Justin Sullivan/Getty Photographs Information

Walgreens Boots Alliance (NASDAQ:WBA) has been a persistent underperformer for a few years. As soon as thought-about a development retail darling like Walmart (WMT) within the Eighties and Nineties, working outcomes have upset for fairly a while as a operate of fierce competitors and an excessive amount of debt on the stability sheet. Nonetheless, the valuation is now extremely low cost. The simply lined 4.5% dividend yield is difficult to disregard. And, the corporate has numerous shifting elements and belongings with misunderstood price by the common investor. For backside fishers like myself, shopping for a small place has loads of logic behind it, even when extra short-term draw back seems.

The perfect information and catalyst for a inventory backside is Walgreens is getting ready to promote its British Boots pharmacy belongings within the coming months, which may usher in as a lot as US$7 to $9 billion in money to repay debt or redeploy to development initiatives. A profitable Boots sale ought to enable administration to refocus the corporate on American shops and shoppers (82% of gross sales and 90% of earnings technology the final two quarters). A number of studies have two, if not three, potential patrons finalizing critical bids by the top of Might. The mainstream monetary press is anticipating Apollo International (APO), Asda/TDR Capital, and presumably India’s Reliance Industries would be the possible suitors.

On the finish of February 2022, the corporate held $16.8 billion in present belongings vs. $22.7 billion in present liabilities, $21.9 billion in future lease obligations, and $11.2 billion in long-term debt. In abstract, $5 billion in annualized money stream technology over the past 4 years at WBA stays a low/weak quantity vs. a internet long-term legal responsibility complete of $44 billion (complete liabilities minus present belongings). The almost 9x ratio of internet long-term liabilities vs. trailing 12-month money stream is excessively excessive measured in opposition to an S&P 500 blue-chip a number of common nearer to 5x.

Extra concepts to munch on, 73% of U.S. gross sales are categorized as pharmacy associated vs. 27% for common retail. AmerisourceBergen (ABC) is the principle wholesale supply of prescription drugs to Walgreens, promoting $30 billion in items to the corporate over the primary six months of fiscal 2022. When it comes to cross possession, WBA held 28.2% of Amerisource Bergen, roughly 58.8 million shares on the finish of February (price $8.9 billion on the present $151 ABC market quote).

Weak Efficiency Scaring Away Traders

Truthfully, the fast-money crowd has left Walgreens for useless the final couple of years, regardless of document profitability throughout the COVID-19 pandemic. WBA has reported an all-time excessive $6.2 billion in after-tax working earnings and asset features, about $7.27 per share over the trailing 4 quarters.

