jetcityimage

Thesis

Buying and selling at a one-year ahead P/E of lower than x6 and a dividend yield of larger than 5%, Walgreen Boots Alliance (NASDAQ:WBA) inventory is simply too engaging to disregard. Buyers ought to think about that from a top-down perspective, there may be little that justifies doubting that WBA won’t proceed to ship engaging money flows in relation to the corporate’s valuation. Personally, I imagine WBA inventory needs to be valued at $47.45/share. I anchor my argument on a residual earnings mannequin primarily based on analyst consensus estimates.

For reference, WBA has underperformed YTD: this inventory is down 33% versus a lack of 18% for the S&P 500 (SPY).

Searching for Alpha

About Walgreen Boots Alliance

Walgreens Boots Alliance, Inc. is the holding firm that owns the pharmacy chains Walgreens and Boots, in addition to some smaller pharma producers and distributors. WBA is finest described as a pharmacy-led retail firm, which sells each prescribed drugs and a portfolio of retail merchandise, together with verticals referring to magnificence, well being and wellness. The corporate was shaped in 2014, following the merger of Walgreens and Alliance Boots. This made the conglomerate one of many largest pharma distributors globally. Right now, WBA operates nearly 9,000 retail shops within the US and barely greater than 4,000 retail shops in Germany, United Kingdom, Eire, Norway, the Netherlands, Thailand, Mexico, and Chile. Notably, as of early 2022, Walgreens Boots Alliance was ranked because the US’ 18th largest enterprise when it comes to income (Forbes 500), producing greater than $132 billion of gross sales in 2021.

WBA’s Financials

Since Walgreens and Alliance Boots merged in 2014, the corporate has managed to take care of a regular enterprise enlargement, rising revenues at a CAGR of about 5%. Accordingly, revenues elevated from about $103 billion in 2015 to $132.5 billion in 2021. To be honest, profitability has not expanded at an identical tempo. Over the identical time interval, gross revenue elevated from $26.9 billion to $28 billion. Working earnings even decreased: from $5.2 billion in 2015 to $3.7 billion in 2021.

The lack of profitability can arguably be defined by two components: (1) more durable aggressive surroundings — principally because of giant basic retail gamers coming into the market by means of e-commerce, together with Amazon (AMZN) and Walmart (WMT) — (2) and WBA’s personal investments in digital enlargement. However for my part, the market greater than discounted the profitability loss and more durable aggressive surroundings, as WBA inventory has depreciated by greater than 60% since 2015. Consequently, WBA is now valued at enterprise worth of $63 billion, composed of $30 billion market capitalization and $33 billion of internet debt. This, I argue, is engaging in relation to money from operations equal to $5.1 billion (TTM reference).

