Justin Sullivan

Walgreens Boots Alliance (NASDAQ:WBA) had considerably of a troublesome quarter however the run-rate state of affairs seems to be fairly good. With resilient retail exposures and a number of other vectors of restoration from waning COVID-19 forces the outlook isn’t too dangerous, particularly within the face of what has turn into a fairly low a number of. Everybody loves an ample dividend too, and WBA’s is effectively lined. The outlook has components that development optimistic and will mitigate no matter negatives we will anticipate from the macroeconomic atmosphere. On the very least it is a good earnings play.

WBA Overview

The corporate is a retail pharmacy and sweetness product firm. It runs this mannequin by means of the Boots and Walgreens manufacturers that used to exist independently. There have been plans to promote Boots to a keen purchaser, however problem in elevating capital for such a big deal when the market jitters hit torpedoed these plans, and the corporate plans to run with the Boots belongings for the foreseeable future.

On a reporting foundation they function in two segments: United States and Worldwide. Boots is contained within the worldwide phase whereas Walgreens is reserved to america phase. The cut up is about 85:15 by way of income between the segments. Investments are specializing in Walgreens and never a lot on Boots, particularly funding into Shields for specialty pharmacies and the VillageMD investments which began in tandem with CVS (CVS) in 2020 to prepare on capitalizing on vaccinations but in addition making an attempt to make WBA a extra complete offeror as per their omnichannel technique.

Q3 Replace

The latest outcomes got here out this month they usually look challenged on the floor however fairly cheap when squaring it with the a number of and the YTD traits. Due to sturdy comps from final 12 months, the US phase is struggling, with AllianceRx taking a significant hit on account of falling vaccination numbers.