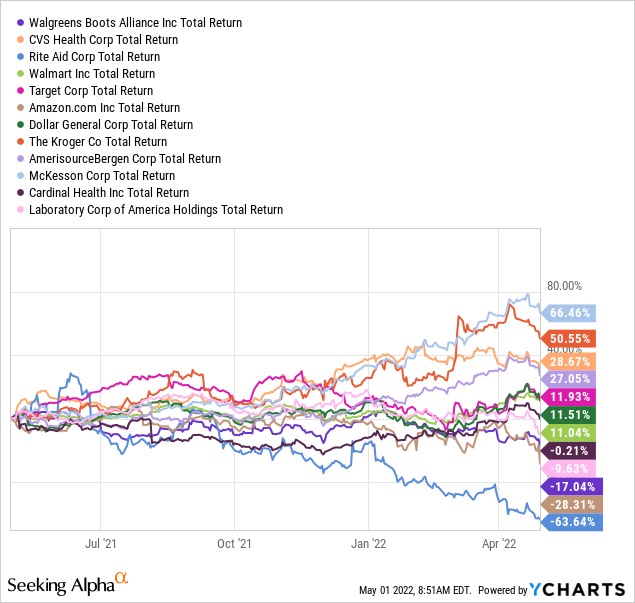

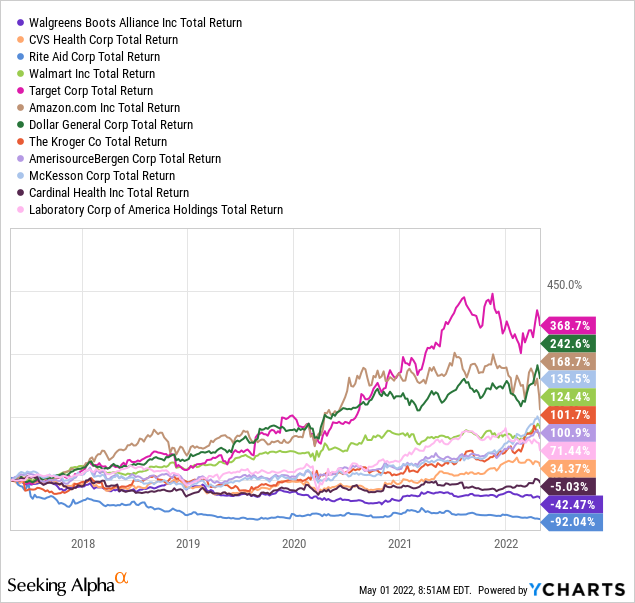

Within the well being care supply and main retailer sectors, Walgreens has been one of many weakest investments to carry since 2017. It’s not obscure why share homeowners have bought, or stay disgusted and upset at administration. Beneath are 1-year and 5-year graphs evaluating complete returns vs. friends and rivals within the bigger capitalization area. This checklist consists of CVS Well being (CVS), Ceremony Support (RAD), Walmart, Goal (TGT), Amazon (AMZN), Greenback Normal (DG), Kroger(KR), AmerisourceBergen, McKesson (MCK), Cardinal Well being (CAH), and Laboratory Corp. of America (LH).

YCharts YCharts

Nonetheless, on a bullish notice, technical momentum indicators are beginning to behave higher. Particularly, the drop in worth on Friday to new 52-week lows was not confirmed by creations just like the each day ADL, NVI or OBV indicators. I’ve circled in inexperienced, bottoms in every of those momentum alerts since early December.

1-12 months Chart, Each day Worth with Writer Reference Factors – StockCharts.com