Low cost Valuation And Engaging Yield

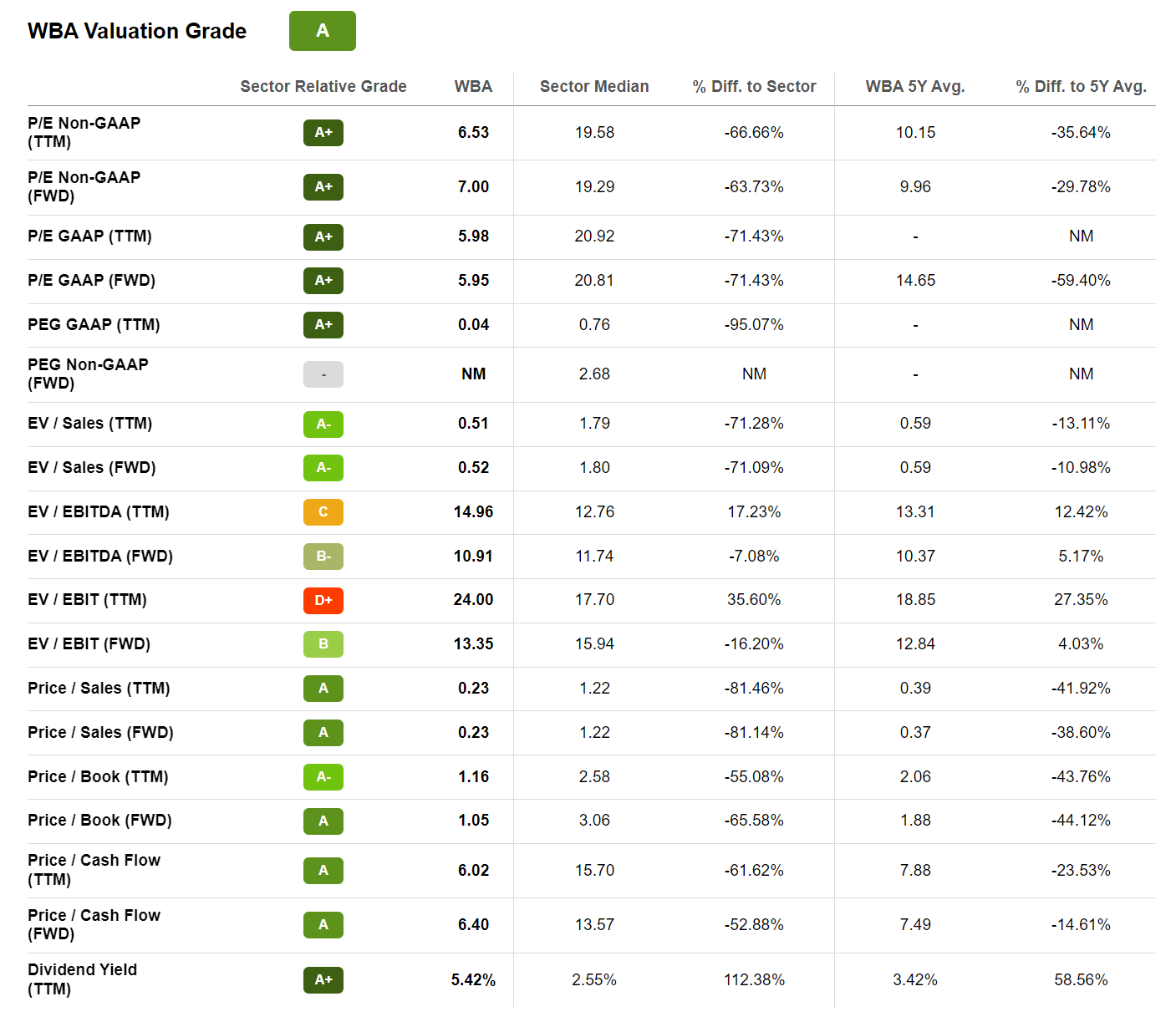

Walgreen Boots Alliance is valued very low cost. Buyers ought to think about that WBA inventory is buying and selling at a one-year ahead P/E of lower than x6, a P/S of x0.2 and a P/B of about x1. As in comparison with the sector median, these multiples indicate an undervaluation of 71%, 81% and 65% respectively. True, WBA operates with monetary leverage, so enterprise multiples is perhaps extra fitted to comparability. However nonetheless, EV/EBIT of x13 and EV/Gross sales of x0.5 point out that WBA inventory could possibly be 15% – 70% undervalued as in comparison with opponents.

Furthermore, I might additionally prefer to level out the larger than 5% dividend yield for WBA, versus 2.5% for the sector. Even when an investor considers WBA’s dividend security as non-sustainable — given stronger competitors and margin pressures because of inflation — the dividends provide margin of security earlier than the yield compresses to the trade median.

Searching for Alpha

Goal Value Estimation

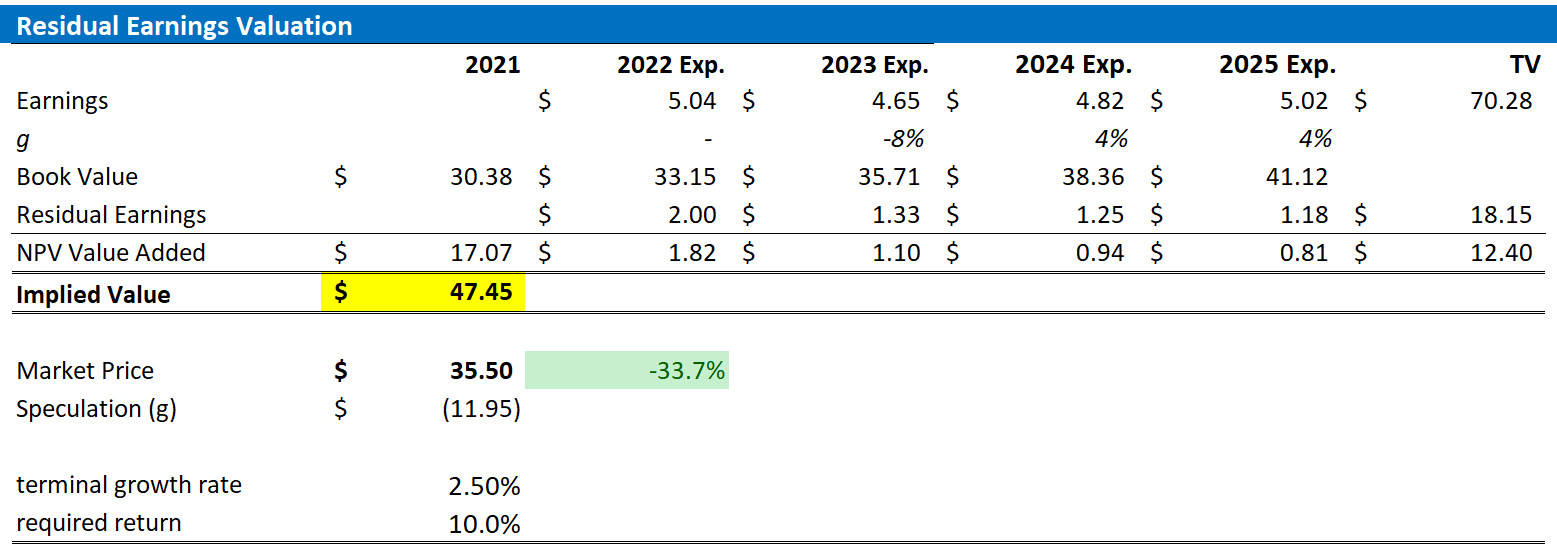

To estimate a inventory’s honest implied share value, I like to make use of the residual earnings mannequin, which anchors on the concept {that a} valuation ought to equal a enterprise discounted future earnings after capital cost.