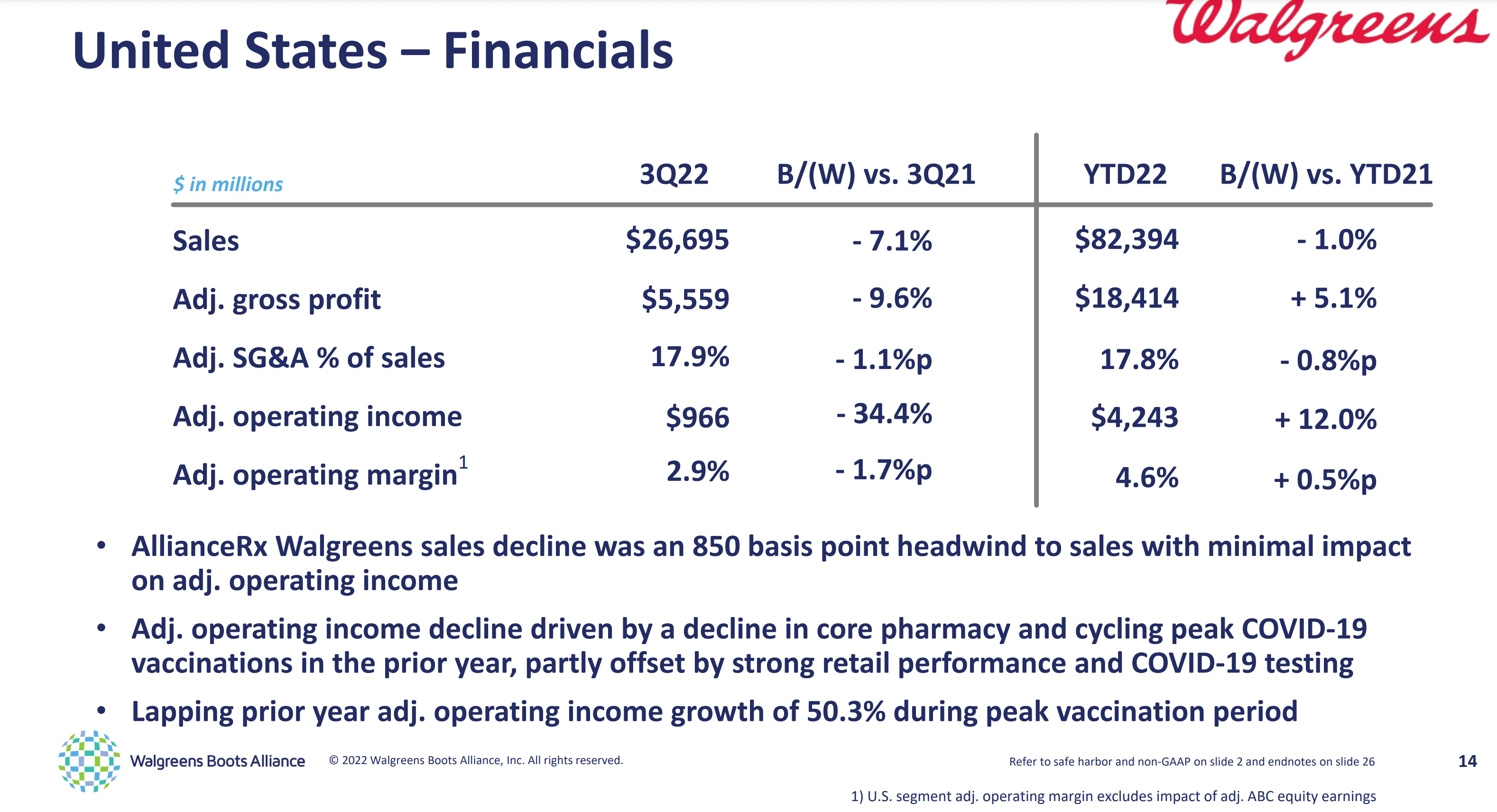

US Section (Q3 2022 Pres)

The EPS declined 29% YoY and 18% is coming from these falling vaccination figures. Many of the remainder of the headwinds are additionally coming from bills associated to the growing footprint of VillageMD which is rising shortly and regardless of its small dimension making a modest contribution to the topline. These detrimental results from AllianceRx offset good efficiency by way of gross sales in retail and the rising VillageMD clinic footprint which tripled during the last 12 months. Gross sales development would have been 3% YoY this quarter have been it not for AllianceRx and associated vaccination declines, the place the precise gross sales development was -3% on a relentless foreign money foundation.

The opposite headwind within the US was pharmacy. Ordinarily pharmacy and script volumes must be strong, and certainly that is an space that provides the corporate stability within the detrimental macro atmosphere we’re anticipating however labor shortages are making it troublesome to capitalize on a restoration in site visitors and mobility. Computerized fulfilment methods are mitigating the impacts right here no less than.

Pharmacy Subsegment (Q3 2022 Pres)

Lastly, the transferring away from tobacco revenues, particularly coming off sturdy COVID-19 comps, has been a headwind for normal merchandise, however a restoration in private care helps volumes and stabilizing the image. Granted, these volumes have been coming from at house testing kits for COVID-19, which whereas a dependable contributor now might be topic to uncertainty as attitudes round COVID-19 change. So long as isolation on analysis is remitted by workplaces we predict WBA will probably be secure on this one. Furthermore, issues like picture providers are additionally seeing a restoration and contributing again into the margins as mobility returns.

The Walgreens Well being enterprise which accommodates the VillageMD publicity grew by 65% excluding AllianceRx impacts, however did so unprofitably for now as a quickly increasing footprint nonetheless must mature into being a revenue contributor after the expansion part.

Within the worldwide phase, which hasn’t been mentioned but, there’s development in each income and gross sales because of restoration primarily in Boots UK. Pharmacy was a nonetheless a little bit of a languisher as regular healthcare utilisation turns into restored, though it did develop, however all different retail classes grew in addition to the wholesale enterprise in Germany.

Valuation

The Q3 accounts for about 16% of the everyday Q3 share of annual revenues. Taking YTD figures subsequently and annualizing them by implying one other quarter on the present run-rates, the place YTD evolutions on each gross sales and working earnings have been optimistic, creates a extra credible image for constructing what’s going to nonetheless be a conservative a number of. With a P/E just under 7x, and subsequently an earnings yield that covers with substantial margin the 5% dividend yield, the corporate would not have a heady a number of and gives a secure earnings.

Annualizing like this is not a stretch. We should always have comparable headwinds onto EPS from the Walgreens Well being growth, lapping vaccination ranges from 2021, in addition to working by means of investments to mitigate and restore the labor state of affairs in shops. Whereas VillageMD will possible maintain incurring growth expense the opposite headwinds ought to begin to dissipate considerably, however the vaccinations do stay an unknown. We expect we might have arrived at extra normalized charges as of now, since some COVID-19 vaccination will proceed as there will probably be extra variants, however apart from this troublesome to foretell space EPS headwinds are coming off.

Conclusions

The macro considerations exist for all firms, and disposable earnings declines which might be anticipated to be introduced on by the curiosity hikes ought to see some influence on WBA income by means of the retail phase. Pharmacy ought to get better regardless and supply resilience. Furthermore, with logistics prices being excessive, individuals are optimizing by attending the retail footprint extra, sustaining its place of their omnichannel strategy. Any pent-up demand not being met as a consequence of labor shortages ought to turn into captured in a few quarters’ time. The corporate trades at a low a number of and at a reduction from CVS which admittedly advantages from extra strong exposures owing to Aetna. The earnings is there too with a 5% dividend.