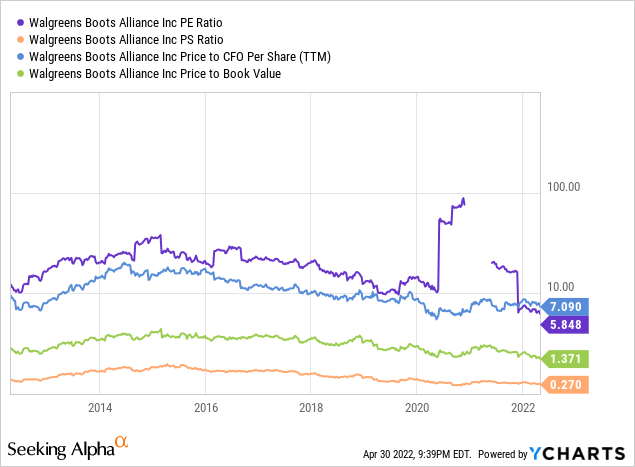

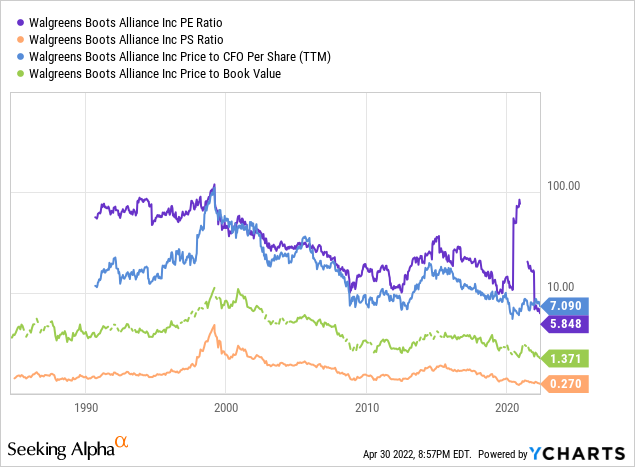

File Low Valuation

The principle argument to purchase Walgreens now could be it has reached a document low valuation in late April 2022. Years of detrimental inventory worth developments have mixed with flat to barely higher underlying fundamentals to create right this moment’s undervaluation. You may evaluation on 10-year and 35-year graphs drawn beneath how the WBA valuation image on trailing working metrics could be very engaging proper now. Taking a look at worth to earnings, gross sales, money stream, and ebook worth, this might be a once-in-a-generation purchase alternative for a number one nationwide U.S. brand-name pharmacy chain.

YCharts YCharts

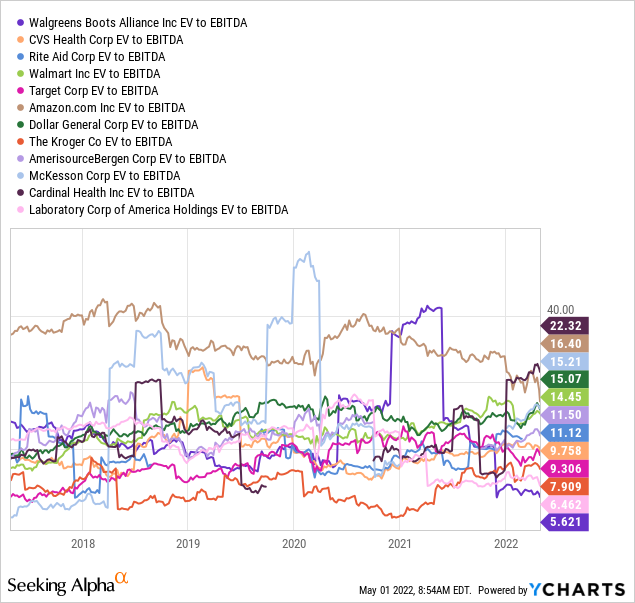

Even contemplating Walgreens heavy debt load (together with future rents), after we cross document earnings in 2021-22 with a multi-year inventory worth low, a cut price ratio of enterprise worth to earnings earlier than curiosity, taxes, depreciation and amortization exists right this moment. You may see beneath the 5.4x EV to EBITDA a number of is way beneath the peer and competitor group median common of 11x, or the S&P 500 nearer to 16x (not pictured).

YCharts

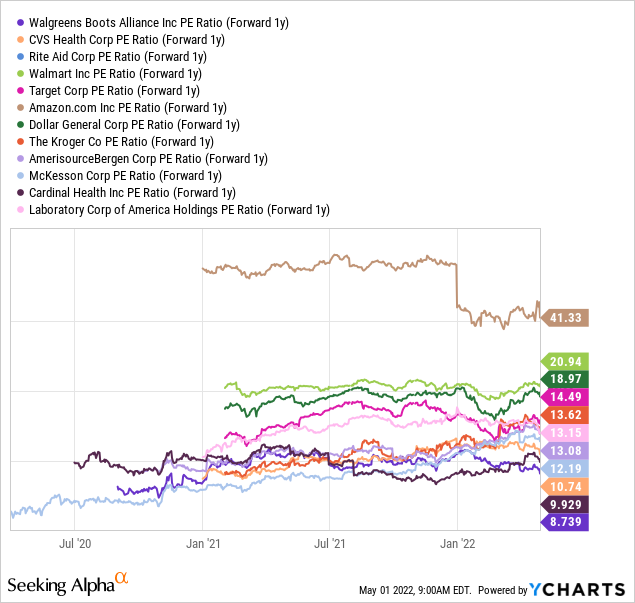

Wanting ahead 1-year to 2023 expectations by analysts on Wall Road, worth to EPS stays amazingly low cost. A projected 8.7x P/E is the bottom of the group and much away from the 13x median common.