With reference to my WBA valuation, I make the next assumptions:

- To forecast EPS, I anchor on the consensus analyst forecast as accessible on the Bloomberg Terminal ‘until 2025. In my view, any estimate past 2025 is just too speculative to incorporate in a valuation framework. However for 2-3 years, analyst consensus is normally fairly exact.

- To estimate the capital cost, I anchor on WBA’s price of fairness at 10%.

- To derive WBA’s tax price, I extrapolate the 3-year common efficient tax price from 2019, 2020 and 2021.

- For the terminal development price after 2025, I apply 2.5%, which is the same as the nominal international estimated GDP development.

Given these assumptions, I calculate a base-case goal value for WBA of $47.45/share (nearly 35% upside).

Analyst Consensus EPS; Creator’s Calculation

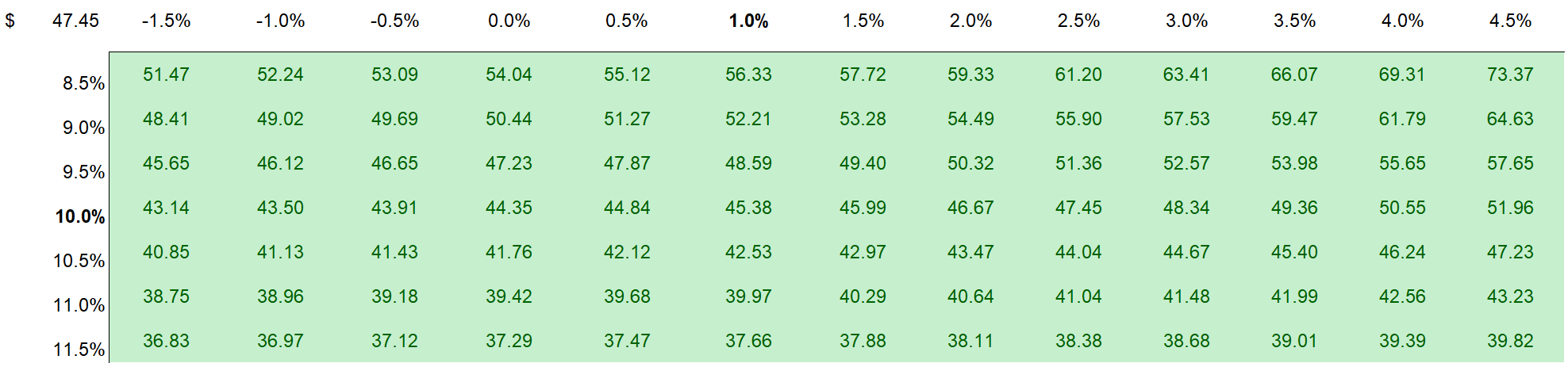

Notably, my bullish value goal will not be a mirrored image of a selected mixture of development and price of capital. The truth is, please discover under a sensitivity evaluation that helps completely different assumption.

Analyst Consensus EPS; Creator’s Calculation

Reflecting on WBA’s valuation low cost, I believe it’s honest to say that Mr. Market costs WBA like a worth entice, with little potential for development. Nevertheless, whereas it’d definitely be potential that WBA will develop at a CAGR in step with nominal GDP development (in actual fact, that is my base-case assumption), I imagine the enterprise has a lovely potential for margin enlargement. Buyers would possibly wish to think about that WBA’s EBITDA margin is at the moment lower than 3.5%, versus about 12% for the patron staples sector median. For reference, if administration may enhance profitability (EBITDA) to five% of gross sales, a further $1 to $1.5 billion of internet earnings may undoubtedly be potential. And as administration is closing underperforming shops, in addition to pushing for a better share of digital gross sales, a 150-basis level margin enlargement will not be farfetched, for my part.

Dangers

Walgreen Boots Alliance has internet monetary leverage of about 100% of the corporate’s fairness market valuation. Consequently, I imagine it’s honest to fret about financial tightening and rising rates of interest, which may result in greater price of debt and decrease profitability. As a consequence, WBA’s dividend yield would possibly endure a contraction.

On a short- to mid-term time horizon, traders may additionally wish to think about that the present macro-environment for shares will not be very favorable. Prospects for the worldwide economic system are skewed towards a recession, for my part — which is mirrored in value uncertainty for shares. And WBA’s fairness should not be exempt from volatility.

Conclusion

The chance/reward alternative for Walgreen Boots Alliance inventory is engaging, for my part. Buyers would possibly wish to think about that WBA’s P/E, P/S and P/B multiples indicate an undervaluation as in comparison with the sector median of 71%, 81% and 65% respectively. This low cost ought to greater than sufficiently steadiness any threat that the corporate would possibly face in relation to trade competitors and macroeconomic/financial coverage uncertainty. Primarily based on a residual earnings mannequin, I imagine WBA needs to be valued at $47.45/share. Purchase.