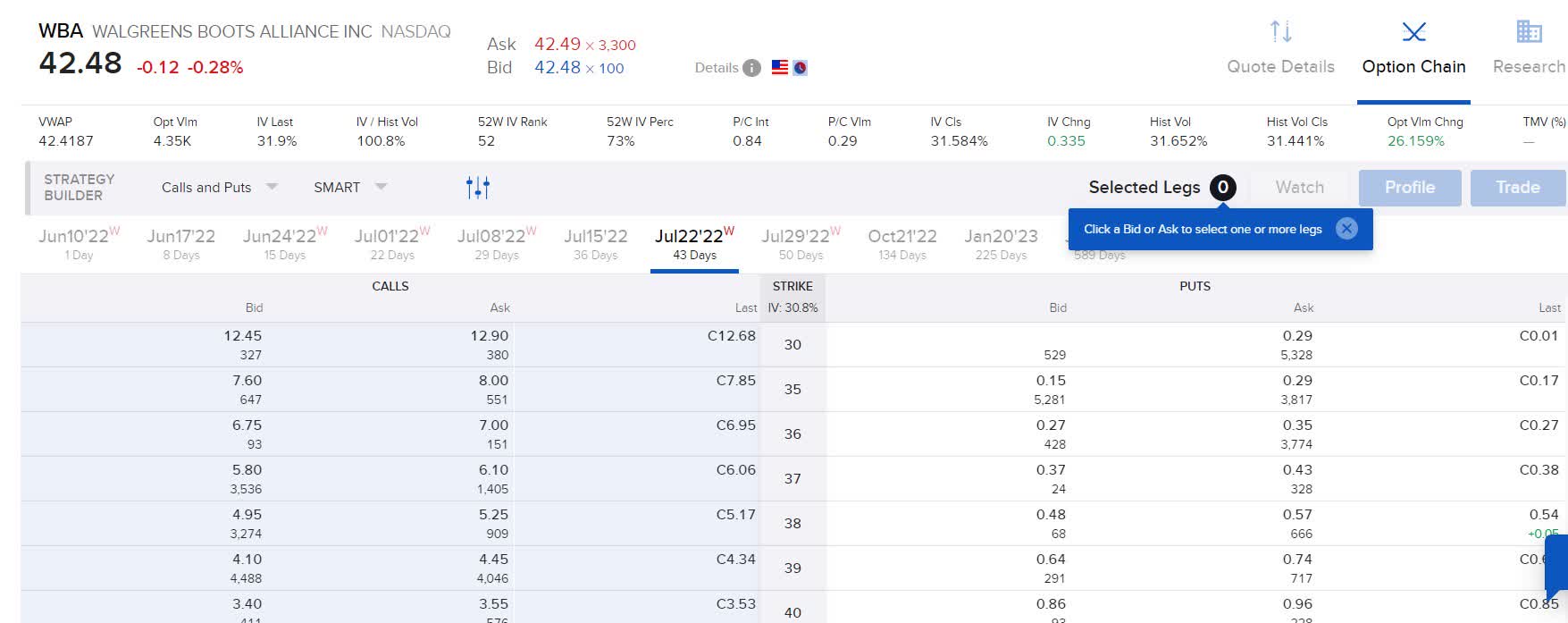

WBA is buying and selling inside a 10-15% vary of my desired entrance worth of roughly $37. There’s a massive quantity of purchases within the $34 to $38 vary, in response to the quantity profile on Yahoo Finance (Determine 15). WBA over the long run has not traded close to these lows since 2020 and previous to that 2014. I speculate WBA might proceed to strategy these ranges and should present an entrance alternative. We will make the most of the promoting of put choices to gather a premium whereas we look ahead to our aim worth to be achieved. As of the writing of this text, the $37 strike for 43 DTE on July 22, 2022, has a bid and ask worth of $0.37 and $0.43 (Determine 16). Because of this a mid worth of $0.40 would create an annualized return of (365/43) * [($0.40*100)/$3,700] * 100 = 9.18%. It will create an appropriate return to allocate collateral of $3700 promoting a put place with a premium (9.18% annualized) whereas patiently observing the value motion.

Determine 15. Lengthy-term worth motion (Yahoo Finance)

Determine 16. Promoting places 43 DTE (IBKR)

Conclusion

WBA has had a deterioration of efficiency over the previous few years, however I believe it has the mid- to long-term potential to reap the benefits of its strengths. WBA is coming into into a brand new business and doubtlessly creating a strong new income section for itself. I believe the present worth motion may transfer favorably towards my valuation worth, creating a chance for coming into a place over the long run. I at present charge shares as a “maintain” and would shift that to a “purchase” as they strategy the present valuation worth.