YCharts

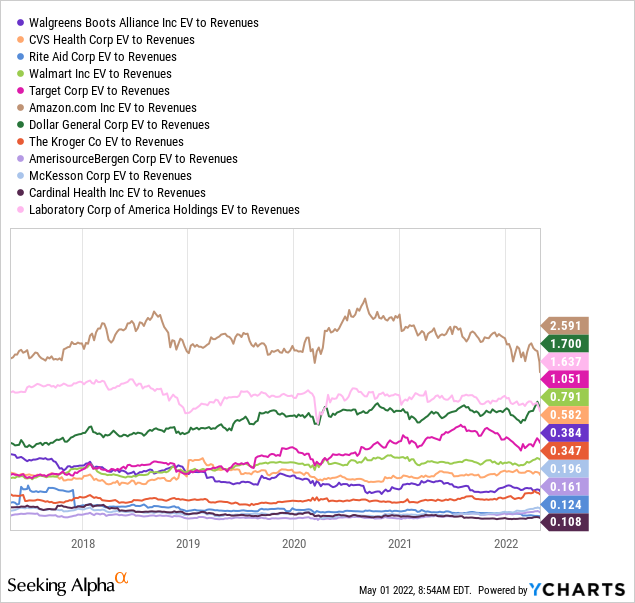

EV to revenues of 0.38x for Walgreens is extra typical vs. friends, however nonetheless represents about HALF the extent of 5 years in the past. Decrease remaining margins are the explanation why, a direct results of further leverage and curiosity expense.

YCharts

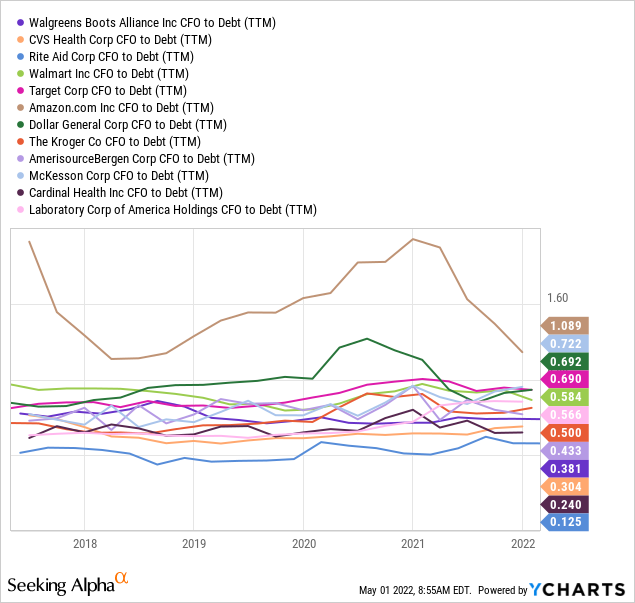

Money stream technology to complete debt can be on the weaker facet vs. the peer group. The simplest strategy to elevate WBA’s valuation over the brief run could be a easy technique of paying off debt quickly. If the corporate receives money for Boots and makes use of it completely to extinguish debt, it could change into tough for inventory quote to say no a lot from $42 a share. My considering is Wall Road analysts would rerate the remaining, extra worthwhile U.S. operations at the next valuation on improved margins general.

YCharts

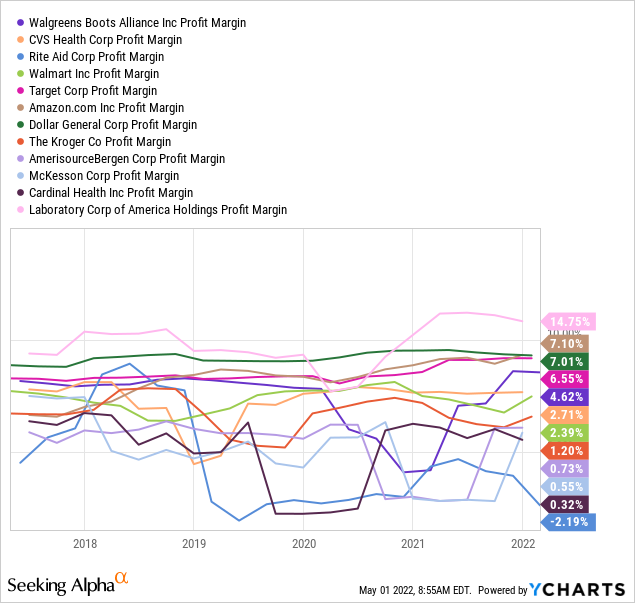

Lastly, remaining revenue margins are low vs. the common S&P 500 enterprise, however not horrible in opposition to well being care supply and main retail friends. For instance, remaining earnings on gross sales of 4.8% is at present a greater quantity than closest competitor CVS, or Walmart and Kroger (extra lower-margin meals gross sales), whereas just below the extent for Goal and Greenback Normal.

YCharts

Worthwhile Dividend Yield

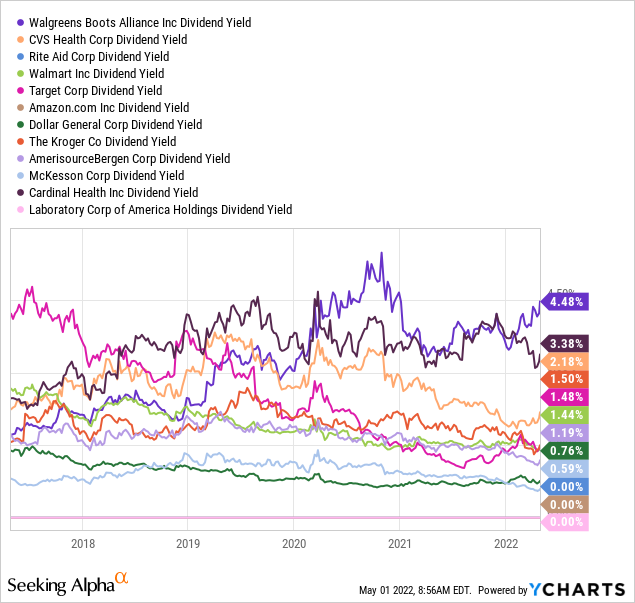

After the lowball valuation story, the following finest cause to personal Walgreens is its terrific annual dividend yield. Earnings traders will love the 4.5% dividend price on $42 per share, greater than TRIPLE the peer group median common and equal S&P 500 price of 1.4%. It’s additionally nicely above the complete Treasury bond yield curve, with “fastened” coupons largely within the 1% to three% vary right this moment. If administration can get development going once more, dividend hikes are coming with even stronger distribution test quantities despatched to your mailbox or brokerage account.

YCharts

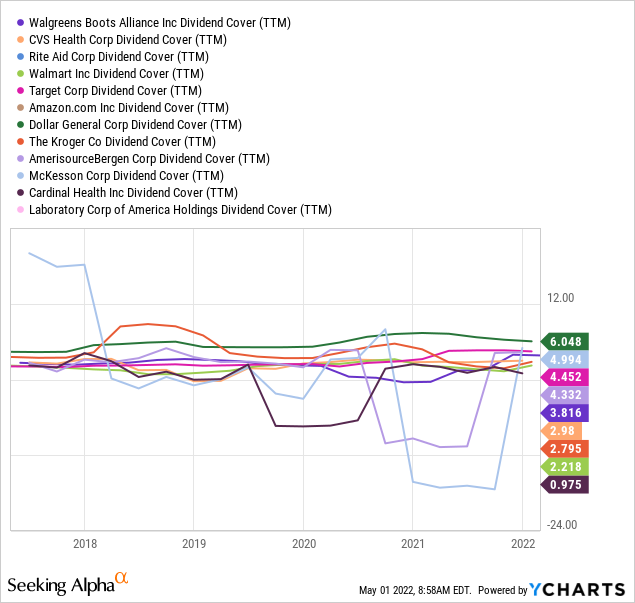

Wall Road is so bearish on Walgreens proper now, it’s largely ignoring the highly effective dividend proposition. On document earnings, WBA has a robust dividend cowl of three.8x over the previous 12 months, pictured beneath.

YCharts

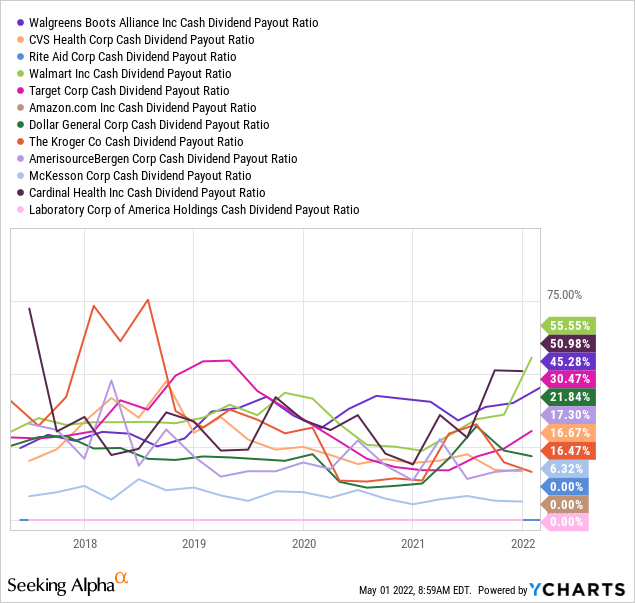

The working payout price at 45% of money stream technology is admittedly greater than I would like, however once more the Boots sale proceeds and easy constructive results from rising inflation in America ought to hold earnings and money stream round document ranges in 2022-23.

YCharts

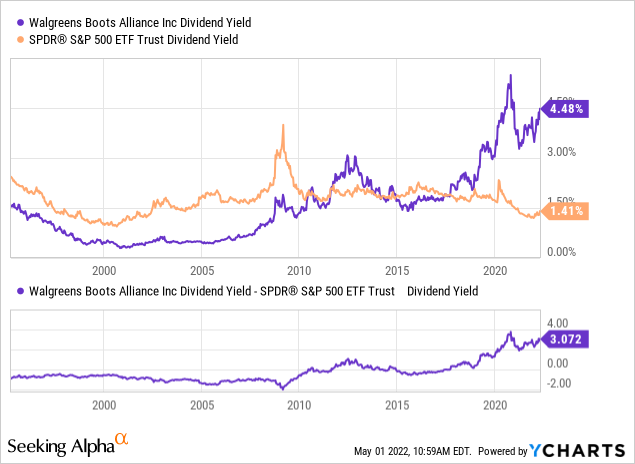

Beneath is a chart evaluating the Walgreens trailing dividend yield since 1995 to the identical accessible yield from the SPDR S&P 500 ETF (SPY). Whereas WBA usually bought at a premium valuation earlier than 2012 (from anticipated above-average enterprise development charges), together with a decrease money yield vs. the final U.S. inventory market, that started to vary markedly in 2019. In the present day, we now have reached a near-record constructive yield unfold for the corporate, standing virtually +3.1% above the equal S&P 500 money distribution price on new funding.

YCharts

Retailer Focus Reimagined

I’ve my very own view on some methods to extend shareholder worth, after promoting Boots. The principle concept is to leverage its community of prime actual property areas, in heavy visitors areas of every city or metropolis, and rebrand itself as a prime well being and wellness vacation spot.

Give it some thought, not solely are you able to decide up your prescription, however every location may change into an extended-hours supply for primary major physician care. Walgreens is already onerous at work on this complimentary idea (CVS is doing the identical). The VillageMD partnership and 63% majority possession acquired in November 2021 goals to place hundreds of Village Medical Major Care physician places of work subsequent door or as a part of transformed Walgreens areas.

VillageMD Web site VillageMD Web site

One other angle is to refit and restock its intensive native chain of retail areas to promote extra magnificence and wellness merchandise as an alternative of meals and common merchandise, which may strongly differentiate its enterprise vs. CVS or Walmart/Goal shops. What if native Walgreens weren’t solely your pharmacy and physician of alternative, however a prime spot to seek out varied well being merchandise, nutritional vitamins and dietary supplements, shampoos, lotions, cosmetics, grooming provides, health gear, and extra.

Given the correct Walgreens wellness push, administration may weigh some great benefits of placing a small yoga/aerobics studio into some ground plans, or an eye-doctor workplace, or perhaps a hair/nail salon. All advised, a Walgreens technique shifting towards a well being middle for native residents might be the profitable play right this moment vs. a number of cabinets promoting sweet, toiletry and family items with solely minor gross sales each day.

Ultimate Ideas

One other asset shuffle concept could be a merger between Walgreens and AmerisourceBergen. Such may efficiently and profitably stabilize and consolidate gross sales round prescription drugs, each in wholesale and retail provide channels. ABC is a detailed second for market capitalization dimension and complete gross sales to McKesson on the wholesale supply of medical merchandise and prescribed drugs to the U.S. well being care system. Given Walgreens already owns 28% of the corporate, buying one other 22% to realize 50%+ voting management with a consolidation of accounting outcomes would value an estimated $7.5 billion on the present ABC share worth (roughly equal to the estimated Boots proceeds in a money sale or 1.5x years of money stream technology for WBA).

My level is Walgreens inherently maintains a wide range of avenues to enhance shopper well being and wellness retail choices to drive gross sales and earnings development, past the fundamental pharmacy strategy. It may additional and simply consolidate the pharmacy provide chain beneath one roof. Plus, its huge actual property empire permits for better monetary flexibility (together with many fastened and contract-rate rents) as inflation charges soar. The 4.5% dividend yield seems to be one of many smarter earnings alternatives accessible on Wall Road right this moment, triple the S&P 500 yield, with future payout raises supported by common inflation within the U.S. economic system.

What are the draw back dangers on funding? Whereas the enterprise is considerably recession proof, with the vast majority of gross sales originating within the pharmacy, a deep recession often is the major threat that would carry decrease gross sales, money stream and earnings, notably if debt/leverage stays abnormally excessive. The second largest direct threat to the inventory quote is a weaker economic system and rising rates of interest proceed to tug all U.S. equities decrease, together with WBA. The bear market of 2022 has not been type to the Walgreens share quote, and this probably may proceed for months.

What about competitors from Amazon? Wall Road is nervous Amazon is entering into pharmacy gross sales on-line, and can possible steal some market share initially. Nonetheless, final week’s bearish Q1 Amazon report and lowered steering for 2022 means its palms are full with a slowing economic system. And, if Walgreens strikes additional right into a well being/wellness focus, simply blocks from your own home, Amazon may very well not be an enormous quick risk for knowledgeable in-person recommendation and gross sales.

For contrarian traders with a penchant for deep worth blue-chip positions, Walgreens might be a screaming purchase right this moment (or within the coming weeks on but decrease quotes). I don’t personal a stake as of this writing however am formulating a purchase plan throughout early Might. Doubtless, WBA is a ticker image demanding extra in-depth consideration by critical long-term traders, particularly the income-hungry crowd affected by rates of interest nonetheless amazingly low vs. trendy monetary market historical past.

Thanks for studying. Please contemplate this text a primary step in your due diligence course of. Consulting with a registered and skilled funding advisor is beneficial earlier than making any commerce.